A secondary market is a financial ecosystem where existing investors buy and sell securities from one another rather than from the company that originally issued them. In a primary market transaction, a business or fund sells new securities and receives the proceeds. In a secondary transaction, those securities change hands again, and the cash flows to the seller, not to the issuing company. The most familiar example is the stock market: when you buy Apple shares on Nasdaq, Apple gets nothing. The seller gets your money.

That distinction sounds academic until you start thinking about private equity secondaries, pre-IPO shares, and limited partner (LP) fund interests. The same principle applies, but the mechanics, pricing, and liquidity look almost nothing like a public exchange. This guide covers both, with most of its weight on what serious readers want to understand: how private equity secondaries work, how to buy and sell pre-IPO shares, what the platforms do and don't do, how pricing is set, and how to track it all.

What is the secondary market?

A secondary market is a venue, whether formal or informal, where securities trade between investors after their original issuance. The asset already exists; ownership simply moves from one holder to another at whatever price the buyer and seller agree on.

In public markets, that structure is heavily standardized: the NYSE and Nasdaq match millions of orders per day, settle in two business days, publish prices in real time, and operate under SEC and FINRA rules. Liquidity exists, and price discovery happens continuously.

In private markets, almost none of those conditions apply. There is no central order book for a private company's shares, and no continuous quote for a fund's LP interest. Transfer restrictions and information rights are written into the original documents. A buyer and seller can agree on a price, but the company or general partner usually has to approve the transfer, and the value being traded might be measured against a number that's three to nine months stale.

