A concentrated stock position can be a sign of success, but it also creates a planning problem that many investors underestimate. The issue is not just volatility. One holding can begin to drive your net worth, your liquidity, your tax bill, and in some cases your future income at the same time.

This is especially common for founders, senior employees, and households with large grants of company stock. It also shows up after an inheritance, a business sale, or a long period of outperformance in a single name. Whatever the source, the real question is not whether the stock is good. It is how much of your financial plan depends on one company continuing to go right.

What Is a Concentrated Stock Position?

A concentrated stock position exists when one stock has become large relative to the rest of your portfolio. Many advisors become more concerned once a single name exceeds 10 percent of investable assets. At that point, the portfolio is no longer being driven mainly by asset allocation. It is being driven by one security.

That threshold is not a rule of nature. A household with substantial outside wealth, limited dependence on the company, and high risk tolerance can sometimes carry more. A household whose salary, bonus, and future grants all come from the same employer may need to act much sooner. That is why single stock concentration risk has to be evaluated in context rather than by headline percentage alone.

Common Sources of Concentrated Positions

The most common source is equity compensation. RSUs, stock options, and employee stock purchase plans (ESPPs) can build a large position gradually, almost quietly, because each grant or purchase feels manageable on its own. Over several years, the combined exposure can become substantial.

Other common sources include founder equity, inherited stock, legacy positions with very low basis, business sale proceeds, and portfolio drift. In practice, many investors do not make an active decision to concentrate. They simply do not interrupt the process early enough.

How Concentrated Positions Develop

At growth companies, concentration often builds because equity arrives on a schedule while the underlying shares appreciate faster than the rest of the balance sheet. A few large vesting years can change a household allocation much more than people expect.

RSUs deserve special attention because rsu concentration risk is often disguised as compensation planning rather than portfolio planning. Employees focus on vest dates, withholding, and blackout windows, but the larger issue is that vested shares keep adding to an already correlated position unless there is a policy for selling or transferring them.

Inherited stock creates a different kind of inertia. The obstacle is often emotional rather than analytical. A family position may carry identity, loyalty, or memory, which makes reducing it feel more consequential than reducing any other holding.

