For many startup employees and founders, the hardest part of equity is not earning it. It is living with a large asset that looks valuable on paper but does not yet behave like money. In simple terms, pre-IPO liquidity refers to the ways shareholders can turn private equity into cash before an IPO or acquisition. While these paths can be incredibly useful, they rarely feel simple in real life.

A person may need cash for an option exercise, a tax bill, a home purchase, or basic diversification. At the same time, selling too early can mean accepting a discount, giving up future upside, or damaging a tax benefit that would have mattered more later. That is why monetizing private shares works best when it is treated as a holistic planning decision, rather than just a transactional afterthought.

What Is Pre-IPO Liquidity?

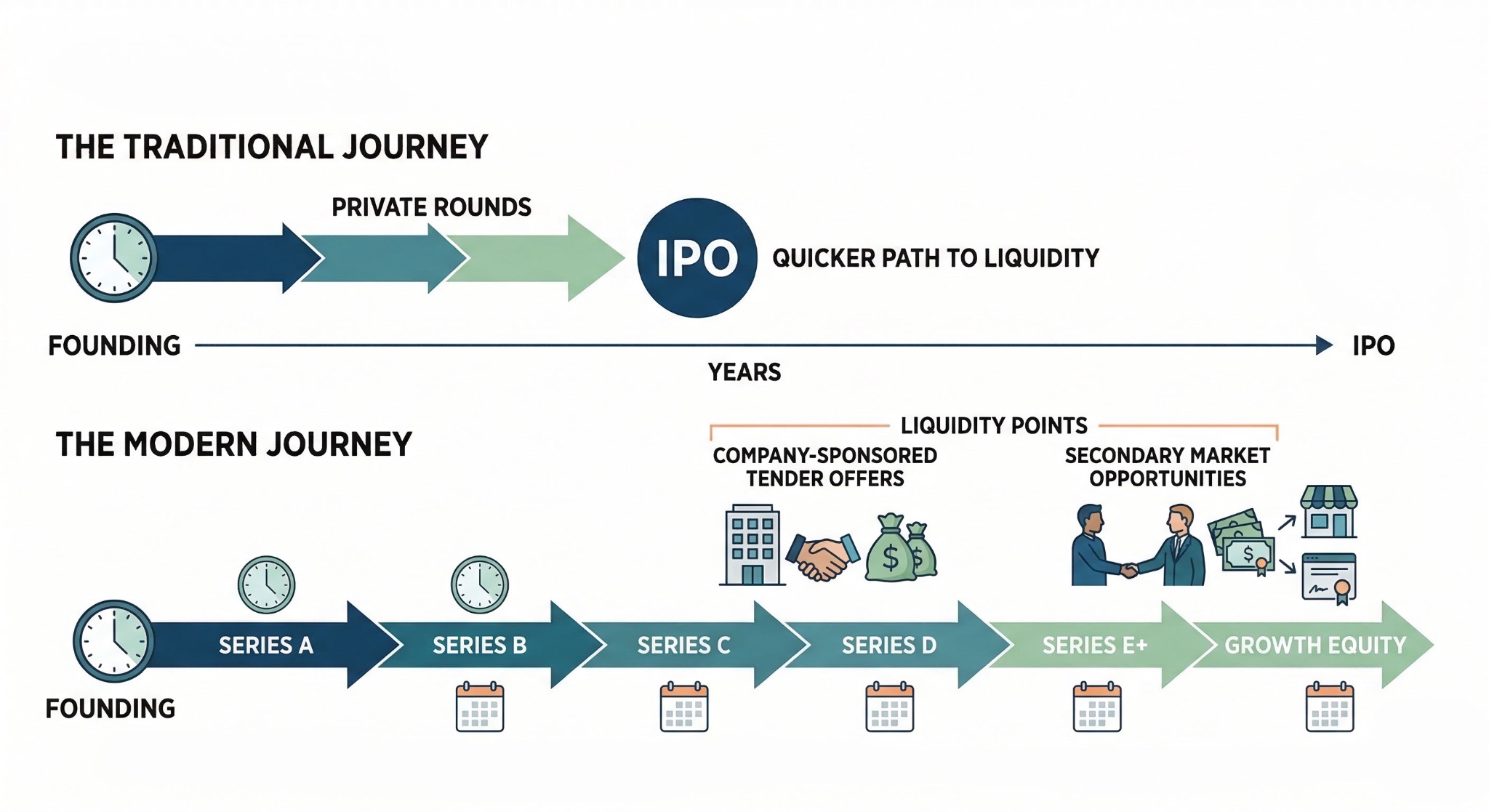

Pre-IPO liquidity is the umbrella term for transactions that let holders of private company shares or options access value before the company goes public. Historically, most people simply waited for a sale of the company or a public listing. That model made perfect sense when startups moved from founding to IPO relatively quickly.

Today, however, many strong companies stay private for years longer than earlier generations did. The rise of late-stage venture capital, abundant growth equity, and looser shareholder-count rules, such as the JOBS Act increasing the private reporting threshold from 500 to 2,000 shareholders, have significantly reduced the pressure to enter public markets. For people on the cap table, that means a much longer period in which equity compensation can dominate a household balance sheet without becoming spendable cash.

This extended delay creates real financial tension. A founder may be extraordinarily wealthy on paper while remaining essentially cash poor. Similarly, a tenured employee might have enough vested equity to fundamentally change their net worth, but lack the liquid assets required to exercise their options comfortably.