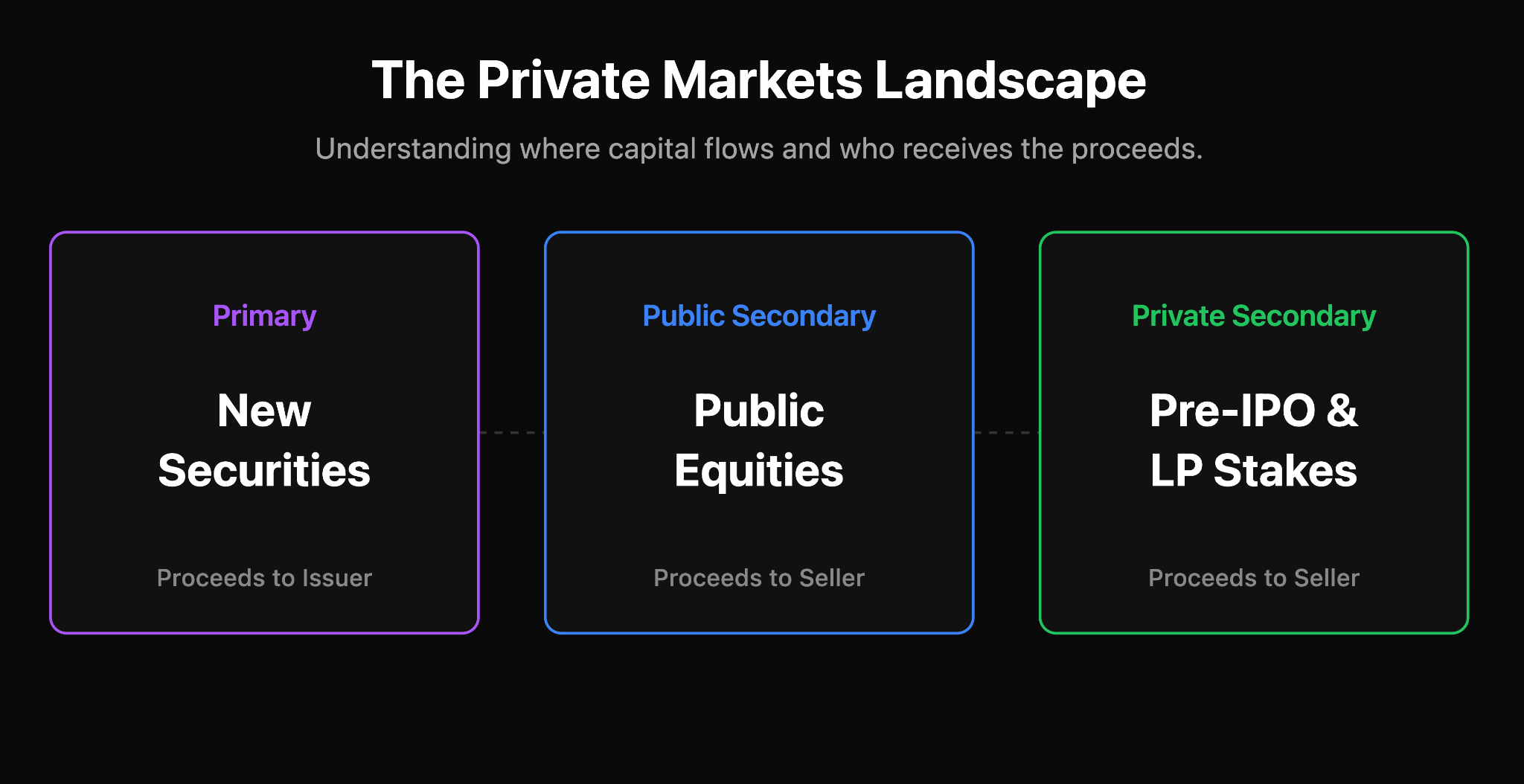

Primary market vs secondary market

The cleanest way to keep these straight is to ask one question: who gets the money?

For public-market readers, the implication is mostly conceptual: most of what happens on the stock market is secondary, even though people often refer to a hot IPO as 'the market.' For private-market readers, the implication is operational. Founders and boards care who appears on the cap table, and that affects every part of the deal.

The four main types of private secondary transactions

There are public secondaries (the NYSE and its peers), and then there are private secondaries, which split into four practical categories. Mixing them up leads to confused expectations about pricing, approvals, and who is on the other side of the trade.

Each has its own pricing logic and its own definition of 'approved.'

The private equity secondary market

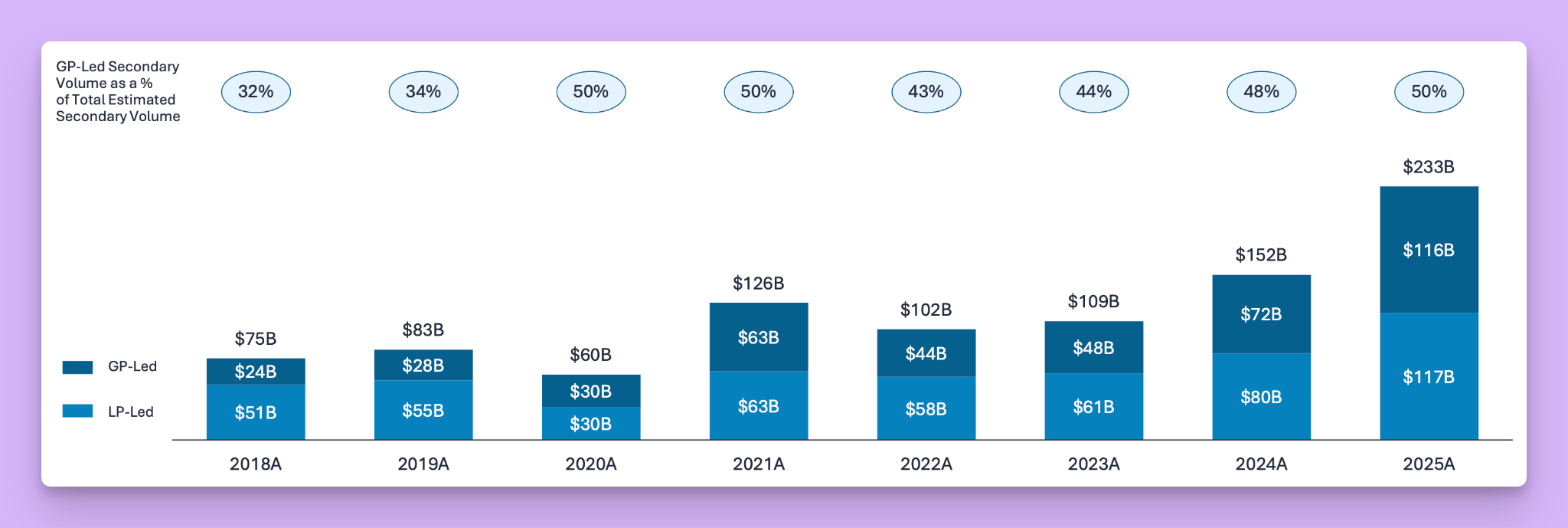

The PE secondary market has matured into a serious institutional segment of private capital. In 2025, GP-led deals reached $116 billion while LP-led transactions hit $117 billion, and dedicated secondary capital reached a record $327 billion (Lazard, Jefferies).

LP-led secondaries are the older format. A limited partner in a buyout, venture, credit, or infrastructure fund decides to sell its interest before the fund's natural term. The buyer steps into that LP's shoes, taking the existing portfolio exposure plus any unfunded commitments.