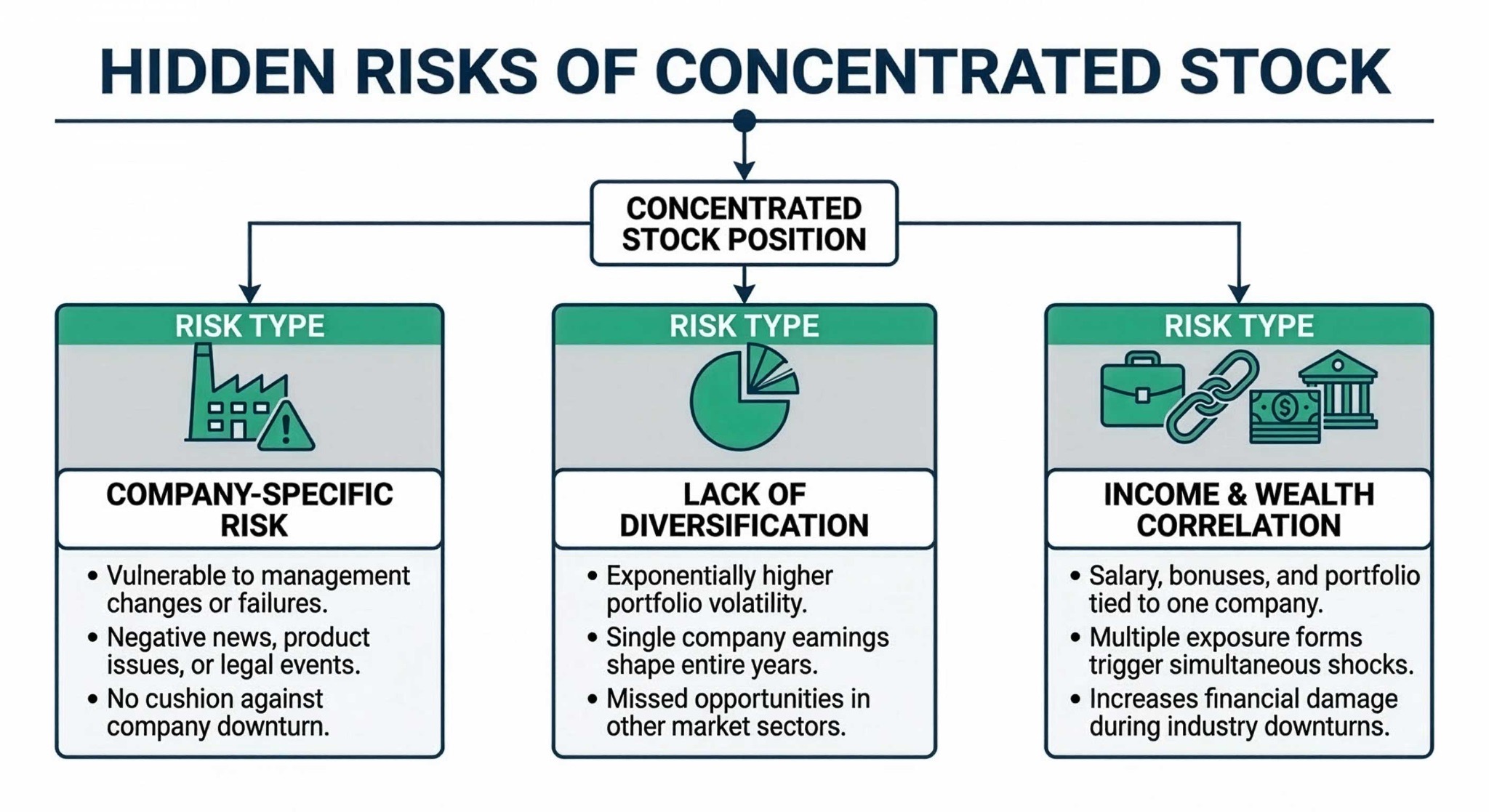

The Hidden Risks of Concentrated Stock Positions

Company-Specific Risk

The first risk is obvious but still underweighted in real-world decision making. A single company can disappoint for reasons that have nothing to do with the broader market. Management changes, litigation, regulation, product failure, margin pressure, or a shift in industry structure can all damage a stock that once looked durable.

That is the essence of concentrated stock risk. Historical data makes this concrete: between 1987 and April 2024, roughly 67% of individual stocks underperformed the Russell 3000 index, and over 40% of Russell 3000 companies experienced catastrophic stock price losses of 70% or more from 1980 to 2021. Broad equity markets have many ways to recover from a weak quarter or a challenged sector. A single company has far fewer ways out. When the position is large enough, a problem in one boardroom becomes a household balance sheet event.

While the precise figures change by study, the planning lesson is stable: single-name exposure carries a very different risk profile from diversified equity exposure.

Lack of Diversification

Diversification does not eliminate losses, but it changes the source of those losses. In a diversified portfolio, outcomes are spread across many companies, sectors, and cash flow streams. In a concentrated position, one earnings call or one guidance revision can reshape your entire year.

This is why concentrated stock diversification strategies matter even for investors who remain bullish on the underlying business. The objective is not always to abandon conviction. Often the objective is to reduce the cost of being wrong.

Income and Wealth Correlation

For employees and executives, the more serious problem may be correlation between human capital and financial capital. If salary, bonus, unvested grants, and existing shares all depend on one company, the household has multiple forms of exposure to the same single company.

That can turn a routine company setback into a combined income shock, liquidity shock, and portfolio shock. In those cases, a financial plan should measure not only the value of vested shares but also the degree to which future earnings depend on that same issuer.

Why Tracking Your Concentrated Position Is Critical

Concentration is not static. It changes with market movement, new grants, exercises, vesting, sales, and transfers. A position that looked manageable at the start of the year can become dominant after a rally or after a large vesting cycle.

The mechanics matter. Cost basis may differ by lot. Holding periods may differ by lot. Some shares may be freely tradable while others are subject to blackout periods, lockups, insider trading policies, or transfer restrictions. Without a current inventory of those details, investors make decisions with incomplete information.