This tension often peaks when a departing employee faces a short 90-day post-termination exercise window (PTEW) and has to decide quickly whether to invest more of their own cash into an already concentrated position. In each of these cases, the central question is not simply whether the stock has value. It is whether any of that value can be accessed on acceptable, risk-adjusted terms.

Why Pre-IPO Liquidity Matters More Now

For employees, the issue is often concentration. It is common for startup equity to represent a very large share of net worth, especially for early employees who accepted lower cash pay in exchange for upside. In a normal portfolio discussion, that level of single-company exposure would look extreme. In startup life, it often becomes normal by accident.

The second issue is time. Vesting may finish in four years, but the company can remain private for another six, eight, or ten. During that stretch, people still need to make decisions about housing, taxes, education funding, and career changes. Articles like Value of Unvested Stock Options and Stock Options Tax resonate because they speak to a problem many shareholders already feel: the equity may be meaningful, but it does not yet solve the cash-flow problems in front of them.

Companies have their own reasons to support structured liquidity. A thoughtful tender offer can help retain long-tenured employees, reduce pressure for a premature IPO, and keep control over who owns the stock. It can also clean up the cap table, which becomes more valuable as the shareholder base grows and old grants become operationally messy.

The Main Pre-IPO Liquidity Paths

The core mistake people make here is treating every liquidity option as if it solved the same problem. It does not. A tender offer, a direct sale, and an option financing arrangement may all create cash, but they do it in different ways and with very different consequences.

