What Is an Accredited Investor?

The accredited investor standard comes from Regulation D under the Securities Act of 1933. It determines who can participate in certain private securities offerings without the full disclosure protections required for registered public securities.

Accredited investor requirements for a natural person include meeting at least one of the following tests:

- Income: $200,000 or more in each of the two most recent years ($300,000 with a spouse or spousal equivalent), with a reasonable expectation of reaching the same level in the current year

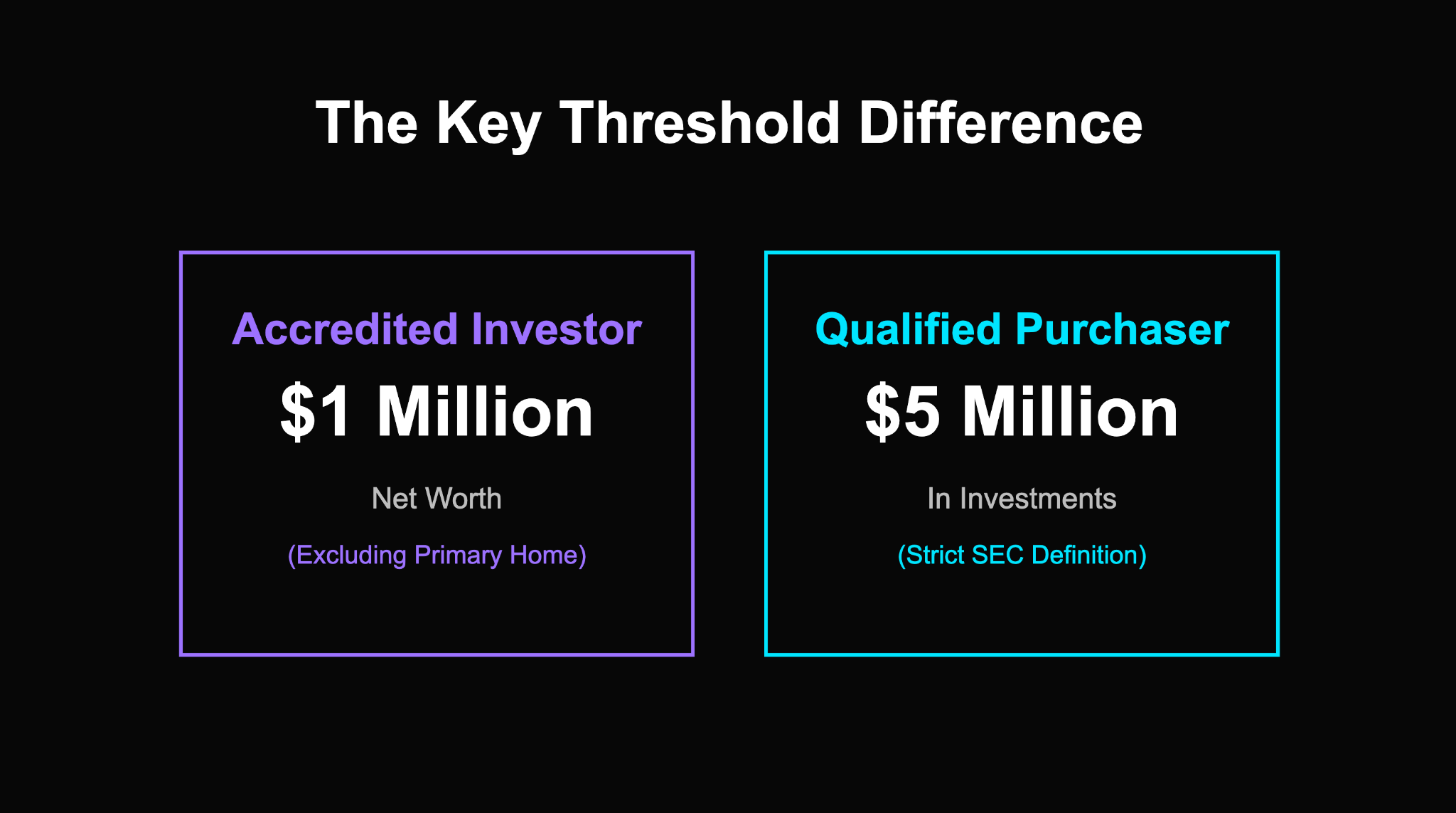

- Net worth: More than $1 million, excluding the value of the primary residence, individually or jointly with a spouse or spousal equivalent

- Professional license: Holds a Series 7, Series 65, or Series 82 license in good standing

- Knowledgeable employee: Certain employees of the fund in which they are investing may qualify under a separate test

Entities also have their own accredited investor requirements. A company, LLC, trust, or other entity may qualify if it holds total assets exceeding $5 million, or if all of its equity owners are themselves accredited investors.