A good tracking process should show the current percentage of net worth tied to the name, the embedded gain by lot, the holding period of each lot, and the next expected liquidity or vesting event. That is the operating dashboard for a concentrated stock position.

Tax Implications of Managing Concentrated Stock

Capital Gains Considerations

Tax is usually the reason investors hesitate to reduce concentration, and sometimes with good reason. Selling appreciated shares can trigger a large tax bill, especially when the position has compounded for years at a low basis.

But tax cost should be compared with risk cost. Paying tax efficiently is important. Treating the tax bill as a reason to do nothing is different. In many cases, the right question is whether the household is being adequately compensated for continuing to run the risk.

The answer may differ by lot. Some lots may be suitable for sale now, others may be better held until they cross the long-term threshold, and some may be better reserved for charitable giving, family transfers, or estate planning. That is why tax planning should be done lot by lot rather than at the account level.

Illustrative tax framework. Actual rates, surtaxes, and state rules vary. Investors should confirm the current rules with a tax professional before acting.

Equity Compensation Tax Issues

With company equity, tax implications vary by instrument. RSUs are generally taxed as ordinary income when they vest. Non-qualified stock options create ordinary income on exercise. Incentive stock options may preserve capital gains treatment in the right fact pattern, but they can also create alternative minimum tax exposure and a more complicated cash planning problem.

Investors with company stock inside a qualified plan may also need to evaluate net unrealized appreciation treatment. That is a narrower planning tool, but when it applies, the tax difference can be meaningful. These are decisions to model with a tax professional before execution, not after.

Tax-Managed Strategies

Tax-managed implementation can materially improve the result. Tax loss harvesting, gifting, charitable transfers, staged liquidation, and lot-specific sales are all examples of ways to reduce concentration without ignoring taxes.

The point is not to eliminate tax entirely. The point is to align sale timing, deductions, losses, and charitable intent so the household can reduce risk in a tax efficient way. For many investors, that is the bridge between knowing they should diversify and actually doing it.

