Strategic stock option planning ranks among the most powerful wealth-building tools for executives and founders. A single exercise decision can create tax bills exceeding $100,000. The right approach to stock options tax planning turns that liability into a strategic advantage.

The Core Challenge: The federal government taxes stock option gains at rates ranging between 0% and 37%. Your option type, exercise timing, and holding period determine where you land on that spectrum. Sophisticated investors who integrate deferred compensation and equity grants as a coordinated tax strategy keep significantly more wealth.

This guide covers everything you need: ISO vs. NSO tax treatment, incentive stock options Alternative Minimum Tax (AMT) calculations, advanced estate planning, and the stabilized QSBS changes under the One Big Beautiful Bill Act signed July 4, 2025.

Understanding Stock Options and Tax Implications for Substantial Equity Positions

A stock option grants the right to purchase company shares at a fixed price. That fixed price goes by two names: the strike price or the exercise price.

Profit potential lies in the appreciation of company stock value above the strike price. You buy low at the strike price and sell the stock later at the higher market value.

For high-net-worth individuals, options often represent $500K or more in concentrated wealth. This level of exposure demands sophisticated planning across tax, estate, and portfolio dimensions.

The Two Critical Taxable Events

Every stock option creates two taxable events that shape your total tax bill.

- Event 1. At Exercise: You purchase shares at the strike price and the IRS recognizes income.

- Event 2. At Sale: You sell the shares and realize capital gains or losses.

When managing equity positions worth $500K or more, tax optimization at each event can save $100K+ annually. (Learn more about capital gains tax rates and strategies.)

Why Option Type Determines Your Tax Strategy

Two types of stock options exist: Non-Qualified Stock Options (NSOs) and Incentive Stock Options (ISOs). Each follows fundamentally different tax rules.

The distinction becomes critical for individuals in the top tax brackets. Federal ordinary income tax rates reach 37%, while long-term capital gains max out at 20% plus the 3.8% Net Investment Income Tax (NIIT). That 13.2% gap on a $1M option exercise equals $132,000 in potential savings.

