What Is an Accredited Investor Letter?

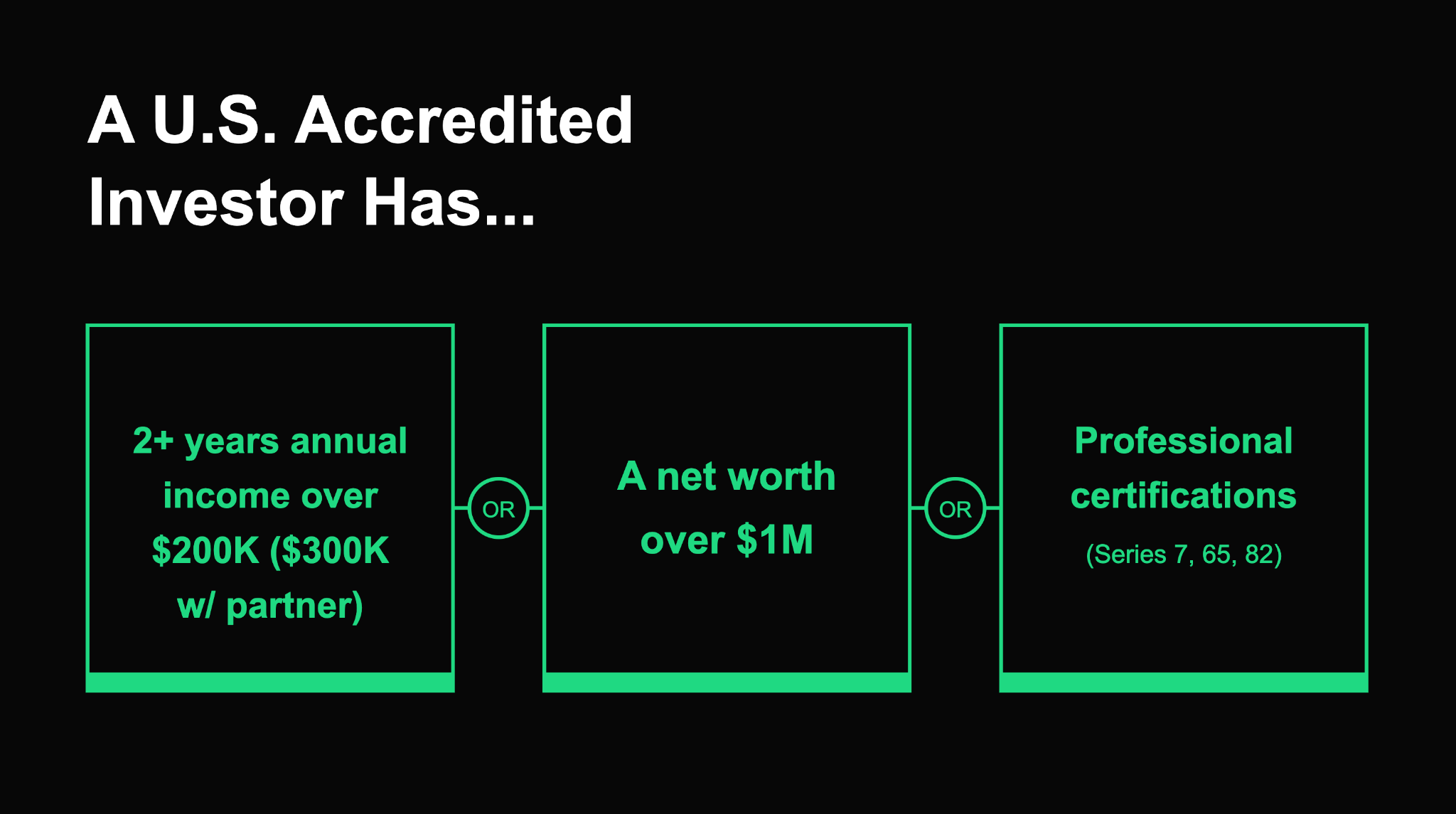

An accredited investor letter is a document issued by a licensed professional that confirms you qualify as an accredited investor under SEC rules. The SEC defines an accredited investor as someone who meets specific income, net worth, or professional-credential thresholds.

You may also see this document called an accredited investor verification letter. Both terms refer to the same thing: a signed, dated statement from a qualified third party that you have the financial standing to participate in certain private offerings.

There is no government agency that issues an accredited investor certificate. The SEC does not send you a card or a license number. Instead, federal securities law places the responsibility for verification on the issuer. When you invest in a private placement or private fund that requires accredited investor status, the issuer needs documented evidence that you qualify. That evidence is the letter.