The accredited investor standard applies to Regulation D offerings, including Rule 506(b) and Rule 506(c). For a detailed look at how Rule 506(c) verification works in practice, see our article on Rule 506(c) accredited investor verification.

What Is a Qualified Purchaser?

The qualified purchaser standard comes from the Investment Company Act of 1940, not the Securities Act. It is a separate legal framework with a different purpose.

Qualified purchaser requirements for a natural person center on a single threshold: the individual must own at least $5 million in investments. The critical word is "investments," not total net worth. The distinction is significant.

"Investments" under the qualified purchaser definition generally includes:

- Securities: stocks, bonds, publicly traded funds, and private fund interests

- Real estate held for investment purposes (not a primary residence, and subject to detailed rules about active business use)

- Cash and cash equivalents held for investment

- Commodity interests and certain financial contracts

"Investments" generally does not include:

- The value of your primary residence

- Personal property not held for investment purposes

- Assets used directly in the active operation of a business in which the investor is primarily engaged (subject to complex rules)

The $5 million threshold is for a natural person. The rules for trusts, companies, and other entities are more complex and should be reviewed with qualified legal counsel before relying on entity status for a fund subscription.

Accredited Investor vs. Qualified Purchaser at a Glance

Why One Deal Asks About Accredited Status and Another Asks About Qualified Purchaser