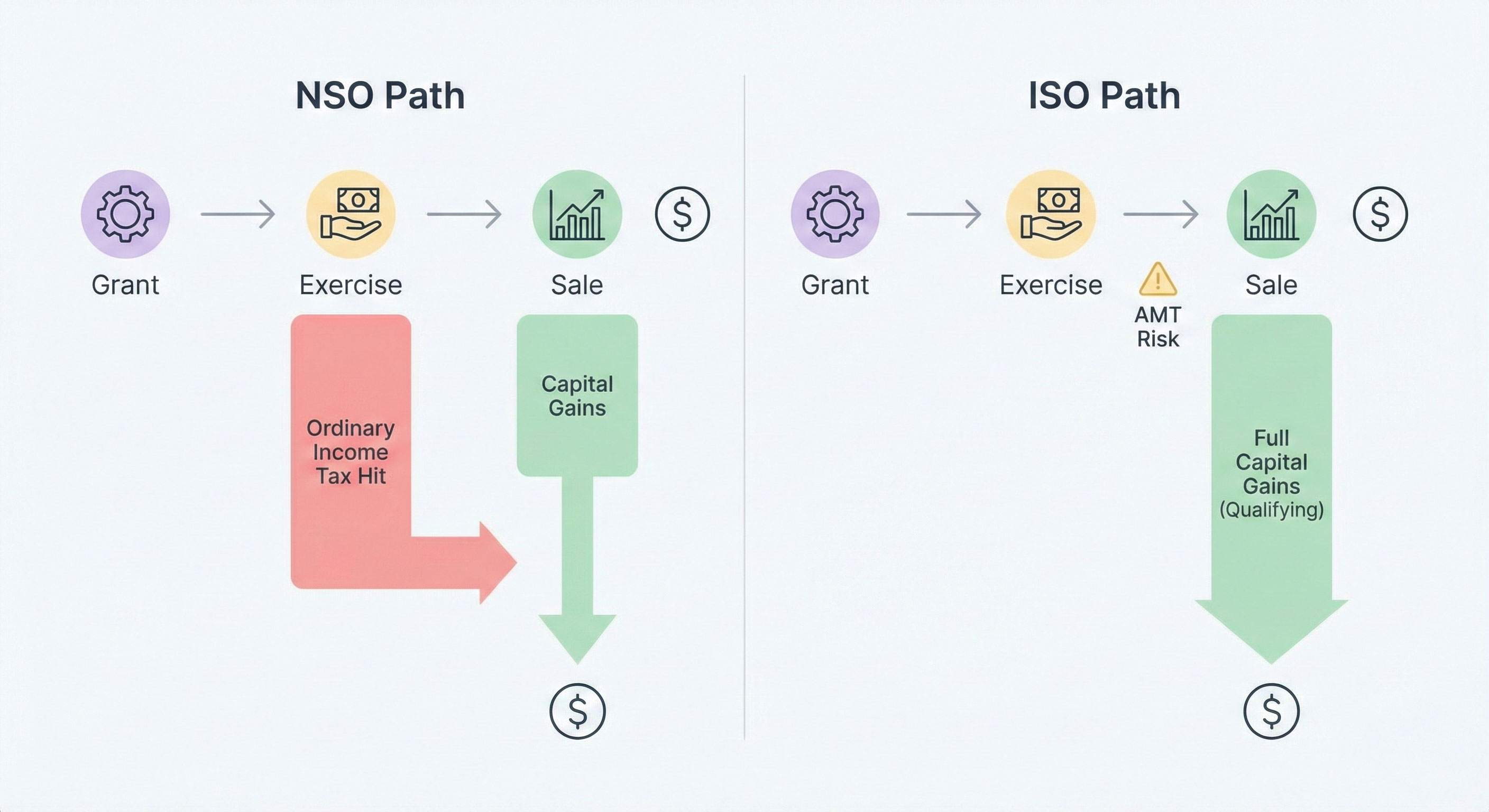

How Are Non-Qualified Stock Options (NSOs) Taxed?

NSOs represent the most common type of stock options for senior executives and board members. Companies can grant them to employees, contractors, consultants, and advisors.

They offer more flexibility than ISOs but carry less favorable tax treatment. Every dollar of gain at exercise faces ordinary income tax rates.

NSO Taxation at Exercise: The Ordinary Income Hit

When you exercise the options, the IRS taxes the spread between the fair market value (FMV) and your strike price as ordinary income. Your employer withholds federal, state, and payroll taxes and reports this income on your Form W-2.

NSO Exercise Tax Calculation Example:

Note: This calculation assumes the 2025 Social Security wage base of $176,100. High earners typically max out the Social Security portion early in the year, leaving only the 1.45% Medicare tax and 0.9% Additional Medicare Tax on the exercise income.

This example shows why cash planning matters before exercising. You owe $113,718 in taxes on income you received as shares, not cash.

NSO Taxation at Sale: Capital Gains Treatment

After exercising, your cost basis equals the FMV on the exercise date. Any future appreciation above that basis qualifies for capital gains treatment, not ordinary income rates.

Short-term gains (held one year or less after exercise) face ordinary income tax rates up to 37%. Long-term capital gains (held more than one year after exercise) enjoy preferential rates of 0%, 15%, or 20% federal, plus the 3.8% NIIT for high earners.

NSO Sale Tax Calculation: Sell at $40, Held 2+ Years After Exercise

Strategic NSO Planning for High-Net-Worth Portfolios

Smart executive stock option tax planning coordinates exercise timing with your broader financial picture.

- Time exercises to align with capital loss harvesting in your broader portfolio.

- Defer exercise until immediately before liquidity events to minimize the gap between exercise and sale.

- Split large exercises across multiple calendar years to manage marginal tax bracket impact.