The letter itself does not grant you any legal status. It documents what a professional has verified after reviewing your financial records. Think of it as accredited investor proof that you give to the issuer rather than something you hold permanently.

When Do You Need an Accredited Investor Letter?

Not every private investment triggers the same verification requirement. The answer depends on the offering structure.

Rule 506(c) offerings

Issuers raising money under Rule 506(c) of Regulation D must take "reasonable steps" to verify that all purchasers are accredited investors. A third-party letter from a CPA, attorney, broker-dealer, or registered investment adviser is the most common way to satisfy that requirement. For more detail on how this rule works, see our article on Rule 506(c) accredited investor verification.

Hedge funds and private funds

Many private funds structured under Section 3(c)(1) of the Investment Company Act rely on the accredited investor standard to limit their investor base to 100 or fewer beneficial owners. Fund subscription documents typically require written representations or a third-party letter before you can invest.

Pre-IPO platforms and secondary transactions

Platforms that facilitate secondary sales of private company shares typically require accredited investor verification before you can participate. Verification requirements differ by platform. Some accept self-certifications. Others require a formal letter. See our guide to pre-IPO liquidity and our overview of EquityZen alternatives for context on how different platforms approach verification.

Subscription packages and platform onboarding

When you sign subscription documents for any private investment, the subscription package usually includes an accredited investor representation. Some platforms ask for it once at onboarding while others require updated verification for each new offering. Always confirm the current requirement before assuming a previous letter is still valid.

Investors who have recently experienced a liquidity event often encounter multiple verification requests in a short period as they deploy capital into private markets.