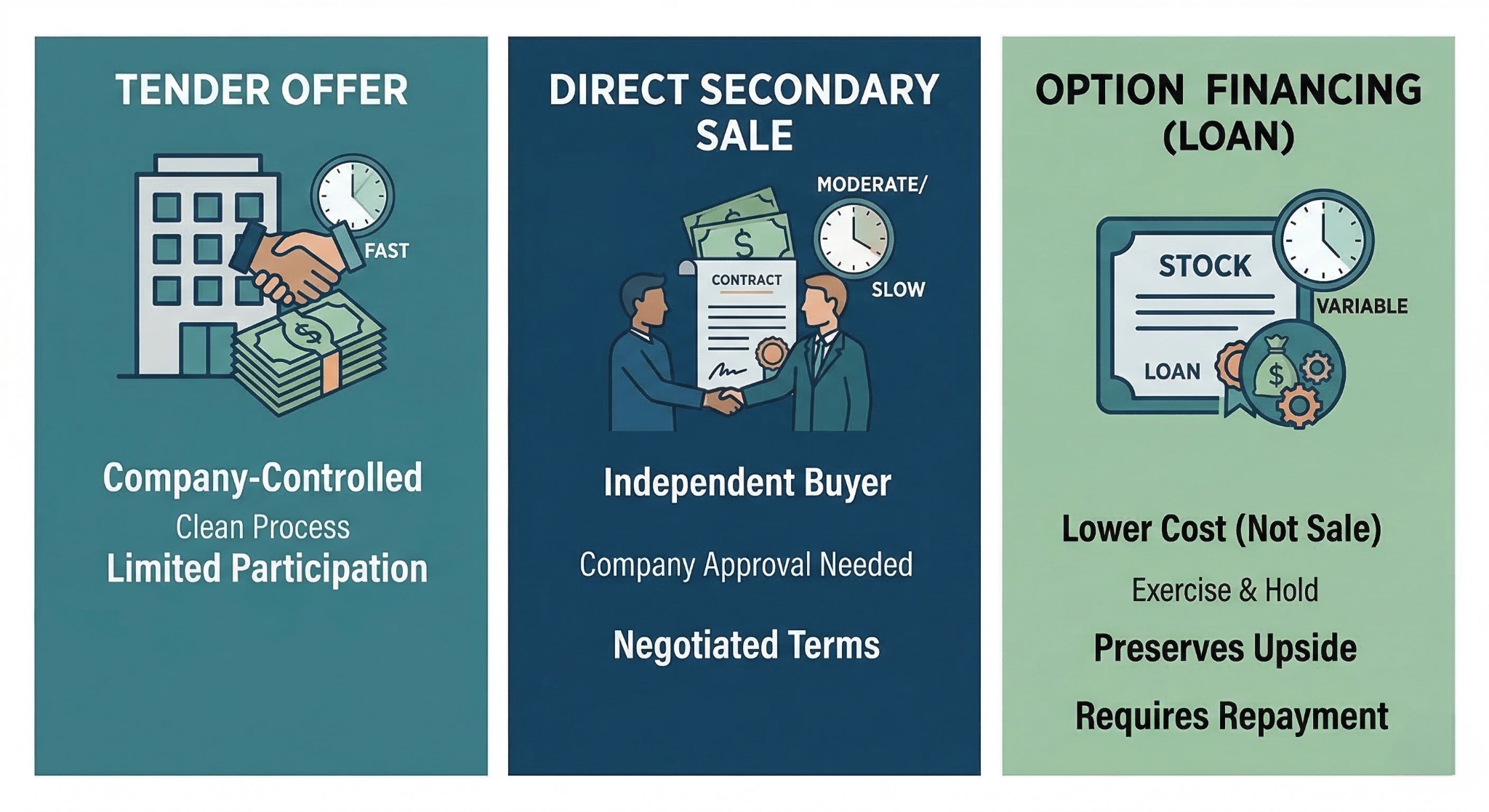

Company-Sponsored Tender Offers: The Cleanest Path to Cash

A company-sponsored tender offer is the cleanest pre-IPO liquidity path most employees will ever see. The company sets the price, decides who can participate, limits how much each person can sell, and either repurchases the shares itself or brings in an approved outside buyer. That structure removes much of the transaction friction that makes ad hoc private sales difficult.

The tradeoff is control. If the company offers a tender, you usually do not negotiate much. You may only be allowed to sell 10 to 20 percent of vested holdings, and the pricing may come in below the most recent preferred round. Still, for many holders, a tender offer is attractive because it combines speed, clarity, and company approval in one process.

A common example looks like this: an employee who joined eight years ago has most of her net worth tied to one company, plus a meaningful tax bill from earlier exercises. She does not need to sell everything. She needs enough liquidity to reduce pressure. A tender offer that lets her sell a modest portion of vested shares may be a very good answer even if the price is not perfect.

Direct Secondary Sales: Navigating Friction and Restrictions

A direct secondary sale happens when an individual shareholder finds a buyer and negotiates terms outside a company-run program. This is usually what people mean when they say they want to sell private company stock. In practice, the process is more constrained than the phrase suggests.

Most companies impose transfer restrictions, require board approval, and reserve a right of first refusal, or ROFR. That means the company can step in and buy the shares on the same terms you negotiated with an outside buyer. Even when the company does not exercise that right, it still may slow the process or reject the transfer.

Pricing also tends to disappoint first-time sellers. A buyer in a private transaction is taking on illiquidity, limited information, and timing risk. That buyer often expects a discount to the last financing round or even to the most recent 409A valuation. Anyone comparing a direct sale price with an imagined IPO price is usually comparing two very different things.