- Use cash to pay exercise costs and withholding rather than selling shares to preserve upside.

On a $200,000 exercise requiring $113,000 in taxes, cash payment preserves 4,400 shares worth $110,000 today. Those shares could multiply at exit. (See also: Should I sell my RSUs when they vest?)

How Are Incentive Stock Options (ISOs) Taxed?

ISOs offer the most favorable tax treatment for stock options. Only employees qualify. Contractors and advisors cannot receive ISOs.

The key benefit: all gains can potentially face long-term capital gains tax rates instead of ordinary income rates. For executives in the top bracket, this means paying 23.8% instead of 40.8% (37% Income + 3.8% NIIT) on the same gain.

How Does the Alternative Minimum Tax (AMT) Work with ISOs?

Here is what you need to know: the IRS does not tax ISO exercises as ordinary income. However, the bargain element becomes an adjustment for Alternative Minimum Tax (AMT) purposes.

The AMT operates as a parallel tax system. You calculate your tax liability under both the regular system and the AMT system, then pay whichever amount is higher. For 2025, AMT rates stand at 26% on the first $239,100 of AMT income and 28% above that threshold. The AMT exemption for single filers equals $88,100 in 2025.

The AMT Trap: Paying Tax Without Cash

Exercising ISOs and holding shares past December 31 can trigger a substantial AMT bill even though you received no cash. This creates a liquidity crisis that many executives fail to anticipate.

Important exception: if you sell the shares in the same calendar year as the exercise, the AMT adjustment does not apply and the gain is taxed as ordinary income.

ISO AMT Calculation Example:

This $113,000 tax bill arrives without any cash from a sale. Plan your liquidity carefully before exercising ISOs you intend to hold.

AMT Credit Carry-Forward

AMT paid creates a credit you can use in future years when your regular tax exceeds AMT. You can recover these credits when you sell ISO shares or in years with lower AMT exposure.

For high-net-worth individuals, tracking these credits across years forms a critical part of long-term tax planning. (See: Tracking net worth)

Qualifying vs. Disqualifying Dispositions: What Happens When You Sell?

A qualifying disposition delivers the maximum tax benefit for ISOs. You must hold shares for at least 2 years after the grant date AND at least 1 year after the exercise date.

Meet both requirements, and the entire gain from strike price to sale price faces long-term capital gains tax rates. No ordinary income portion applies.

Qualifying Disposition Example:

- Strike Price: $5 per share

- FMV at Exercise: $55 per share (AMT paid on $50 spread)

- Sale Price: $75 per share (meets both holding periods)

- Total Long-Term Capital Gain: $70 per share ($75 - $5)

- For 10,000 shares: $700,000 LTCG

- Federal LTCG Tax at 23.8%: $166,600

- State Tax (CA 14.4%): $100,800

- Total Tax on Sale: $267,400

When Does a Disqualifying Disposition Make Sense?

A disqualifying disposition occurs when you fail to meet either holding period. The IRS splits the tax treatment: the bargain element at exercise becomes ordinary income, and additional gain above FMV faces capital gains rates.

Intentional disqualification sometimes saves money. If the AMT burden from holding exceeds the ordinary income tax from selling early, an immediate sale produces a better outcome.

ISO vs. NSO Tax Treatment: Side-by-Side Comparison

The $100,000 ISO Annual Limit

Only the first $100,000 worth of ISOs (valued at strike price) becoming exercisable per calendar year receive ISO treatment. Amounts exceeding this limit automatically convert to NSO tax treatment.

Example: 50,000 ISOs vest with a $5 strike price, totaling $250,000 in value. The first 20,000 shares ($100,000) receive ISO treatment. The remaining 30,000 shares ($150,000) face NSO ordinary income rules at exercise.

What Advanced Tax Strategies Work for High-Net-Worth Individuals?