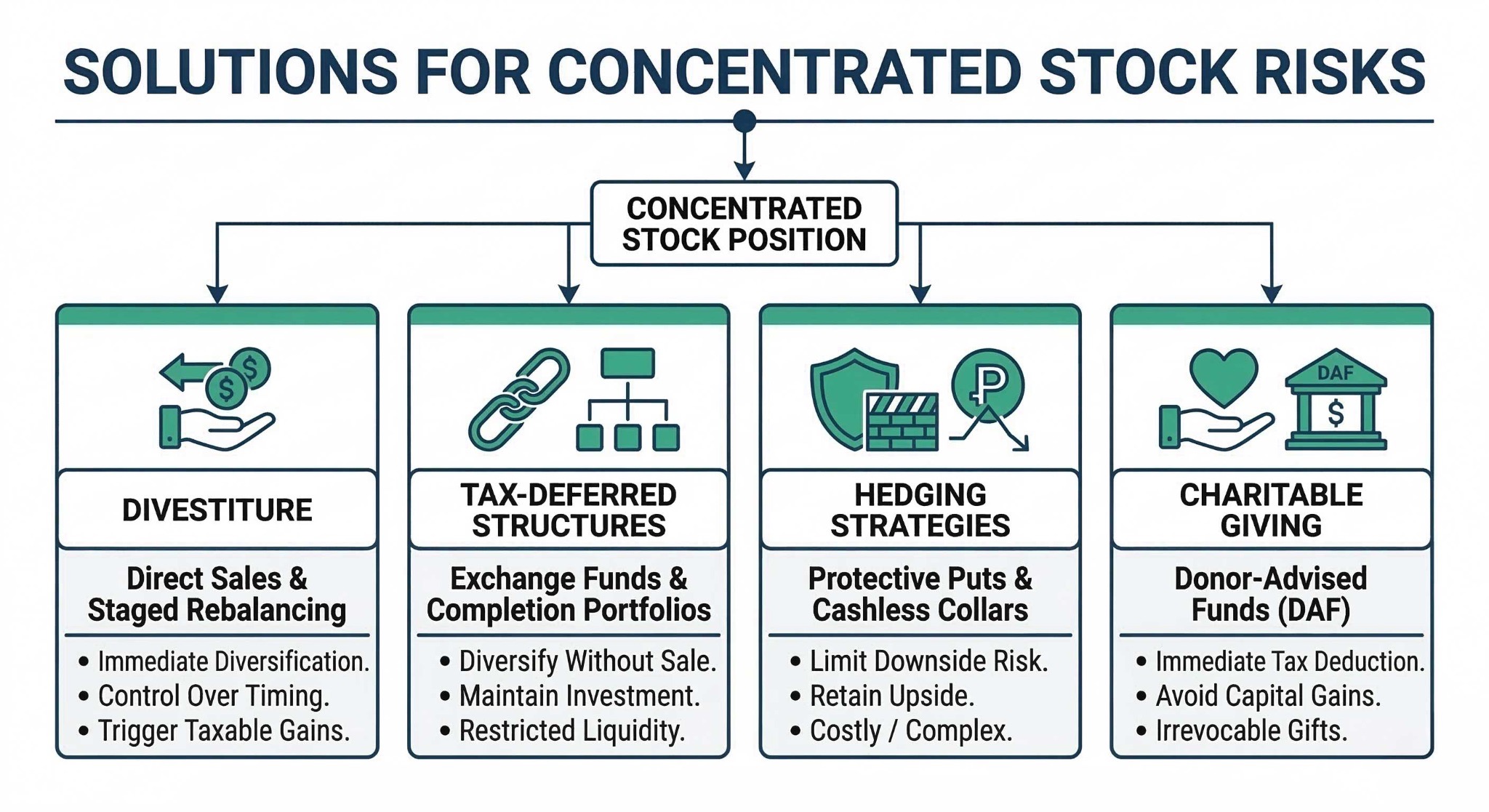

Strategic Approaches to Managing Concentrated Positions

Direct Liquidation Strategies

The simplest approach is usually the most underused: sell some shares on purpose and repeat. A pre-committed selling schedule can reduce concentration, lower the temptation to market time, and make the tax bill more manageable across calendar years.

For insiders, a Rule 10b5-1 trading plan may be the cleanest structure because it sets the terms in advance and reduces the number of judgment calls during trading windows. For many households, this is still the most reliable answer to how to diversify a concentrated stock position.

Portfolio Rebalancing

A portfolio policy can define the maximum target weight for any single name and the conditions that trigger trimming. This is one of the most practical concentrated stock diversification strategies because it turns a difficult identity-laden decision into a repeatable investment rule.

Hedging and Options Strategies

Options can reduce downside risk or create a more controlled exit path, but they are not free and they are not simple. Protective puts, collars, and other structures can be useful for very large positions, especially when immediate sale is unattractive for tax or control reasons.

These strategies need to be evaluated carefully because the costs, tax implications, and liquidity terms can materially affect the outcome. Hedging is often useful, but it should not be treated as a magic substitute for broader diversification.

Exchange Funds for Concentrated Stock

Exchange funds for concentrated stock can be appropriate for a narrow group of investors who want diversification without an immediate taxable sale. In broad terms, the investor contributes appreciated shares to a pooled vehicle and receives an interest in a diversified basket instead of simply selling the stock outright.

This can sound elegant, but the tradeoffs are real. Eligibility can be limited. Liquidity is reduced. Fees are meaningful. Holding periods are long. For the right household, an exchange fund can be useful. For many others, a staged selling plan is simpler, more flexible, and easier to explain.

Charitable Giving Strategies

For households with charitable intent, appreciated stock can be one of the cleanest assets to give away. Donating low-basis shares can reduce concentration, support a tax deduction, and avoid realizing embedded gains that would otherwise accompany a sale.

Donor-advised funds (DAFs) are often helpful when the investor wants the deduction in one year but would prefer to choose grants over time.

Lending and Liquidity Solutions

Borrowing against a concentrated position can provide liquidity without an immediate sale, but it should be treated as a liquidity tool rather than a diversification tool. In a falling market, leverage can make the household more fragile, not less.