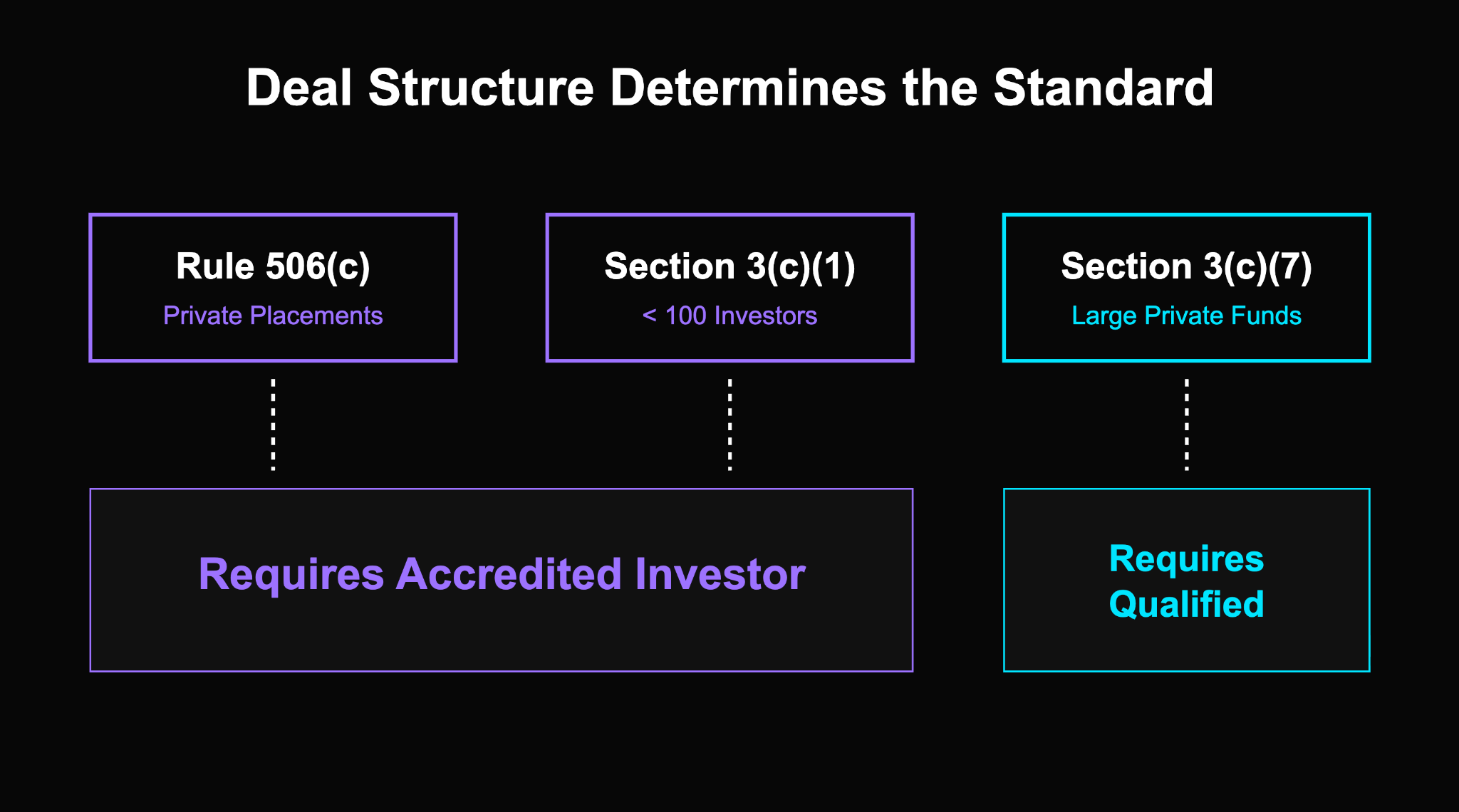

The answer lies in how the fund or offering is structured under federal law. Understanding 3(c)(7) vs 506(c) is the key to understanding why these standards apply in different situations.

Rule 506(c): accredited investor standard

Companies raising capital under Rule 506(c) of Regulation D can sell to accredited investors and must independently verify that all purchasers meet that standard. This is the rule you encounter most often in private placements, angel rounds, and real estate syndications.

Section 3(c)(1) funds: accredited investor standard with a 100-investor cap

Private funds can avoid registration as investment companies under Section 3(c)(1) of the Investment Company Act if they have 100 or fewer beneficial owners and do not make a public offering. Investors generally must be accredited investors. This structure is common for smaller hedge funds, private equity vehicles, and early-stage venture funds.

Section 3(c)(7) funds: qualified purchaser standard

Private funds can also rely on the Section 3(c)(7) exemption if all investors are qualified purchasers. This structure allows for more than 100 beneficial owners without triggering investment company registration. It is the structure used by large institutional hedge funds, major private equity vehicles, and venture funds that want to accommodate a broader investor base while remaining private.

When you encounter a fund that asks for qualified purchaser status rather than just accredited investor status, it is almost certainly a 3(c)(7) fund. The structure determines the requirement.

What Changed in March 2025 and What Did Not

In March 2025, the SEC staff issued a no-action letter that addressed verification procedures for certain high-minimum Rule 506(c) offerings under Regulation D. For offerings with a minimum investment of $200,000 or more per investor, issuers may now be able to rely primarily on written investor representations rather than third-party verification letters, provided specific conditions are met.

Key points on scope:

- This guidance applies exclusively to Rule 506(c) verification. It involves the Securities Act, not the Investment Company Act.

- The qualified purchaser standard is rooted in the Investment Company Act. The March 2025 guidance does not change it.

- Qualified purchaser requirements, the definition of "investments," and the documentation burden for 3(c)(7) fund subscriptions are unchanged.

- Funds relying on Section 3(c)(7) must still confirm that all investors meet the qualified purchaser standard, regardless of this guidance.

If you are qualifying for a 3(c)(7) fund, the March 2025 guidance does not apply to your situation. The two standards operate under different laws and respond to different rule changes.

What Documents Do Investors Usually Need?

For accredited investor verification

- Tax returns for the two most recent years (W-2s, Form 1040, K-1s) for income-based qualification

- Bank and brokerage statements, dated within 90 days, for net worth-based qualification

- Mortgage statements and liability documentation to support net worth calculations

- Professional license documentation if using the Series 7, Series 65, or Series 82 path

For qualified purchaser verification

- Comprehensive investment account statements across every qualifying account

- Real estate investment holding documentation, clearly marked as investment property rather than personal residence

- Private fund interest documentation, including current NAV statements where available

- A clear breakdown separating qualifying investments from non-qualifying assets (personal property, business operating assets, primary residence)

- Entity documents, ownership records, and organizational agreements if investing through a trust, LLC, or other entity structure

Qualified purchaser documentation is significantly more complex than accredited investor documentation. The definition of "investments" requires careful classification and, for many investors, legal analysis. Working with a CPA or attorney who understands the difference between qualifying investment assets and non-qualifying assets is important.