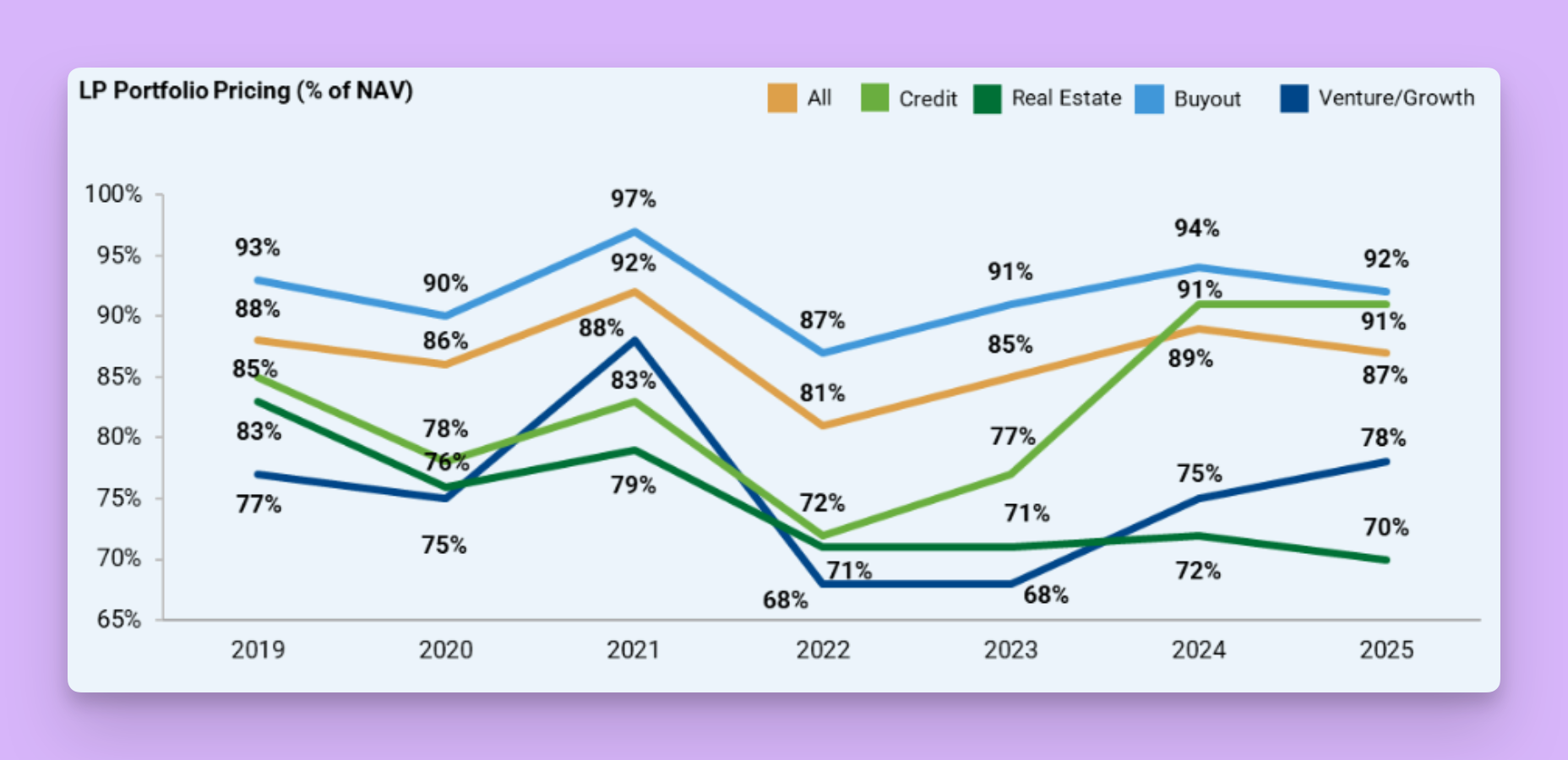

Pricing is usually quoted as a percentage of NAV. Sellers do this because an endowment is overallocated, a pension needs liquidity, a corporate is exiting an asset class, or a family office wants to redirect capital. Buyout pricing finished 2025 at 92 percent of NAV, venture and growth at 78, credit at 91, and real estate at 70.

