If you invest in private deals, you've been through the drill. A fund asks you to prove you're accredited. So you dig up two years of tax returns, or ask your CPA to write an accredited investor letter, or hand over bank statements to a third-party verification service. It takes days. Sometimes weeks. It costs money. And it happens again for the next deal, because the last verification expired.

In March 2025, the SEC's Division of Corporation Finance issued a no-action letter that provides a clearer path for rule 506(c) accredited investor verification in certain high-minimum offerings. Not all of them. But enough to matter.

This post explains what the guidance said, what it means in practice, and what to do when someone still asks you for an accredited investor letter.

First, some context: 506(b) vs 506(c)

Most private placements in the US raise money under Regulation D — specifically Rule 506(c) under Regulation D or its sibling Rule 506(b) — which exempts them from registering with the SEC. Within Reg D, there are two paths that matter:

Rule 506(b) is the traditional route. The fund can't advertise publicly — it relies on existing relationships to find investors. In exchange, the verification standard is more lenient: the fund needs a "reasonable belief" that you're accredited. In practice, issuers typically gather substantive information about investors — through questionnaires, pre-existing relationships, or other contextual knowledge — that supports that belief. The bar is lower than 506(c), but it isn't a formality.

Rule 506(c) was created in 2013 as part of the JOBS Act. It allows investment funds to advertise publicly — run ads, post on social media, speak at conferences about specific investment opportunities. The tradeoff: the fund must take "reasonable steps" toward verifying accredited investor status for every purchaser. A questionnaire alone isn't enough.

This verification process is one major reason 506(c) has remained much smaller than 506(b). Despite being available for over a decade, the vast majority of private capital — roughly $2.7 trillion in 2023 — was still raised under 506(b). Only about $169 billion used 506(c). Fund managers avoided it because the verification required was expensive, invasive, and scared away investors who didn't want to hand over personal financial documents.

The SEC provided a non-exclusive list of acceptable methods for rule 506(c) verification: reviewing IRS forms for income verification, reviewing bank statements showing net worth alongside a credit report, and obtaining written confirmation from a registered broker-dealer, registered investment adviser, licensed attorney, or CPA. These methods worked. They were also miserable for everyone involved.

What changed in March 2025

On March 12, 2025, the SEC's Division of Corporation Finance issued a no-action letter in response to a request from Latham & Watkins LLP, providing interpretive guidance on verifying accredited investor status under Rule 506(c) under Regulation D.

Important framing first. A no-action letter reflects the views of SEC staff, not the Commission itself. The letter explicitly states it "is not a rule, regulation, or statement of the Commission" and "has no legal force or effect." It does not amend Rule 506(c). What it does is tell issuers that, in the specific fact pattern presented, staff would not recommend enforcement action — which in practice gives fund managers and their counsel a clear, defensible path to follow.

With that understood, here's what the guidance established: if certain conditions are met, an issuer can satisfy the rule 506(c) verification requirement through a combination of high minimum investment amount and written investor representations — without collecting financial documents.

Staff agreed that an issuer could reasonably conclude it has taken "reasonable steps" toward verifying accredited investor status if three conditions are met:

- Minimum investment thresholds. The investor commits at least $200,000 for natural persons or $1,000,000 for legal entities. The size of the commitment was part of what supported the staff's analysis in the fact pattern presented.

- Written representations. The investor provides a written statement that (a) they are an accredited investor, and (b) the investment is not financed by a third party for the purpose of meeting the minimum. This can be in a subscription agreement, a standalone document, or a written electronic communication.

- No contrary knowledge. The issuer has no actual knowledge of facts suggesting the investor isn't accredited or that the investment is being financed by a third party.

No tax returns. No bank statements. No accredited investor letter. No third-party service — provided the issuer and its counsel are comfortable relying on this path.

What this means in practice

For investors in some 506(c) private placements with a minimum investment amount of $200K or more, you may no longer need to provide financial documents, if the issuer chooses to rely on the March 2025 staff guidance and all other conditions are met. If a fund still asks for your tax returns, you or your attorney can point them to the no-action letter — though the fund is not required to adopt this path.

For fund managers, this removes the single biggest friction point in the rule 506(c) verification process. You can now advertise publicly and use a streamlined approach, as long as you maintain appropriate minimum investment amounts and the other conditions in the guidance are satisfied. The guidance also noted this can apply mid-offering: if you're running a 506(b) deal and want to switch to 506(c) to begin advertising, you can do so if the 506(c) conditions are met and Form D is amended.