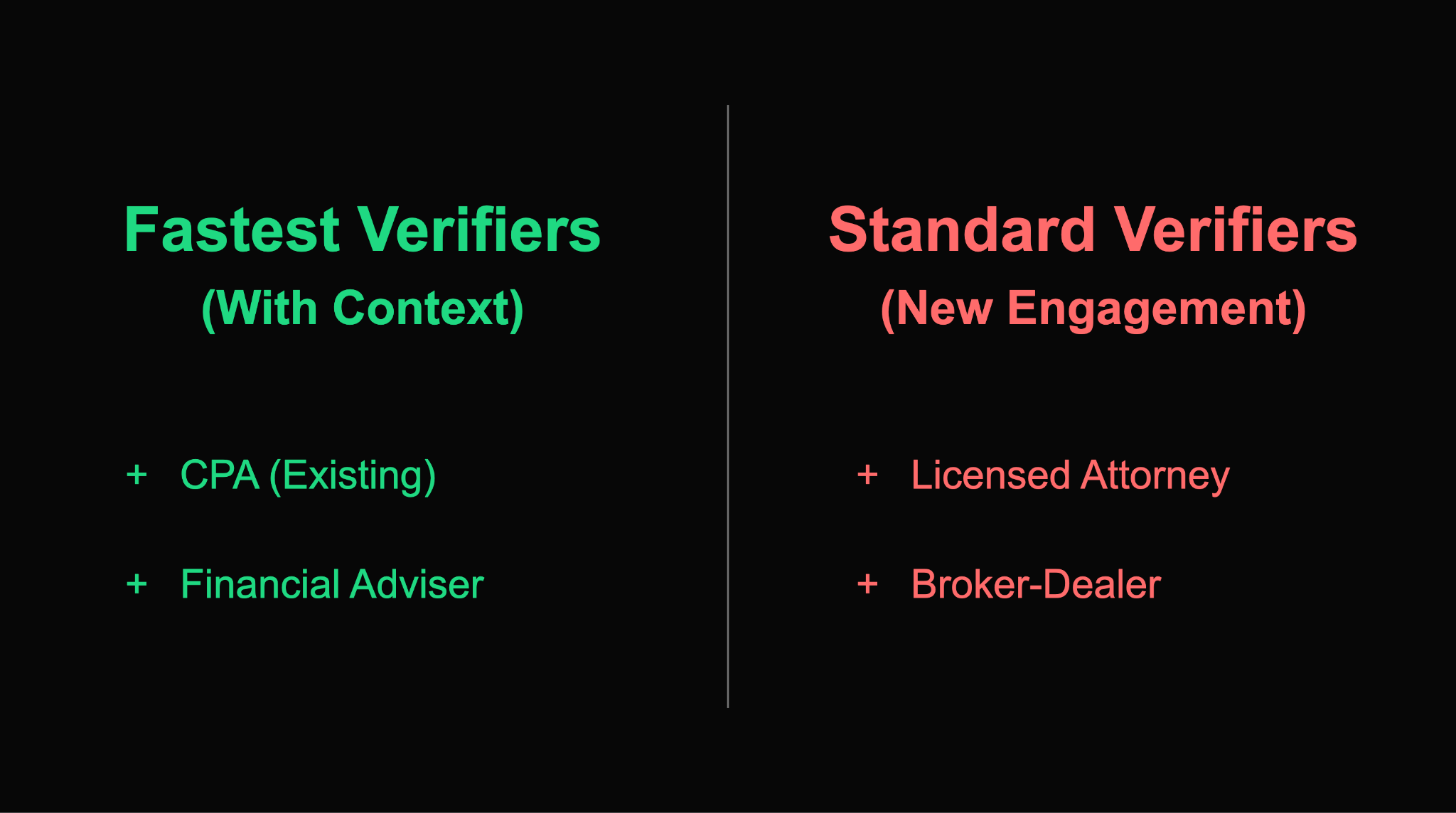

Who Can Issue an Accredited Investor Letter?

The SEC's guidance on third-party verification for Rule 506(c) offerings identifies four categories of professionals who can issue a valid letter. Understanding who can issue an accredited investor letter helps you choose the fastest and most cost-effective path.

1. CPA

A CPA letter for accredited investor qualification is one of the most common options. A licensed CPA reviews your tax returns, W-2s, K-1s, bank statements, or brokerage statements and writes a signed letter confirming that you meet the income requirement or the net worth requirement. If you already work with a CPA, they are typically the fastest starting point because they have your records on file.

2. Attorney

An attorney letter for accredited investor verification works the same way. A licensed attorney in good standing reviews your financial information and provides a signed confirmation. Some investors prefer an attorney if they also need legal review of subscription documents at the same time. This approach combines two steps into one engagement.

3. Broker-dealer

A registered broker-dealer can provide verification based on their customer-of-record information. If your primary investment accounts are held at one firm, the firm may offer verification services for clients. Contact your account representative to ask whether this is available.

4. Registered investment adviser

An SEC-registered or state-registered investment adviser who manages a portion of your assets can also issue a letter. If your financial adviser already has a comprehensive view of your finances, this can be the quickest path. The adviser signs based on their actual knowledge of your financial position.

Limits of self-certification

Some platforms accept written self-certifications, particularly private funds structured under Section 3(c)(1) of the Investment Company Act. However, Rule 506(c) issuers are explicitly required to verify investor status independently. A simple "I certify that I am an accredited investor" signature does not satisfy the "reasonable steps" standard for most 506(c) offerings. The March 2025 guidance created a narrow exception for high-minimum offerings, which is discussed in the section below.

What Documents Do You Usually Need to Prepare?

The documents you need depend on which qualification path you use: income-based, net worth-based, or professional license.

Income-based qualification

- Federal tax returns for the two most recent years (Form 1040, W-2s, K-1s, Schedule C if self-employed)

- Pay stubs or an employment verification letter if income has changed this year

- Documentation of bonus, commission, or other variable income if relevant

Net worth-based qualification

- Bank and brokerage statements dated within 90 days, showing balances and account ownership

- Investment account statements across every account you are including in the net worth calculation

- Documentation of real estate assets held for investment (not your primary residence)

- Mortgage statements, credit card balances, and any outstanding loan documentation to establish liabilities

- Trust or entity documents if any assets are held outside your personal name

When you contact a CPA or attorney, arrive with a balance-sheet-style summary showing assets, liabilities, and net worth as of a specific date. Attaching individual statements to that summary makes the review faster. Professionals spend less time chasing records, and the letter arrives sooner. Organized financial records directly reduce the cost and turnaround time of getting accredited investor proof.

How Did the March 2025 Rule 506(c) Guidance Change the Conversation?

In March 2025, the SEC staff published a no-action letter that addressed verification procedures in a specific subset of Rule 506(c) offerings.

The guidance allows certain issuers to rely primarily on written investor representations rather than third-party verification letters, but only when the following conditions are met:

- The offering has a minimum investment of $200,000 or more per investor

- The issuer has no actual knowledge contradicting the investor's representations

- Other reasonable steps are taken in combination with the representations

What this guidance does not do:

- It does not apply universally to all Rule 506(c) offerings

- It does not remove the verification obligation from issuers in lower-minimum offerings

- It does not change the qualified purchaser standard, which is a separate legal framework

- It does not mean every platform or fund will accept written representations instead of a third-party letter

Most issuers and platforms have not changed their procedures as a result of this guidance. If you are investing in a high-minimum offering, ask the issuer or their counsel directly whether they are relying on written representations. When in doubt, prepare a traditional third-party letter. For a complete breakdown, see our dedicated article on Rule 506(c) accredited investor verification.