GP-led secondaries are the faster-growing category and the more interesting one structurally. The general partner of an existing fund identifies one or more assets it wants to hold longer, sets up a continuation vehicle (CV), and offers existing LPs the option to take cash, roll into the new vehicle, or do a partial combination of each. New buyers underwrite the CV directly. Continuation funds dominated the GP-led market at roughly 86 percent of total volume in 2025. By 2025, nearly 80 percent of the top 100 sponsors by AUM had completed a CV transaction.

The appeal is real: shorter duration than primary commitments, a clearer view of underlying assets, and J-curve mitigation. The risks are equally real: NAVs lag the market, and GP-led conflicts are not theoretical, which is why fairness opinions and LPAC processes matter. Unfunded commitments transfer with LP interests.

Pre-IPO secondary markets: buying and selling private company shares

The other large piece of private secondaries is direct trading in private company shares, especially late-stage venture-backed names. This is where most individual accredited investors and startup employees encounter the term.

On the seller side: founders looking for partial liquidity, current and former employees with vested stock, angel investors, and early funds whose lifecycle is winding down. On the buyer side: accredited investors, family offices, secondary funds, dedicated platforms, and strategic investors arranged through company-run programs.

Three transaction structures dominate. Tender offers are run by the company itself, often annually or every couple of years. The company sets the price, eligibility rules, and the buyer or buyers. In 2025, US company-led tender offers reached roughly $35 billion, and they have become a standard talent-retention tool at companies that have stayed private for a decade or more.

Direct secondary sales happen when a shareholder negotiates a transfer with a single buyer through a broker. Marketplace transactions route the same kind of trade through a platform that handles introductions, paperwork, and settlement. In every case, the company sits in the middle. Most have a right of first refusal (ROFR), board approval requirements, and rules about eligible buyers. A listing on a marketplace is an indication of interest, not a closed trade.

Sellers sell for practical reasons: diversifying a position that has grown to most of their net worth, paying for a house or a tax bill, or fatigue with an IPO that has been five years away for five years.

How to buy pre-IPO shares step by step

Treat this as a process, not a click. The friction is the point.