The Pre-IPO Secondary Market: Structure Without Guaranteed Liquidity

The pre-ipo secondary market has become more organized over the last decade, but it is still not a public market in miniature. Platforms such as Forge, Hiive, EquityZen, and Nasdaq Private Market can help match buyers and sellers, verify accredited investor status, and move paperwork along. They can make a hard process more orderly. They do not remove the company’s control over the transaction.

This matters because many sellers assume a marketplace creates liquidity by itself. It does not. Buyer demand still varies sharply by company, transaction timelines can stretch, and the final price may still reflect a meaningful discount for risk and illiquidity.

If you are trying to understand the likely range, comparing a 409A valuation with actual bid levels is often more useful than looking at headlines about what a company might someday be worth. That is one reason pieces like Pre-IPO Stock Value and EquityZen Alternatives are useful reference points when you start evaluating bids.

How to Cash Out Stock Options Before IPO: Timing and Tax Sequencing

Many people asking how to cash out stock options before ipo are really asking two separate questions. First, can I get liquidity from these options at all? Second, if I can, what sequence creates the least damage on taxes and future upside?

In most cases, the options themselves are not what gets sold. The holder usually needs to exercise first, participate in a tender offer that permits sale treatment tied to option exercises, or use outside capital to fund the exercise and wait for a later exit. That makes the problem less about finding a buyer and more about managing timing, strike price, tax exposure, and company rules.

This is where the details matter. A low strike price and a modest 409A value can make an early exercise look reasonable. A high spread can make the same move dangerous, especially if the holder does not fully understand the AMT risk on incentive stock option exercises or the payroll and ordinary income consequences tied to non-qualified stock options (NSOs). The right answer often depends on whether the exercise cost is manageable without borrowing and whether the shareholder genuinely wants more exposure to the company.

Financing and Lending Solutions: Managing the Cost of Capital

Some shareholders do not want to sell immediately but still need cash. Others want to exercise options and hold the stock, yet lack the capital to do so. That is where stock option exercise financing and lending solutions enter the discussion.

Specialty firms can fund the option exercise and recover their money at a later liquidity event. Some structures are non-recourse or close to it, which means the provider is taking much of the downside risk if the company fails. That sounds attractive, and in some cases it is. The cost, however, can be high enough that it meaningfully reshapes the economics of the eventual win.

Loans secured by private shares also exist, especially for later-stage companies with clearer valuation support and a more credible path to liquidity. But lenders are cautious for good reason. The collateral is illiquid, transfer restrictions may apply, and downside scenarios are hard to manage. These arrangements can help solve a timing problem. They do not remove concentration risk.

Complex Structures

Large shareholders at late-stage companies sometimes explore prepaid variable forwards or similar derivative structures. These are specialized tools, not mainstream employee solutions. They usually require a large position, sophisticated legal advice, tax analysis, and a company whose governing documents allow them.

When these structures appear in articles, they can sound elegant. In practice, they are narrow tools for narrow situations. Most employees and smaller shareholders do not need to start there.

Key Risks and Considerations

Tax Treatment: The Hidden Costs of Early Liquidity

Taxes shape almost every pre-IPO liquidity decision. Shares held long enough may qualify for long-term capital gains treatment. Option exercises can create ordinary income, Alternative Minimum Tax (AMT) exposure, or both. State taxes can change the outcome again, especially for shareholders who have moved across states while the equity was vesting or being exercised.

The point is not that taxes should paralyze the decision. It is that they often change the ranking of the options. A transaction that looks attractive before tax can look mediocre after tax. A sale that solves today’s cash need can also destroy a larger future benefit, especially if the stock might qualify for QSBS treatment under Section 1202.

A familiar pattern is the employee who exercises ISOs late in the year after a strong valuation step-up, assumes the problem is solved, and then discovers an AMT bill that was far larger than expected. That is why Stock Options Tax, 83(b) Election, and even pieces like Should I Sell My RSUs When They Vest become relevant in the broader planning conversation. The issue is rarely one tax rule in isolation. It is the combined effect of several.