Qualified Small Business Stock (QSBS) Exclusion Under Section 1202

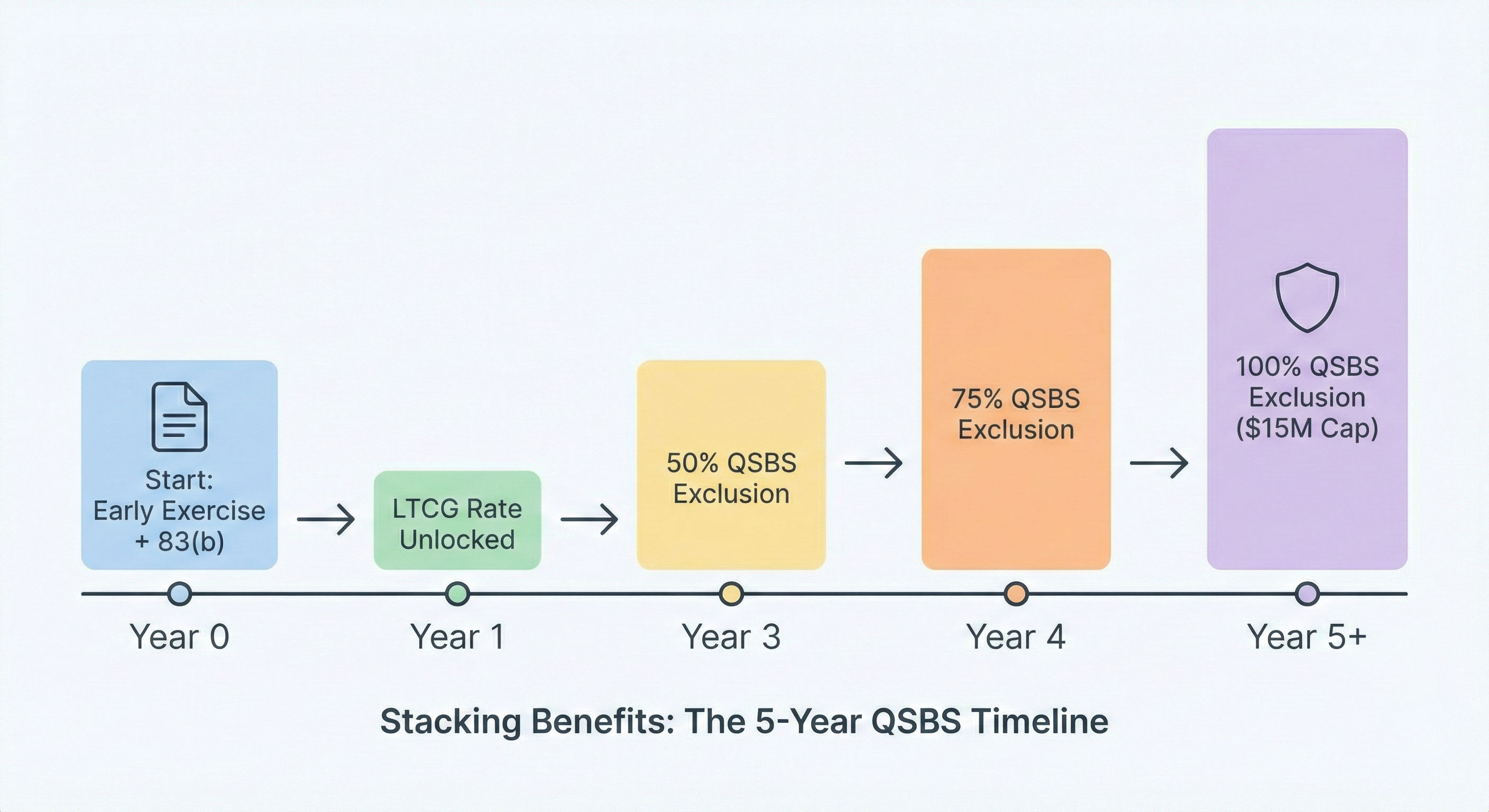

The QSBS exclusion represents one of the most powerful tax benefits available to founders and early employees. Section 1202 allows exclusion of up to $15 million (for stock issued after July 4, 2025) or 10x cost basis in capital gains, whichever is greater.