How Much Does an Accredited Investor Letter Cost?

Costs vary by professional, the complexity of your finances, and your existing relationship with the verifier.

Timing depends heavily on how organized your documentation is. A CPA with your returns on file can often turn around a letter in three to five business days. An attorney engaged for the first time may take one to two weeks. During tax season (February through April), expect longer wait times.

How to Prepare Faster

Follow these steps before you contact a verifier. Each step reduces the time your professional spends on the engagement.

- Compile all financial documentation before reaching out. Have returns, W-2s, K-1s, and statements ready to share. Do not wait until after you make contact.

- Build a balance-sheet summary. List assets with institution names and account types. List liabilities. State the net worth figure as of a specific date. One page works.

- Choose your verifier based on your existing relationships. Your current CPA or financial adviser will work faster than a new engagement because they already have context.

- Share securely. Avoid emailing unprotected PDFs containing full account numbers and sensitive data. Use a secure portal or a shareable link with access controls.

- Request the letter before the deal closes, not the day before. Build in at least two weeks of lead time. Rush requests rarely produce faster results and often add cost.

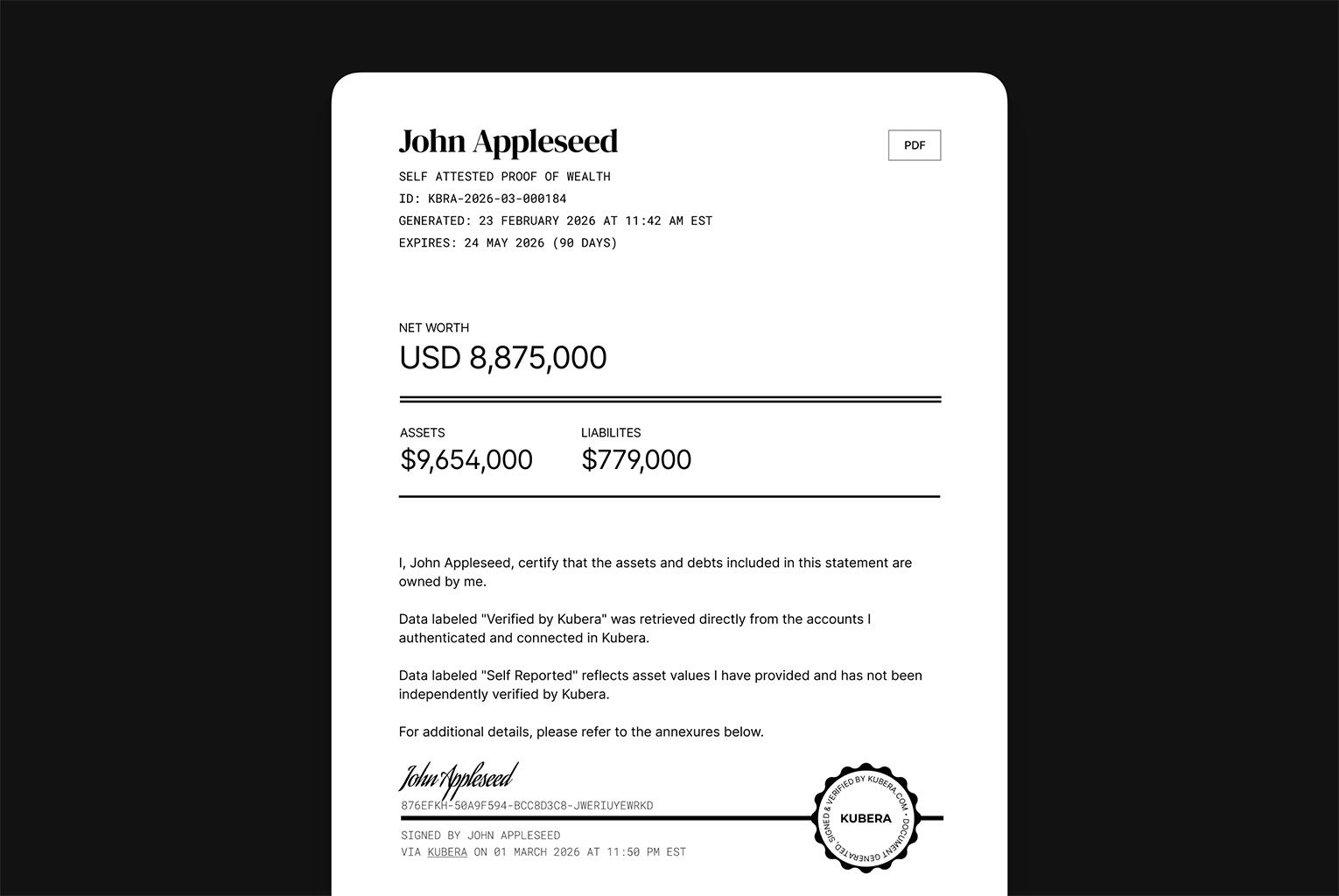

Kubera’s Proof of Wealth helps with steps one through four. It generates a signed, dated, shareable proof-of-wealth package from your connected accounts. You can share it with your CPA or attorney as the organized financial snapshot they need to begin their review. Kubera Proof does not determine accredited investor status. That determination belongs to the issuer and their counsel. But it replaces hours of manual document assembly. See how it works here.

Common Mistakes

- Assuming there is one universal form. There is no standard accredited investor letter template. Different verifiers write letters differently. Different issuers have different requirements. Always ask the issuer what they accept before you commission a letter.

- Waiting until the deal is live. Last-minute requests delay closings and add stress. Start the process when you know you are interested, not when you are ready to sign.

- Sending unorganized screenshots. A folder of phone-camera images of account screens is not professional documentation. Verifiers need dated, complete, institution-branded statements with your name on them.

- Assuming qualified purchaser is the same as accredited investor. These are two distinct legal standards. Some funds require qualified purchaser status, which has a $5 million investments threshold. Accredited investor status is not enough for those funds.

- Assuming one platform's process is the same as another's. A letter that satisfied one issuer may not satisfy another. The fund's legal counsel sets requirements, and those differ across offerings.

- Assuming your letter stays valid indefinitely. Most letters expire after 90 days. Active private-market investors should plan for regular refreshes.

Frequently Asked Questions

Is an accredited investor letter required?