A well-organized balance-sheet summary that clearly separates your investment assets from personal and business operating assets gives the verifier a faster starting point. It also reduces the chance of a misclassification that delays your fund subscription.

For investors with significant equity positions from past exits, the classification of assets can interact with tax planning strategies. See our article on Section 1202 and qualified small business stock for relevant context.

Common Mistakes

- Treating net worth and investments as interchangeable: Net worth includes your primary residence. Qualified purchaser "investments" does not. Many investors assume they qualify when their $5M+ figure is largely home equity.

- Assuming all private deals use the same standard: Accredited investor status is enough for many deals. Qualified purchaser status is required for 3(c)(7) funds. The deal structure determines the standard, and you cannot substitute one for the other.

- Assuming one successful verification transfers to another deal: Each fund and issuer makes its own determination. A letter or subscription representation that satisfied one issuer is not automatically accepted by another.

- Underestimating entity and trust complexity: Trusts have specific rules depending on their structure. LLCs and partnerships have their own analysis. Do not assume your entity qualifies without a specific review.

- Confusing qualified purchaser with qualified client: Qualified client is a third standard under the Investment Advisers Act, used for performance fee arrangements. The three terms, accredited investor, qualified purchaser, and qualified client, are not interchangeable and apply in different contexts.

Where Kubera’s Proof of Wealth Fits

Whether you are preparing for accredited investor verification or qualified purchaser documentation, the common thread is organized, current, clearly labeled financial records. The cleaner your documentation, the faster the professional review.