The One Big Beautiful Bill Act, signed July 4, 2025, expanded these benefits significantly. The gross asset threshold increased from $50 million to $75 million. A new tiered holding period now offers 50% exclusion at 3 years, 75% at 4 years, and 100% at 5 years for newly issued stock.

Strategic approach: Exercise options early when the company qualifies to start the holding period clock. Only domestic C corporations with gross assets under $75 million at issuance qualify.

Early Exercise Programs and the 83(b) Election

Some private companies allow option exercise before vesting. This technique offers three major advantages for stock options tax planning.

- Exercise when the spread is low. Exercise when the spread between strike and FMV is minimal or zero, reducing ordinary income (NSOs) or AMT (ISOs).

- Start the LTCG clock. Start the holding period clock for long-term capital gains immediately.

- Start the QSBS clock. Begin the QSBS 5-year holding period earlier.

Critical requirement: You must file an 83(b) election with the IRS within 30 days of early exercise. Missing this deadline eliminates the tax benefit entirely. The risk: Your invested capital is lost if shares do not vest and the company repurchases them at cost.

Concentration Risk: The 10/5 Rule for Portfolio Diversification

Consider diversifying when a single stock position exceeds 10% of total net worth or 5x your annual living expenses.

For an individual with $10M net worth holding $3M in company stock (30% concentration), the risk warrants action. Tax-efficient diversification strategies include exercising and selling just enough annually to stay in your desired tax bracket, harvesting capital losses from other holdings to offset option gains, and using hedging tools like protective puts or cashless collars.

Estate Planning and Wealth Transfer Strategies

The 2025 federal estate tax exemption stands at $13.99 million per individual, now made permanent by the OBBBA. Strategic use of stock options within estate planning multiplies wealth transfer efficiency.

- Gifting Options: Gift vested NSOs to family members using the annual gift tax exclusion ($19,000 per recipient in 2025) or lifetime exemption. Note: Most plans prohibit gifting ISOs.

- GRATs: Transfer exercised shares to a Grantor Retained Annuity Trust (GRAT). Appreciation above the IRS Section 7520 hurdle rate passes to beneficiaries gift-tax-free.

- Charitable Remainder Trusts: Donate highly appreciated stock. You avoid capital gains tax and receive an immediate charitable income tax deduction. (See: Charitable remainder trust guide)

Example: $5M in ISO shares with $100K cost basis donated to a CRT avoids approximately $1.17M in capital gains tax while providing a lifetime income stream.

Cross-Border Tax Considerations

U.S. tax residents pay tax on worldwide income, including foreign company stock options. Tax treaties may provide credits for foreign taxes paid, but timing of income recognition can differ between countries.

Expatriation triggers an "exit tax" that marks all property (including unexercised options) to market. Plan to exercise options before any change in tax residency to lock in basis and minimize phantom gains.

Which Tax Forms Do You Need for Stock Options?

Proper documentation prevents costly errors. Stock options generate specific tax forms at each stage.

Pro tip: Broker-reported cost basis on Form 1099-B is often incomplete for option exercises because brokers may not track the ordinary income portion added to your basis. Maintain your own records of exercise dates, FMV, and share counts.

Why Does Holistic Wealth Management Matter for Stock Options?

Stock options taxation ranks among the most complex areas of the tax code for high-net-worth individuals. A single misstep creates six-figure consequences.

The challenge grows when you consider how many moving parts demand simultaneous tracking:

- Vesting schedules across multiple grant dates

- Two separate holding period clocks for ISOs (grant date and exercise date)

- Cost basis records for each exercise event at different FMV amounts

- AMT credit carry-forwards across tax years

- Portfolio concentration as a percentage of total net worth

- Tax forms (3921, W-2, 6251, 8949) across multiple years

Stock options do not exist in isolation. They represent one component of a wealth portfolio that typically includes public equities, real estate, alternative investments, retirement accounts, business interests, and cash. Optimizing stock options tax strategy requires seeing the full picture.