That distinction matters. Lending can be sensible for short-term cash flow needs, but it is rarely a substitute for reducing concentration itself.

How to Diversify a Concentrated Stock Position: Creating Your Plan

Step 1: Assessment Phase

Start with the whole balance sheet. Review taxable accounts, retirement accounts, private assets, cash needs, and any expected grants or liquidity events. Then evaluate the position against goals, risk tolerance, and concentration by lot.

This is where single stock concentration risk becomes concrete. A household may say it has high risk tolerance, but the real test is whether it can tolerate a large decline without changing retirement timing, spending plans, charitable goals, or family transfers.

Step 2: Implementation Strategy

The best implementation strategy is usually specific, staged, and boring. Decide which lots are candidates for sale, which should be held longer, which may be gifted, and what percentage of the position should come down over the next period of time.

When clients ask how to diversify a concentrated stock position, the answer is usually not one transaction. It is a sequence of decisions made in the right order with a financial advisor, tax professional, and, when needed, legal counsel.

Step 3: Ongoing Monitoring

Review the plan at least quarterly and after any major life or company event. A new grant, a promotion, a liquidity event, or a major market move can all change the right answer.

The goal is to keep reducing concentration deliberately over a defined period of time rather than letting the position drift back up unnoticed.

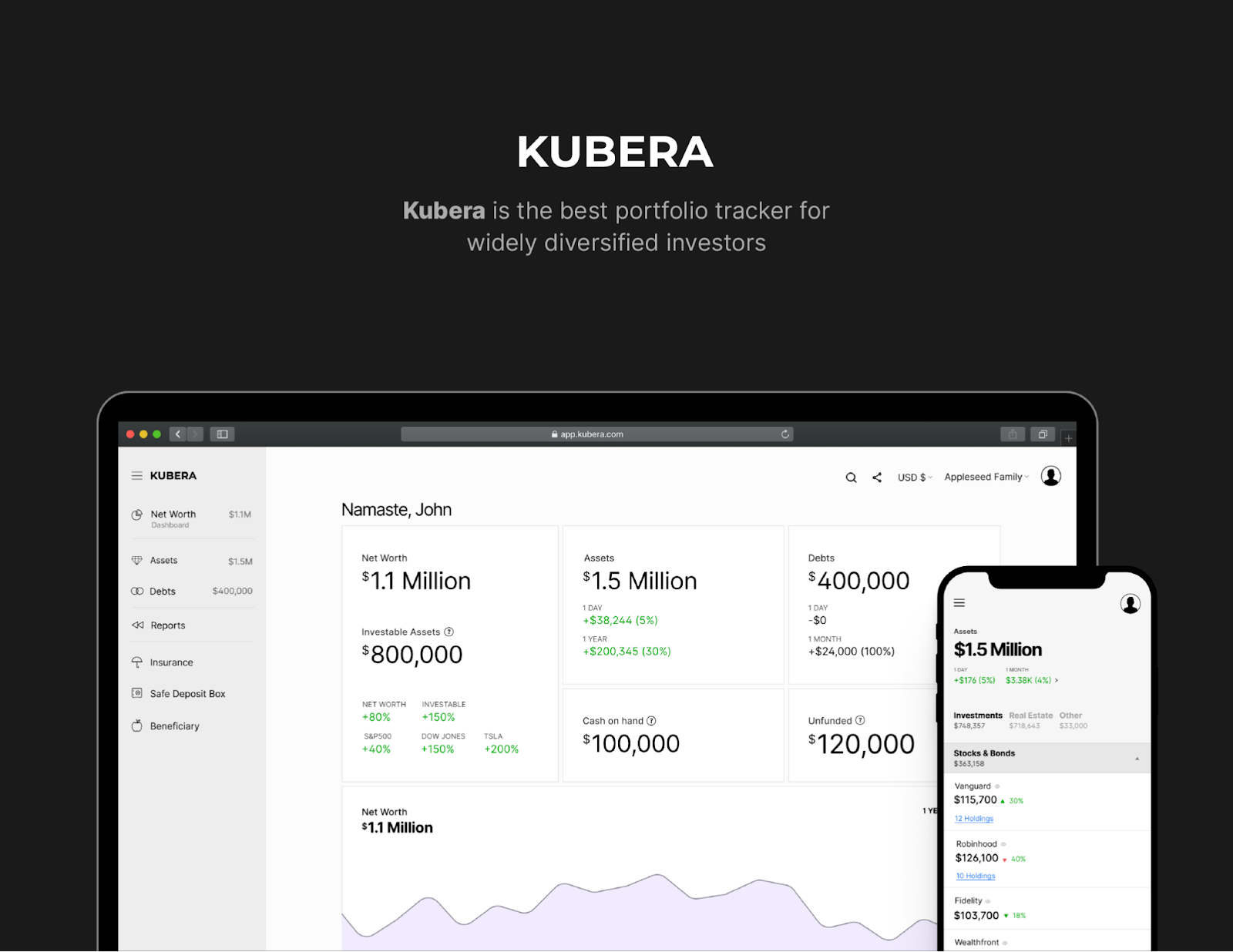

Managing Concentrated Stock with Modern Wealth Technology

Why Traditional Tools Fall Short

A spreadsheet can track shares, basis, and vesting dates, but it becomes fragile once the household has multiple entities, multiple grant years, outside accounts, and more than one advisor. What usually fails is not arithmetic. It is completeness and timeliness.

How Kubera Can Help

Kubera is not a substitute for advice, but it can be useful as an operating system for visibility. It provides high-net-worth individuals with a unified platform to track concentrated stock positions alongside their complete investment portfolio. By moving beyond manual data entry, Kubera offers the infrastructure needed to manage complex equity:

- Automated Equity Tracking: Direct integrations with equity platforms like Carta and Shareworks allow you to automatically sync vested balances, track unvested shares, and monitor upcoming liquidity events in real time.

- Centralized Dashboard: Monitor every component of your wealth in one place - from traditional brokerage and bank accounts to private equity, real estate, and crypto. If the household uses it well, it can make it easier to see current net worth, connected accounts, concentrated holdings, and upcoming vesting events in one place.