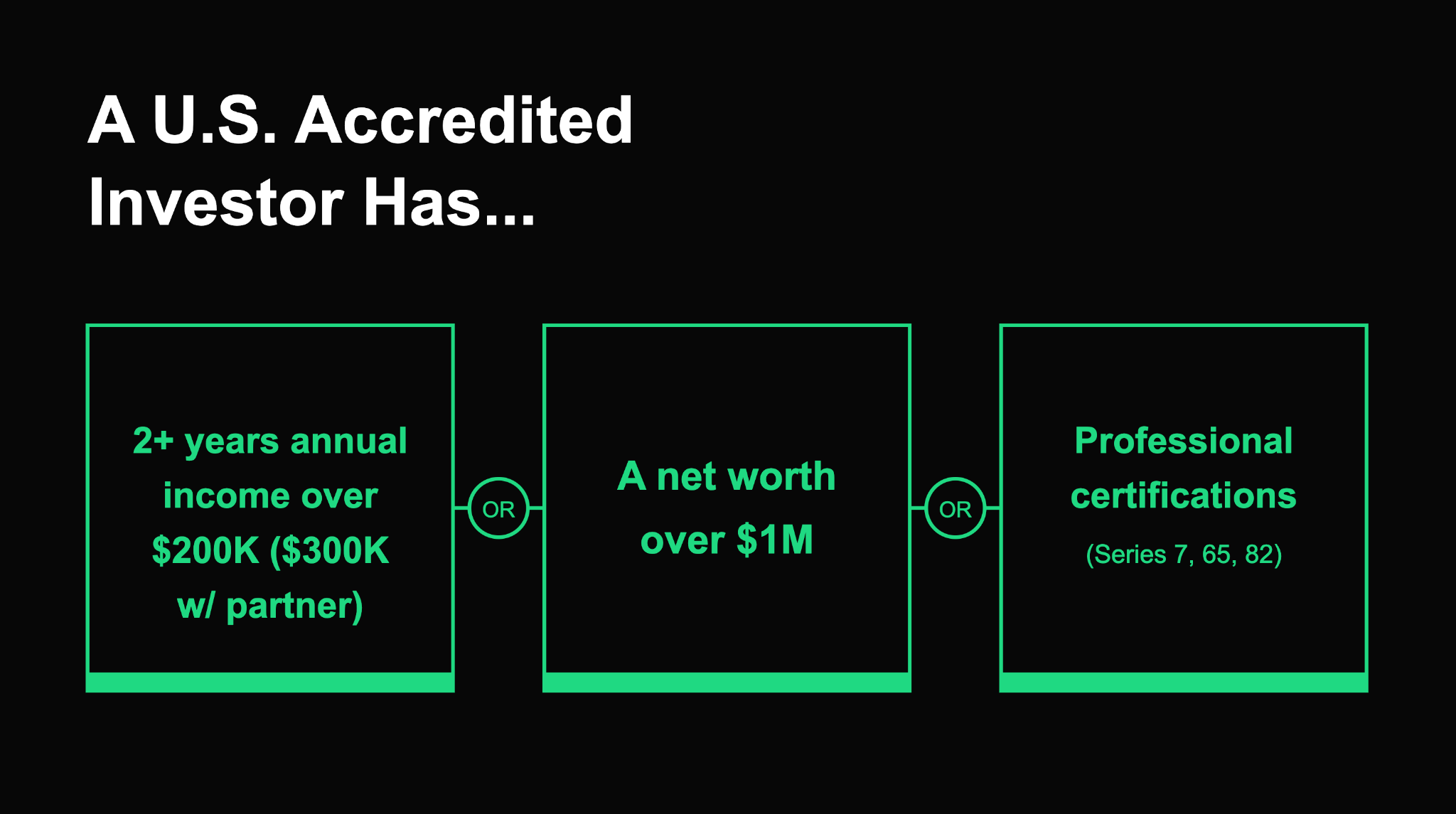

- Confirm accredited investor status: Individuals qualify with net worth over $1 million excluding primary residence, income over $200,000 individually or $300,000 jointly for the past two years with reasonable expectation of the same in the current year, or holding a Series 7, 65, or 82 license in good standing.

- Pick a route: A direct deal through a broker, a marketplace platform, a fund vehicle, or a company-run tender offer all have different mechanics, fees, and minimums.

- Review the company and the share class: Common stock and preferred stock have meaningfully different rights. Preferred stack, liquidation preferences, and board control all matter, and so does the date of the financials you are being shown.

- Understand approvals and restrictions: ROFR, board approval, and information rights vary by company. Ask exactly what has been confirmed and what has not.

- Read the structure: Many platforms route smaller buyers through an SPV, which changes voting rights, fee economics, and distribution timing.

- Confirm fees and minimums: Forge Global typically requires $100,000 for direct deals and $5,000 through Forge Funds. Augment historically required $100,000+ for direct trades and launched a smaller-ticket Collective product (starting from $10,000). Hiive charges sellers around 5 percent on closed transactions. Verify before assuming.

- Plan for taxes and holding period: QSBS Section 1202 may or may not apply depending on when shares were issued and how they were acquired.

- Custody and document the position: Get the transfer notice, executed assignment, and share register update in writing.

- Do not assume liquidity: If you need the cash on a calendar, do not put it here.

Buyer's checklist:

- Accredited status confirmed and verifiable

- Counterparty identity clarified (employee, fund, broker, SPV)

- Share class and capital structure understood

- ROFR and approval status known

- Fee schedule reviewed (transaction, SPV, ongoing management)

- Holding-period and basis records preserved

- Liquidity expectations decided

How to sell pre-IPO shares step by step

For startup employees, this is often the first time investment friction becomes personal. Treat it the same way.

- Pull your equity documents: Stock plan, grant agreement, exercise notices, 83(b) elections. Do not rely on memory.

- Identify what you actually own: Common stock from exercised options, vested RSUs, restricted stock with remaining vesting, or unexercised options that cannot usually be sold directly. The path differs.

- Check transfer restrictions and ROFR: Most private companies require formal notice and a window in which they can match or block the sale.

- Look for an active tender offer: A company-run program is almost always cleaner than a third-party transaction: known price, known timing, no individual approval friction, often better tax mechanics.

- Model the tax outcome before you sign: ISO and AMT issues can turn a clean-looking sale into a surprise tax bill. State residency, holding period, and possible QSBS eligibility all change the math. Bring a CPA in.

- Choose the venue: Forge, EquityZen, Hiive, Augment, Nasdaq Private Market, FNEX, and traditional brokers all play roles at different scales.

- Expect documentation and delay: Stock transfer notices, ROFR waivers, escrow, and counterparty KYC routinely add weeks. Sometimes months.

- Do not violate company policy: Confidentiality and trading-window rules are real, as are clawback provisions in many recent grant agreements.

Seller's checklist:

- Grant and plan documents in hand

- Share type and tax basis confirmed

- ROFR and company approval pathway clear

- Tender offer alternative considered

- AMT and capital gains modeled

- Net proceeds (after platform and broker fees) calculated honestly

- Timeline tolerance set realistically

Platform comparison

The platforms are not interchangeable. They serve different ticket sizes, different participants, and different segments of the cap table. The table below summarizes typical positioning, with the caveat that minimums, fees, and structures change. Verify current terms with the platform before transacting.