How Kubera Simplifies Stock Options Management

Kubera provides high-net-worth individuals with a unified platform to track stock options alongside their complete investment portfolio.

- Automated Options Tracking: Direct integration with platforms like Carta, Shareworks, and others allows you to automatically sync vested balances, grant details, and latest valuations without manual entry.

- Pre-IPO Valuation Updates: Manually update custom 409A valuations to reflect the real-time fair market value of your private equity, ensuring your net worth figure isn't stuck in the past.

- Cost Basis Management: Track cost basis, exercise dates, FMV, and share counts for each option grant.

- Holding Period Monitoring: Monitor time from grant and exercise dates to optimize for qualifying ISO dispositions.

- Concentration Analysis: View equity compensation as a percentage of total net worth with real-time alerts.

- Holistic Visibility: Connect all asset classes in a single dashboard: equities, real estate, alternatives, crypto, and more.

- Collaboration: Share portfolio views with CPAs, wealth advisors, and estate attorneys without exposing credentials.

- Built for privacy and security: Kubera uses AES-256 encryption, read-only account connections, and multi-factor authentication. Your data never gets sold to third parties or used for advertising. Kubera is also SOC 2 Type 2 compliant, adhering to rigorous institutional-grade security standards unlike other consumer apps for additional peace of mind.

Start Managing Your Stock Options with Clarity

Take control of your equity compensation and complete wealth portfolio today. Try Kubera free for 14 days (no credit card required).

Frequently Asked Questions: Stock Options Tax Strategies

What is the difference between ISO and NSO tax treatment?

ISOs receive no regular income tax at exercise. Instead, the bargain element triggers AMT. If you meet both holding period requirements, the entire gain qualifies for long-term capital gains rates. NSOs generate ordinary income at exercise, taxed as ordinary income on the spread between FMV and strike price.

How does the incentive stock options AMT work?

When you exercise ISOs and hold the shares past December 31, the bargain element becomes an AMT adjustment. The IRS calculates your tax under both regular and AMT systems. You pay whichever is higher. For 2025, AMT rates are 26% and 28%, with an exemption of $88,100 for single filers.

Can I avoid AMT on ISO exercises?

Yes. Sell the shares in the same calendar year as the exercise. This same-year sale eliminates the AMT adjustment entirely and treats the gain as ordinary income. You can also exercise smaller batches across multiple tax years to keep the AMT preference below your exemption threshold.

What is the $100,000 ISO limit?

Only ISOs with a total strike price value of $100,000 or less can become exercisable in any single calendar year.Amounts above this limit automatically receive NSO tax treatment. Plan vesting schedules and exercise timing across years to maximize ISO benefits.

How did the One Big Beautiful Bill Act change QSBS rules?

The OBBBA, signed July 4, 2025, increased the QSBS exclusion cap from $10 million to $15 million for stock issued after that date. It raised the gross asset threshold from $50 million to $75 million. It also introduced tiered holding periods: 50% exclusion at 3 years, 75% at 4 years, and 100% at 5 years.

Should I exercise my stock options before an IPO?

Exercising before an IPO can start your holding period clock for long-term capital gains treatment. It may also qualify shares for QSBS exclusion if the company meets Section 1202 requirements. However, you risk capital if the IPO fails or the stock price drops. Coordinate timing with your tax advisor and overall financial plan.

How do I calculate the tax on my stock option exercise?

Multiply the number of shares by the spread (FMV minus strike price). For NSOs, this amount faces ordinary income tax rates plus payroll taxes. For ISOs, calculate the AMT adjustment by adding the spread to your AMT income and comparing the result against your regular tax. Use Form 6251 or consult a tax professional for the exact calculation.