- Secure Advisor Collaboration: Share specific portfolio views with your financial advisor, CPA, and estate attorney without exposing your login credentials. This ensures your entire advisory team is working from the exact same real-time data when executing a 10b5-1 plan or tax-loss harvesting strategy.

- Integrated Document Vault: Securely store grant agreements, exercise notices, K-1s, and tax forms directly alongside the relevant portfolio assets.

That visibility matters because good implementation depends on current data. A dashboard that shows position size, relationship to total wealth, and the next likely tax event is often enough to improve execution materially without turning the software into the hero of the story.

Join thousands of high net worth individuals and executives who trust Kubera to track their equity compensation and concentrated positions across every account. Start your trial today and see your complete financial picture in minutes.

Frequently Asked Questions

When does a position become too concentrated?

There is no single line that applies to everyone, but concern usually rises once one stock exceeds 10 percent of investable assets. The effective exposure may be much higher if employment, future grants, or family cash flow also depend on that same company.

Should I ever keep a large position?

Sometimes yes. A founder preserving control, an executive facing strict trading constraints, or a family with substantial outside assets may rationally keep a larger stake. The key is that the concentration should be intentional, priced, and monitored, not inherited by default.

Are exchange funds for concentrated stock worth it?

Sometimes, but only for a limited set of investors. They can help defer tax while improving diversification, but fees, liquidity limits, minimums, and eligibility rules are meaningful constraints.

What is the biggest mistake investors make?

They frame the decision as all or nothing. In practice, most good outcomes come from a series of measured steps that reduce risk, manage the tax bill, and respect the broader financial plan.

Take Control of Your Concentrated Stock Position Today

A concentrated stock position does not require panic, but it does require discipline. Investors usually get into trouble when they confuse familiarity with safety or tax friction with a reason to stay overexposed.

The right response is to evaluate the position in the context of your total wealth, your goals, your tax situation, and your tolerance for downside. Then act with a plan. That is how investors reduce concentrated stock risk without making reactive decisions.

Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or legal advice. Tax rates, eligibility rules, and product features change over time. Investors should consult their own financial advisor, tax professional, and legal counsel before acting.