Valuation and Opportunity Cost: Bridging the Price Gap

Private-market pricing is messy because the company is not marked continuously by a public market. One buyer may be willing to pay a price close to the last preferred round. Another may insist on a substantial discount. Both may be rational, because each buyer is underwriting different risks.

Imagine your company’s latest 409A value is $5 per share, but a real buyer in a secondary process is only willing to pay $3.50. That gap does not automatically mean the buyer is wrong or predatory. It may simply reflect illiquidity, limited access to company information, transfer friction, and uncertainty around when the company goes public. The seller still has to decide whether solving a real-life need today matters more than holding out for a cleaner future event.

There is also the risk of selling too much. A partial sale that reduces concentration can be smart. A large sale that eliminates meaningful upside just before the company compounds further can feel terrible in hindsight. The right amount is often more important than the decision to sell at all.

Legal and Contractual Constraints: The Fine Print of Illiquidity

Most holders underestimate how restrictive the documents can be. Private company stock is not designed to trade freely. ROFR provisions, co-sale rights, transfer restrictions, board approval requirements, blackout periods, and confidential information rules all affect what is possible.

That is especially true for current employees and insiders. Someone who has regular access to material nonpublic information (MNPI) may be restricted from selling even when a buyer exists and the company is open to transfers in principle. In other words, the practical question is not just whether the documents allow a sale. It is whether the timing, the facts, and the information environment allow one.

Tracking and Managing Private Company Equity

Private equity can become the largest asset on a household balance sheet while remaining the least organized. Holdings may sit across old grant letters, spreadsheets, equity portals, emails, PDF valuation reports, and half-remembered exercise confirmations. That becomes a problem the moment a shareholder needs to make a fast decision.

This is not just an administrative annoyance. Missing a post-termination exercise window can permanently destroy value. Forgetting which lots were exercised when can weaken tax planning. Not having immediate access to share counts, cost basis, vesting status, and supporting documents can slow a tender-offer response or weaken a discussion with a CPA, attorney, or wealth advisor. That is one reason Wealth Management Tips for Founders matters well beyond investment allocation. Organization is part of the strategy.