A few patterns are worth noticing. Forge and EquityZen lean toward fund-pooled, smaller-ticket access for accredited individuals. Nasdaq Private Market is fundamentally a company-sponsored program operator, not a marketplace investors browse. FNEX is institutional. Hiive emphasizes a more exchange-like experience with visible bid/ask quotes. None of them eliminates the underlying frictions of private transfers; they manage them at different levels of fee, transparency, and minimum size.

How secondary market pricing works

Pricing is the most interesting and most misunderstood part of the secondary market. There are several reference points, and they often disagree.

In LP-led deals, the headline number is the percent of NAV. The buyer underwrites the underlying portfolio and offers a price as a percentage of the latest reported net asset value. NAV itself is reported on a delay. 2025 averages landed at 87 percent of NAV across LP portfolios overall, with significant variation by strategy.

In direct pre-IPO deals, common reference points are the last primary funding round price, the company's 409A valuation (used for option pricing and generally lower than the preferred-share price), recent secondary tape if available, and the platform's own indicative price (Forge Price, Hiive bid-ask, Augment data feed). These can diverge by 20 percent or more depending on demand, share class, and information available.

In GP-led deals, single-asset CVs price off underlying business value, usually with a fairness opinion. Multi-asset CVs blend portfolio-level views with individual underwriting.

One idea matters more than the headline discount: forward IRR beats nominal discount. A 25 percent discount to a stale NAV that takes seven more years to distribute is not the same as a 10 percent discount on a fund about to harvest mature assets.

A real life example

- Buyer A acquires a $1,000,000 NAV LP interest at 75 cents on the dollar, paying $750,000. Over four years, the fund distributes $1,000,000 cumulatively. Buyer A's IRR is roughly 7.5 percent, before fees and unfunded commitments.

- Buyer B acquires a similar interest at 90 cents, paying $900,000, and receives $1,100,000 over two years. Buyer B's IRR is closer to 10.5 percent.

The deeper discount loses to the faster distribution.

The discount illusion

A 25 percent discount to NAV is not automatically a bargain. Three things can quietly destroy the value of a steep discount: the NAV itself can be stale and overstated; future distributions can be years away; and forward returns can be weaker than the seller's record suggests. Buying cheap is meaningful only if the cash you actually receive, on the timeline you actually receive it, beats the alternatives. The discount is the entry point. The IRR is the answer.

Risks and downsides of secondary market investing

Public-market investors are used to deep liquidity, narrow spreads, and standardized disclosures. The private secondary market gives up nearly all of that.

Once you own a private fund interest or a block of pre-IPO common stock, you may not be able to exit on any timeline you control. Information asymmetry is real, and rarely in your favor. Valuations are reported with a lag of three to nine months, and counterparty risk lives in the wiring, the transfer agent, and the company's willingness to actually approve a transaction.

Fees are layered. Transaction fees, SPV fees, ongoing management fees, and bid-ask spreads can compound into 5 to 10 percent of total economics before you have earned a dollar. Concentration risk is acute when the position is a single private company. Unfunded commitments can call capital at the worst time, and GP-led conflicts can put the buyer on the wrong side of valuation. Tax surprises (AMT, K-1 timing, state apportionment) are common enough to plan for.

Tax treatment of secondary transactions

This is one of the most situational areas in private markets, and it deserves real tax counsel before any meaningful trade. Capital gains are usually triggered when shares or fund interests are sold, with holding period and basis determining whether the gain is short or long term.

QSBS under IRS Section 1202 can shield a meaningful portion of gain on qualified small business stock, but the rules around eligible companies, holding period, and acquisition method (founders' stock, exercised ISOs, secondary purchases) are technical. Buyers acquiring shares in a secondary transaction often do not get QSBS treatment because of the original-issuance requirement. This is exactly the kind of detail that costs people six and seven figures when they discover it after the fact.

For employee sellers exercising and selling, ISO and AMT exposure can be significant. A same-year exercise and sale generally produces ordinary income on the spread; a hold past one year from exercise and two years from grant qualifies for long-term treatment but creates AMT risk in the exercise year. Tender offers can be structured cleanly for tax reporting. Private fund K-1s arrive late, allocate income across multiple jurisdictions, and can include phantom income that creates tax liabilities without distributions to fund them.