For third-party verification services, their value proposition got narrower for high-minimum private placements where issuers choose to rely on the new guidance. They remain relevant for offerings where traditional verification is still required.

What did NOT change

The March 2025 guidance addressed one specific scenario within one specific rule. Everything else remains the same.

506(b) deals are unchanged. The "reasonable belief" standard still applies. The new guidance doesn't affect these deals because they never required the document-heavy verification process that 506(c) did.

506(c) deals below the thresholds are unchanged. If a private placement has a minimum investment amount below $200,000 for natural persons or $1,000,000 for legal entities, the old rule 506(c) verification rules still apply.

Qualified purchaser status is completely unaffected — and it's worth understanding how qualified purchaser vs accredited investor differ as standards.

An accredited investor typically needs $1M in net worth excluding primary residence, or annual income of $200,000 or more. A qualified purchaser is a higher bar under a different law entirely — it requires $5 million or more in investments, generally including securities and investment real estate, but not a primary residence or property used in a business, subject to certain exceptions. Accredited investor status is defined under the Securities Act of 1933. Qualified purchaser status is defined under Section 2(a)(51) of the Investment Company Act of 1940. The March 2025 guidance addressed only the former. For funds relying on Section 3(c)(7) exemptions, issuers must have a reasonable belief that investors meet the $5M investments threshold — the March 2025 letter does not change that analysis.

Issuer discretion remains. The guidance establishes what staff considers an acceptable path — not a ceiling. Fund managers and their counsel can always require more, and many conservative practitioners will continue requesting traditional documentation while the guidance is relatively new.

State-level requirements may still apply. Both 506(b) and 506(c) are preempted from state securities registration, but states can still require notice filings and fees.

Non-US requirements are unaffected. Investment funds raising from investors in the EU or UK still need to comply with local rules, including the Alternative Investment Fund Managers Directive.

The CPA letter question

Here's the practical scenario many investors face: a fund or its counsel asks for an accredited investor letter confirming your status. What do you do?

If it's a 506(b) deal: An accredited investor letter was never required. The reasonable belief standard applies, and issuers typically satisfy it through questionnaires and the context of their existing relationship with the investor.

If it's a 506(c) deal with a $200K+ minimum investment amount: Under the March 2025 guidance, your written representation may be sufficient, if the issuer chooses to rely on that path and all conditions are met. You can point the fund's counsel to the no-action letter. But this is one acceptable approach, not the only one — fund managers can still require more.

If it's a 506(c) deal below $200K: Traditional rule 506(c) verification still applies. An accredited investor letter, tax returns, bank statements, and third-party verification services are all accepted methods.

If the fund requires qualified purchaser status: The qualified purchaser vs accredited investor distinction matters here. The March 2025 guidance addresses only accredited investor verification and doesn't help with qualified purchaser analysis. The fund needs a reasonable basis to believe you hold $5M+ in qualifying investments, which typically involves reviewing private investments and other account statements.

If the counterparty insists on an accredited investor letter regardless: That's their right. The guidance sets a floor, not a ceiling. Often the fastest path is to comply rather than argue.

But here's the thing: getting that accredited investor letter doesn't have to be the ordeal it used to be.

The real bottleneck was never the rules

Whether a deal requires an accredited investor letter, bank statements, or just a signed representation, the pain point for most high-net-worth individuals has always been the same: assembling the information.

You have accounts at multiple institutions. Real estate that isn't in any brokerage account. Private investments that exist as PDFs in your email. Crypto across multiple wallets. Pulling all of this together into a coherent proof of wealth — every time someone asks — is the real cost.

The March 2025 guidance helps in specific cases. But it doesn't eliminate the fundamental problem: when someone asks you to prove your wealth, you need to be able to show them.