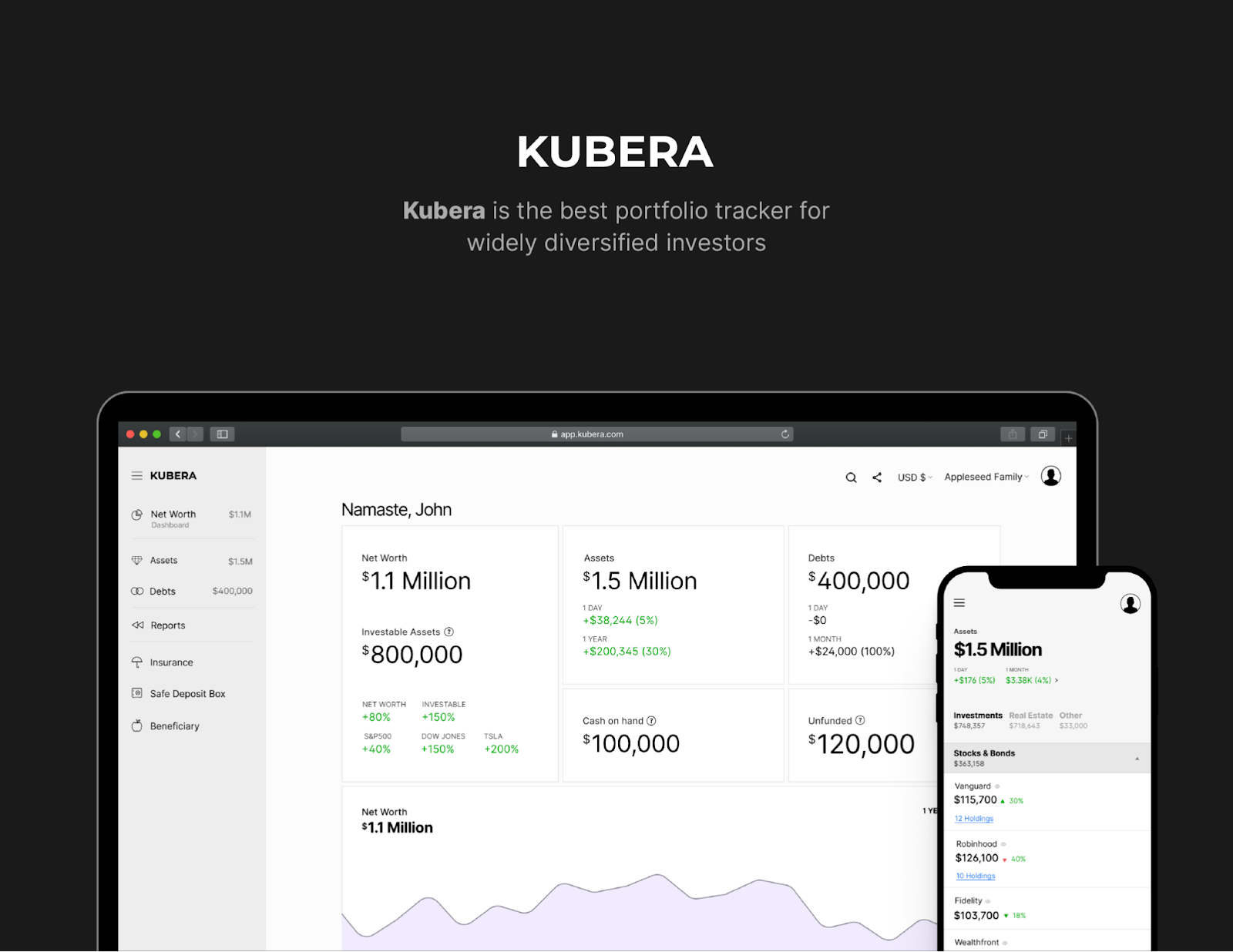

How Kubera Simplifies Pre-IPO Equity Management

Most traditional portfolio tools ignore private company stock or treat it as a rough placeholder value. That may be enough for a casual net worth snapshot. It is not enough when private-company equity is one of the most important assets on the balance sheet.

Kubera helps by giving shareholders one place to track private holdings, unvested and vested equity, updated valuations, documents, and deadlines. You can store grant letters, 409A reports, stock purchase agreements, and tender materials; track cost basis across grants and exercises; model how concentrated your balance sheet is in one company; and share the picture with an advisor when the time comes to act.

That makes the product useful in a restrained, operational way. It does not eliminate transfer restrictions or make a tender offer appear. But what it does is reduce the chaos that often leads to rushed decisions.

Take control of your pre-IPO stocks along with your complete wealth portfolio today. Try Kubera free for 14 days (no credit card required).

Frequently Asked Questions

Can I sell private company shares before an IPO?

Often, yes, but only if the company documents and processes allow it. Most transactions still require company approval, and many are subject to ROFR or other transfer restrictions.

What is the difference between a tender offer and a direct secondary sale?

A tender offer is company coordinated, with set pricing and eligibility rules. A direct secondary sale is negotiated independently and usually involves more friction, less certainty, and more dependence on company approval.

Can I use the pre-IPO secondary market to sell startup equity before IPO?

Sometimes, especially if the company is well known and buyers are active. But a marketplace does not create automatic liquidity, and many transactions still depend on the company’s approval and the buyer’s accredited investor status.

What if I need cash mainly to exercise options?

Then the best path may not be an immediate sale. It may be an early exercise, a tender-offer participation decision, or a financing structure that funds the exercise while you preserve some upside.

Do taxes matter even if I only sell a small portion?

Yes. A small sale can still trigger meaningful capital gains, ordinary income issues, AMT considerations, or lost QSBS opportunities.

Should I sell everything once I get a chance?

Usually not. For many shareholders, the best answer is a partial sale that reduces concentration and solves a real cash need while preserving meaningful upside.

Conclusion

Pre IPO liquidity is no longer a niche topic for venture insiders. It has become a practical planning question for founders, executives, early employees, and investors whose wealth sits in private company shares for longer than it once did. The tools are real, but so are the tradeoffs.

The best decision is rarely the one that maximizes a headline price in isolation. It is the one that fits the tax facts, the concentration risk, the company rules, and the life problem you are actually trying to solve. People usually get into trouble here when they make a rushed decision with scattered information, not when they take the time to understand what they own and what each path really costs.