None of this is legal or tax advice. The only useful generalization is that a serious secondary transaction deserves a serious tax conversation before, not after, signing.

How secondaries fit into a portfolio

Treat private secondaries as long-term capital, even when the duration is theoretically shorter than a primary commitment. A secondary fund's J-curve is shallower, but it is still a private vehicle with multi-year hold periods. A pre-IPO direct position is even more concentrated, less liquid, and more dependent on a single outcome than a fund.

Diversification matters more, not less, when individual positions are illiquid. Vintage diversification on the LP secondary side smooths distribution timing. Manager and strategy diversification reduce single-fund risk. For pre-IPO direct shares, position size should reflect both expected return and the cost of being wrong, with extra weight on the latter because there is no daily mark. A practical liquidity budget helps: target a fixed share of the portfolio for illiquid investments and adjust gradually rather than reactively.

The operational challenge of tracking secondary holdings

The reporting infrastructure for secondary holdings is fragmented in ways public-market investors rarely experience. A typical sophisticated investor with private exposure ends up tracking pre-IPO shares on Carta or another equity platform, LP fund interests through quarterly capital account statements and K-1s, direct secondary stakes through executed PDFs and sporadic broker updates, real estate syndications through their own sponsor portals, and crypto in still other places. The standard brokerage dashboard shows none of it.

The result is predictable: investors meaningfully understate their net worth, allocation decisions are made against incomplete data, and large illiquid positions go un-rebalanced for years. The problem is not lack of data. It is the lack of a single place to bring it together.