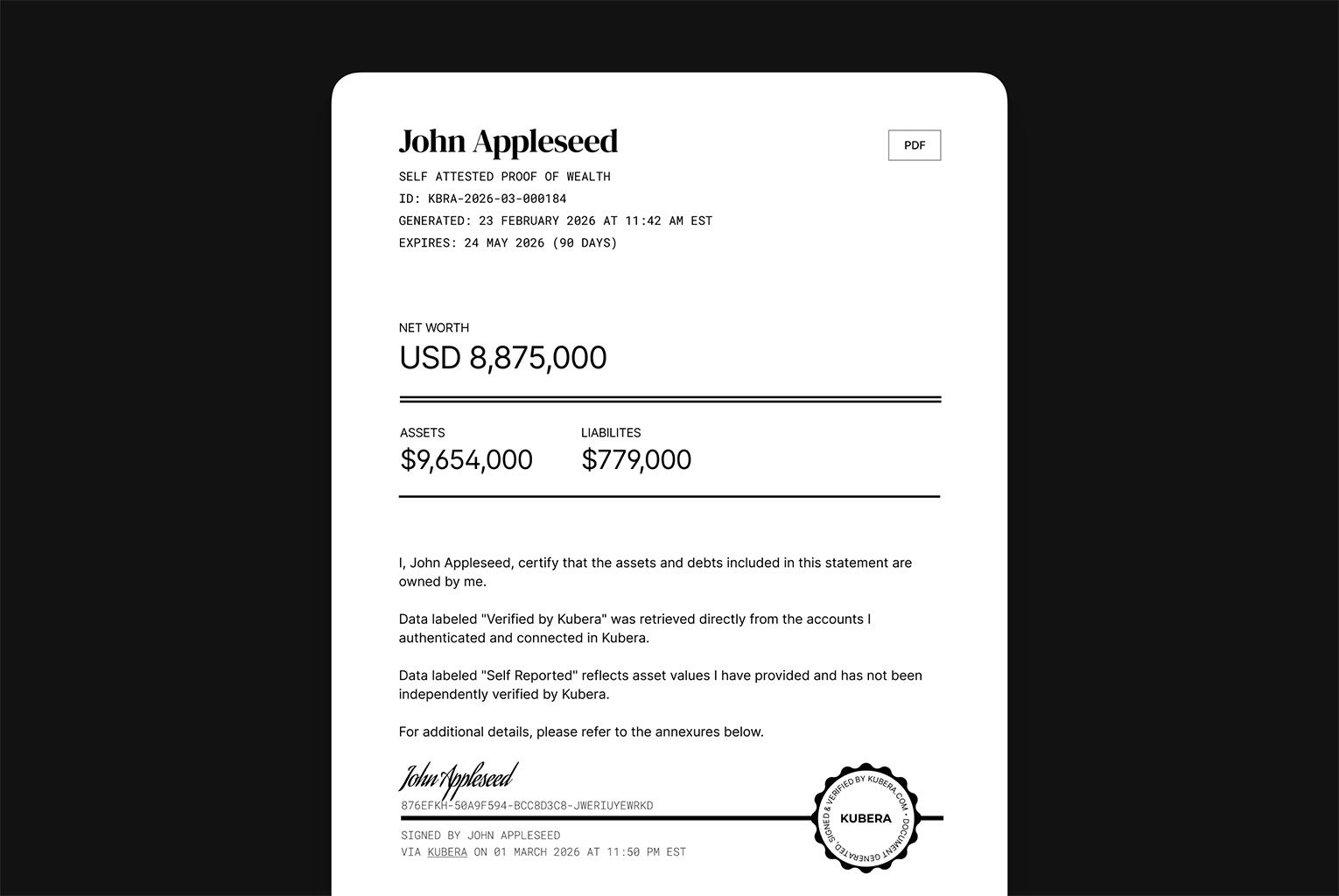

Kubera’s Proof of Wealth generates a signed, dated, shareable snapshot of your financial position from connected accounts. This can serve as a starting package for the CPA, attorney, or adviser who handles the legal determination. It does not determine either legal status. That is a determination made by issuers and their counsel. But it reduces the time you spend assembling supporting documentation. Learn more at kubera.com/proof-of-wealth.

Frequently Asked Questions

Is a qualified purchaser the same as an accredited investor?

No. They are two separate legal standards defined under two separate federal laws. The accredited investor standard comes from the Securities Act. The qualified purchaser standard comes from the Investment Company Act. They apply in different contexts. Meeting the accredited investor standard does not automatically mean you meet the qualified purchaser standard.

Which is harder to qualify for?

Qualified purchaser is significantly more difficult. The $5 million in investments threshold for a natural person is substantially higher than the $1 million net worth threshold for accredited investors, and the qualified purchaser standard uses a narrower definition of "investments" that excludes primary residence and certain business assets.

Does the March 2025 Rule 506(c) guidance affect qualified purchaser status?

No. The March 2025 no-action letter addressed verification procedures for certain Rule 506(c) offerings under Regulation D. It does not change the qualified purchaser standard, the definition of "investments" under the Investment Company Act, or the documentation requirements for funds relying on Section 3(c)(7) exemptions.

What counts as investments for qualified purchaser status?

Investments generally include securities, real estate held for investment purposes (not primary residence), commodity interests, and cash equivalents held for investment. They generally exclude the primary residence, personal property, and business assets where the person actively operates the business. The rules are complex and situation-specific. Consult a securities attorney for analysis of your specific assets.

Can an LLC or trust qualify as a qualified purchaser?

Yes, under specific conditions. A trust may qualify if the trustee and all beneficiaries are qualified purchasers. A company may qualify if all equity owners are qualified purchasers or if the company owns at least $25 million in investments. Entity qualification requires case-by-case legal analysis.

Why does one fund ask for more documents than another?

The documentation requirement reflects the fund's structure and the legal standard in use. A 3(c)(7) fund requires qualified purchaser status and demands detailed investment documentation. A 3(c)(1) fund or a Regulation D offering using the accredited investor standard typically requires less. The fund structure drives the requirement.

Do I need a CPA or attorney letter for qualified purchaser status?

Not always, but the complexity of the qualified purchaser analysis often warrants professional support. Unlike accredited investor verification under 506(c), there is no specific safe-harbor list of third-party verifiers in the Investment Company Act for qualified purchaser determinations. Fund managers typically rely on investor representations in subscription documents, sometimes supplemented by a review of supporting financial statements. Ask the fund's administrator what they require.