It depends on the offering structure. Rule 506(c) issuers must take reasonable steps to verify accredited investor status, and a third-party letter is one accepted method. Rule 506(b) offerings allow self-certification. Some platforms accept written representations under certain conditions. Always confirm the specific requirement with the issuer or platform you are using.

Can a CPA write an accredited investor letter?

Yes. A CPA letter for accredited investor qualification is one of the most common verification approaches. Licensed CPAs are explicitly recognized as qualified third-party verifiers under SEC guidance for Rule 506(c) offerings. If you already work with a CPA, contact them first.

Can I verify myself as an accredited investor?

Self-certification is accepted in some contexts, including many private funds under Section 3(c)(1). But Rule 506(c) issuers are generally required to take independent verification steps and cannot rely on self-certification alone. The March 2025 no-action guidance carved out a limited exception for high-minimum offerings meeting specific conditions. When in doubt, ask the issuer.

How long is an accredited investor letter valid?

Most issuers treat letters as valid for 90 days from the date of issuance. Some platforms extend that to six months. Always confirm the freshness requirement with the issuer before submitting a letter you received for an earlier transaction.

What is the difference between an accredited investor letter and proof of funds?

An accredited investor letter confirms that you meet the legal threshold to participate in certain private offerings. Proof of funds shows that you have available liquid capital for a specific transaction, such as a real estate purchase. They serve different purposes. Some private transactions require elements of both.

What if I qualify by net worth instead of income?

Both qualification paths work equally well. For net worth-based qualification, the verifier reviews asset and liability documentation rather than income records. The $1 million net worth threshold excludes the value of your primary residence. A clean balance-sheet summary with supporting account statements is particularly useful for the net worth path.

What if I invest through an LLC or trust?

Entities can qualify as accredited investors under their own standards. An LLC or similar entity may qualify if all equity owners are accredited investors, or if the entity holds total assets above the applicable threshold. Trusts and other entity structures have specific rules that go beyond individual verification. Entity verification requires organizational documents and evidence of ownership in addition to financial statements. Consult a securities attorney for entity situations.

Create your Proof of Wealth

Kubera connects your bank accounts, brokerage accounts, and other assets in one place. Generate a signed, dated, shareable proof package to share with your CPA or attorney before accredited investor verification.

Get started with Kubera Proof →

Disclaimer: This article is for informational purposes only and does not constitute legal or investment advice. Accredited investor verification requirements vary by offering type, issuer, and platform. Consult a qualified attorney or financial adviser for guidance on your specific situation.