When technology helps

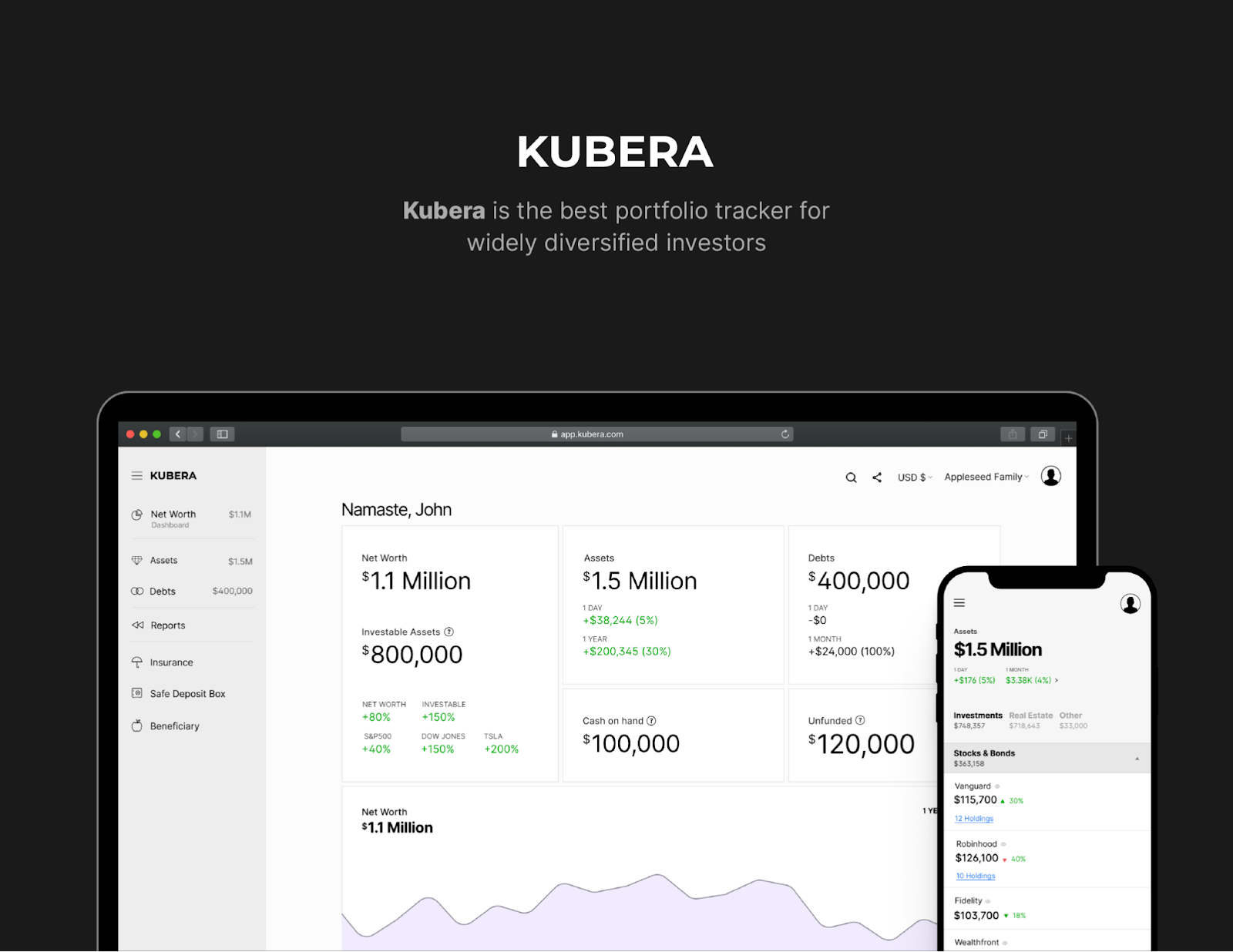

This is where a tool like Kubera earns its keep without much drama. A net worth and portfolio tracking platform that handles bank accounts, brokerage, crypto, real estate, private fund interests, and secondary share positions in one view answers the practical question: what do I actually own, and what is it roughly worth right now, what’s the IRR?

Useful capabilities include a Carta connection for private company equity, manual entry for LP capital accounts and direct secondary positions, AI powered document-based updates for K-1s and quarterly statements, and a single allocation snapshot that reflects both liquid and illiquid holdings. None of this replaces fund-level reporting, but it ends the spreadsheet sprawl that makes most investors' private exposure invisible to themselves.

Sign up now for a 14 day trial to get started and explore more.

Frequently Asked Questions

What is a secondary market?

A secondary market is any venue where existing securities trade between investors after their original issuance. Public stock exchanges are the most familiar example. Private secondary markets cover private equity fund interests, pre-IPO company shares, and other illiquid positions.

What is the difference between primary and secondary markets?

In a primary market, the issuing company or fund sells new securities and receives the capital. In a secondary market, an existing investor sells to another investor, and proceeds go to the seller. The issuing company often has approval rights but does not usually receive cash.

Can individual investors buy pre-IPO shares?

Generally only accredited investors can purchase pre-IPO shares. Even then, access depends on the company's transfer policies, the platform involved, and minimum investment thresholds. Some platforms offer fund-pooled access starting around $5,000, while direct deals often require $100,000 or more.

What are private equity secondaries?

Transactions involving existing limited partner interests in private equity funds (LP-led) or assets transferred into new vehicles by general partners (GP-led). Buyers acquire exposure to existing portfolios rather than committing to a new blind-pool fund.

What is a GP-led continuation vehicle?

A new fund created by an existing private equity sponsor to hold one or more assets longer than the original fund's term. Existing LPs typically choose between cash out, rolling forward, or a partial of each. New investors fund the new vehicle directly.

Are secondary shares risky?

Yes. Risks include illiquidity, information asymmetry, valuation lag, transfer restrictions, layered fees, and concentration risk in single-company positions. Returns can be attractive, but the downside profile differs meaningfully from public-market investing.

Why do secondary shares trade at a discount?

Discounts compensate buyers for illiquidity, valuation uncertainty, stale NAV, unfunded commitments, and the time value of waiting for distributions. A discount is not automatically a bargain; it can also reflect weak underlying assets or extended timelines.

Do I need to be an accredited investor to buy pre-IPO shares?

In nearly all cases, yes. SEC rules define an accredited individual as having net worth over $1 million excluding primary residence, income above $200,000 individually or $300,000 jointly for the past two years with reasonable expectation of the same in the current year, or holding a Series 7, 65, or 82 license.

How are secondary market transactions taxed?

Generally as capital gains, with treatment depending on holding period, basis, and the asset involved. QSBS, ISO/AMT, tender offer mechanics, and K-1 timing for fund interests can all change the outcome. Get tax advice before any large transaction.

Conclusion

Secondary markets exist because investors need liquidity and price discovery on assets that have already been issued. On public exchanges, that function happens at scale, transparently, and almost invisibly. In private markets, the same function exists but operates through a different stack: transfer restrictions, company approvals, fund agreements, NAV reporting cycles, and platforms that bridge buyers and sellers.

For sophisticated investors and informed employees, the private secondary market opens up real options: liquidity before exit, exposure to companies and funds that are not otherwise accessible, and tools for managing concentration and duration. None come without friction. Pricing is messier, information is thinner, timelines are longer, and the operational work of tracking what you own is meaningful.

Treat secondary investing as a long-term, well-diligenced part of a portfolio, plan for the friction, and keep your records in a place where you can see them.