Track your investment assets in Kubera

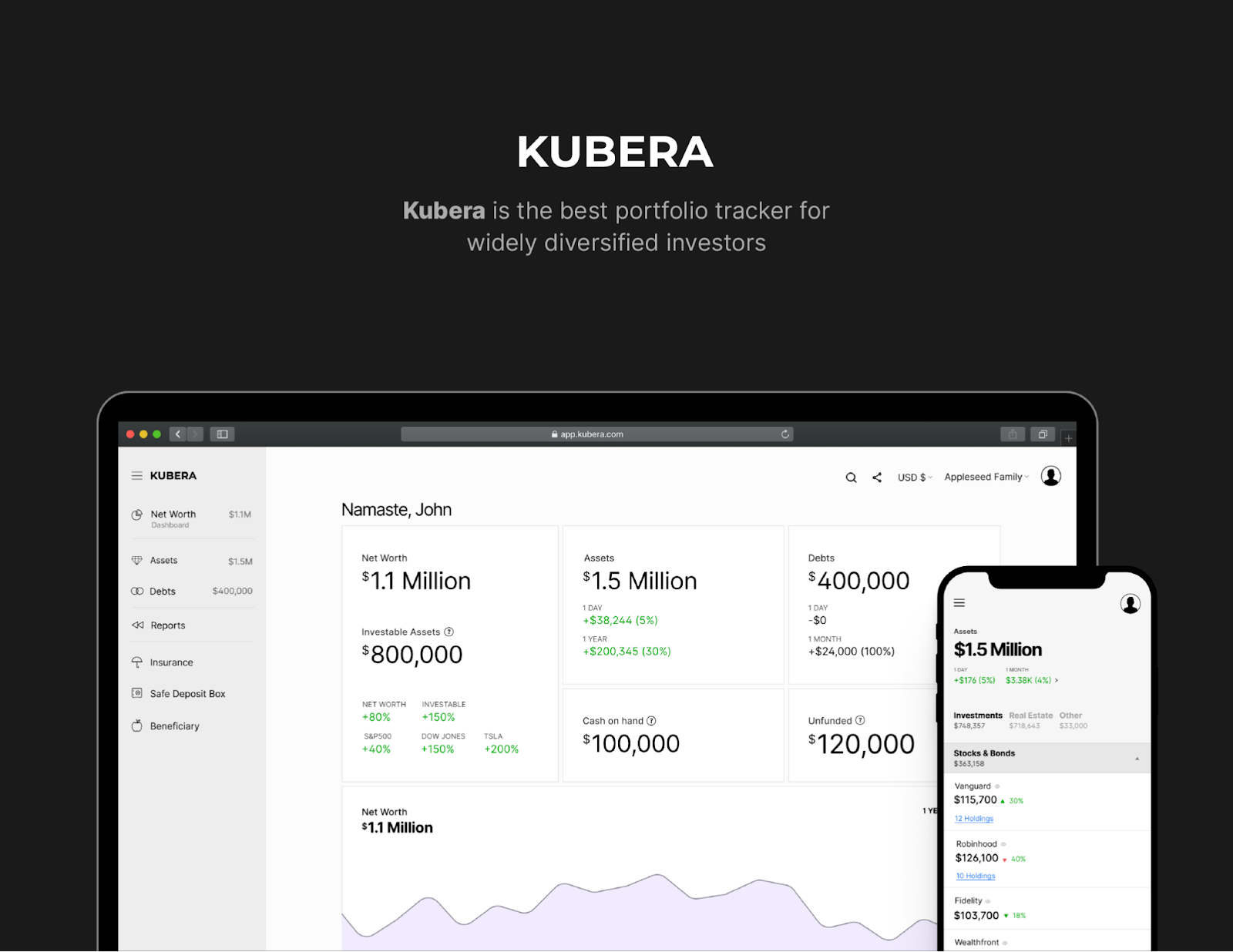

Kubera connects and tracks investment accounts, private holdings, real estate, and other assets in one organized view. Generate a shareable financial snapshot to share with your CPA or attorney before fund subscriptions.

Track your full balance sheet in Kubera →

Disclaimer: This article is for informational purposes only and does not constitute legal or investment advice. Qualified purchaser and accredited investor standards involve complex legal analysis under separate federal statutes. Consult a qualified securities attorney for guidance specific to your situation and any investment you are considering.