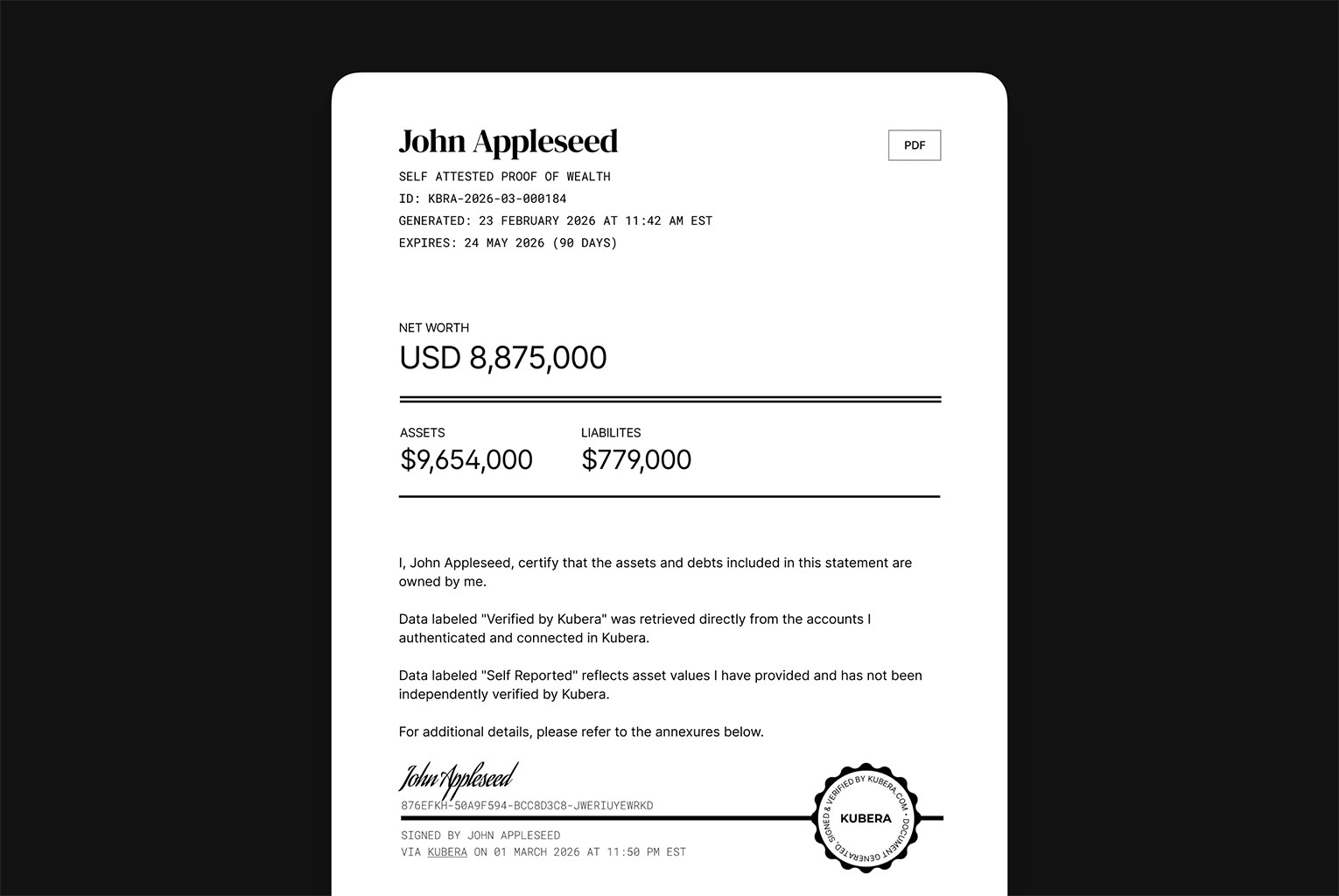

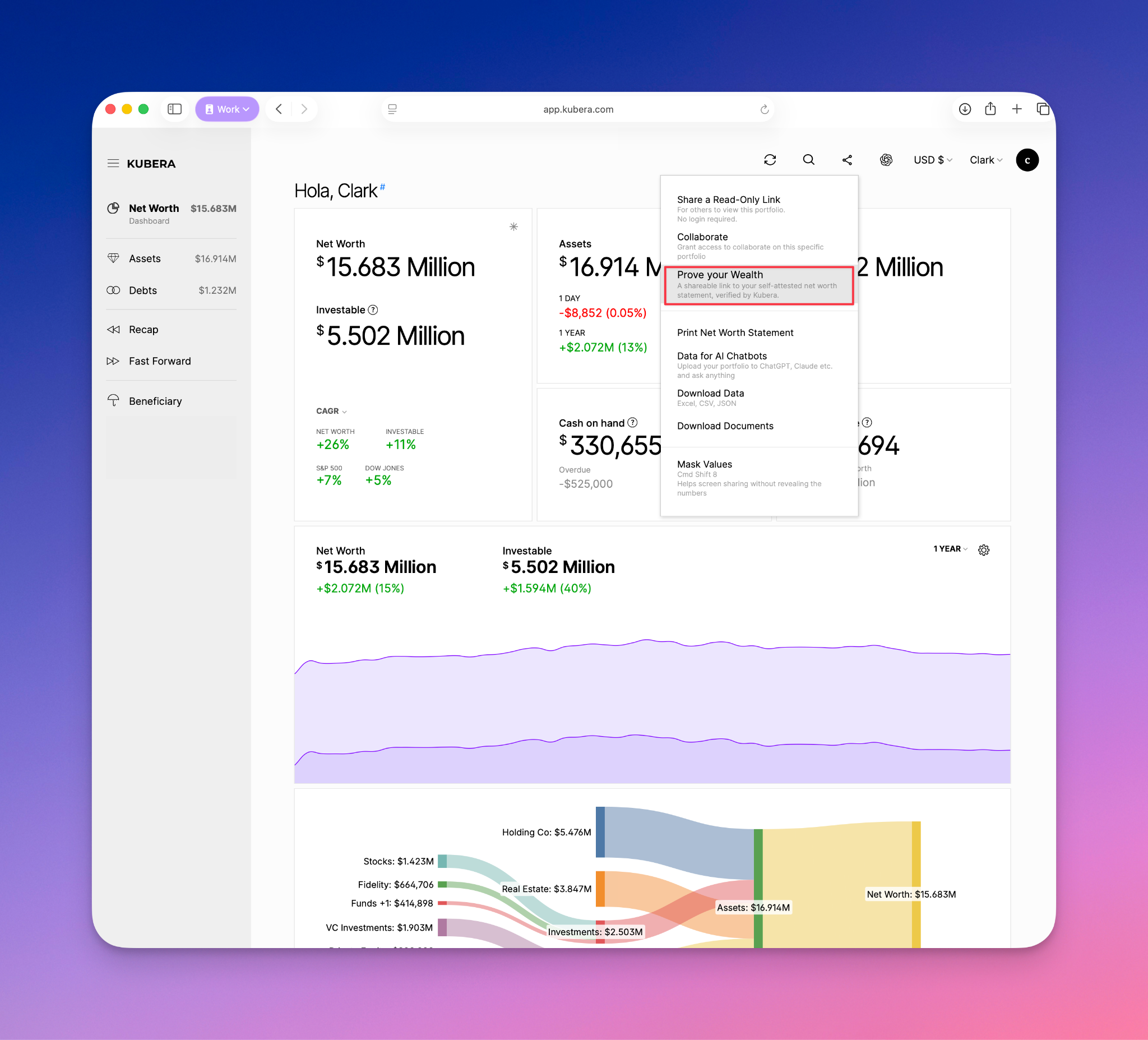

This is why we built Kubera's Proof of Wealth. Connect your accounts once. When you need proof of wealth, select what to include, sign with one tap, and share a secure link (Kubera Dashboard → Share icon → Prove your Wealth). Connected account data is pulled directly from institutional connections. Manual entries — real estate, private investments, art — are clearly labeled as self-reported. The recipient sees everything, transparently distinguished, and makes their own judgment.

Kubera's Proof of Wealth is not a legal determination. It doesn't replace issuer judgment, fund counsel review, or CPA sign-off. Its value is operational: it gives whoever is asking a structured, signed, timestamped snapshot of your financial position — so they can do their job faster, and you can stop hunting down statements.

When an accredited investor letter is still required, you send the link to your CPA. They can often move faster because the information is already assembled. When a fund just needs a clear picture of your holdings, it's already there.

The guidance is getting clearer. Your proof of wealth should match.

Quick reference

This post is for informational purposes only and is not legal, tax, accounting, or investment advice. Whether any proof or verification method is sufficient for a specific offering depends on the applicable requirements and the judgment of the issuer and its counsel. Kubera's Proof of Wealth is a documentation and sharing tool. It does not determine whether any recipient's diligence requirements have been satisfied.