-Election.jpg)

Understanding the 83(b) election represents one of the most important financial decisions for anyone receiving equity compensation. This guide covers everything about the 83(b) election startup employees need to know.

We explain the 83(b) election tax benefits, walk through the new electronic filing instructions, and show you how to combine the QSBS 83(b) election strategy for maximum wealth building.

Understanding the 83b Election for Equity Compensation

The 83(b) election is a formal notification to the IRS under Section 83(b) of the Internal Revenue Code. This election allows startup employees and founders to pay income tax on equity at the time of granting rather than at the time of vesting.

The election applies only to restricted stock and early-exercised options with vesting schedules. Standard stock options that you have not exercised early do not qualify for this election.

Filing an 83(b) election represents a strategic decision to accelerate your tax liability. In exchange, you receive preferential long-term capital gains treatment on all future appreciation of your shares.

Why does this matter for startup employees? High-growth startups can see stock values increase dramatically during your vesting period. Without filing the 83(b) election, you pay ordinary income taxes on that entire appreciation as your shares vest.

Consider this scenario common among startup employees receiving restricted stock: You join a company when shares cost $0.01 each. Four years later at the time of vesting, those shares trade at $10 each. The tax difference can reach hundreds of thousands of dollars.

83b Election Tax Benefits: Converting Ordinary Income to Capital Gains

The 83(b) election tax benefits transform how the IRS taxes your equity compensation. Future stock appreciation shifts from ordinary income tax rates (up to 37%) to the long-term capital gains rate (capped at 20%).

This difference of 17 percentage points means you keep more money. The savings grow larger as your company's value increases over time.

Taxation With the 83b Election

When you file the 83(b) election, you pay taxes immediately on the stock's fair market value at the time of granting. For early-stage startups, this value often approaches zero or costs just pennies per share.

As your unvested shares vest over time, you owe no additional taxes. This means no "phantom income" creates tax liability before you receive any actual cash.

When you eventually sell your fully vested shares at an exit, you pay the preferential capital gains rate. If you hold the shares for more than one year, you qualify for long-term capital gains treatment at rates of 0%, 15%, or 20%.

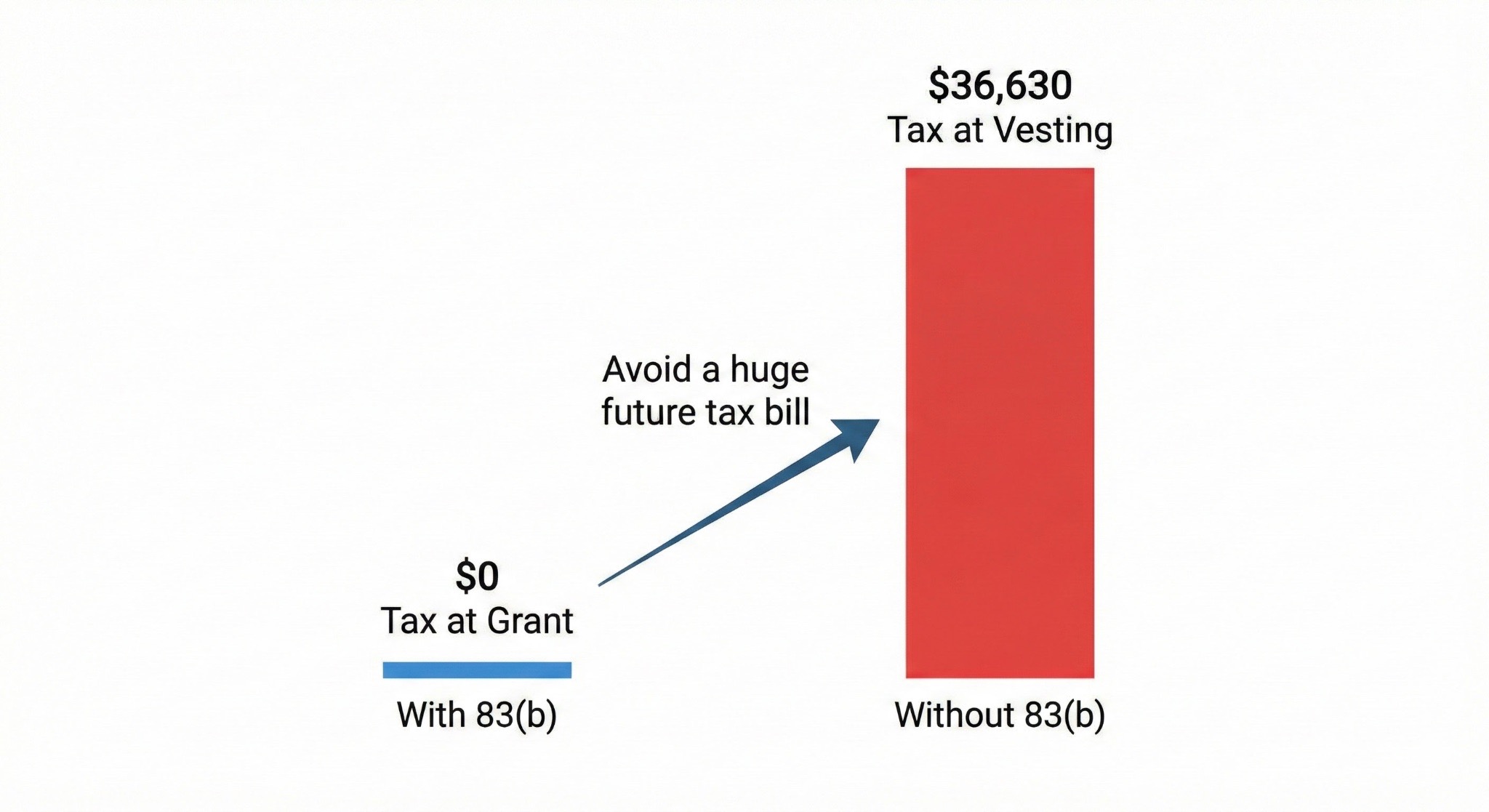

Taxation Without the 83b Election

Without the 83(b) election, you pay no tax at the time of your stock granting. This seems attractive until you understand the consequences.

Each time shares vest, you owe ordinary income tax on the difference between the grant price and the current fair market value. This creates taxable income even though you received no cash to pay those taxes.

This situation creates the "phantom income" problem that traps many startup employees. You may owe tens of thousands in taxes on paper gains while unable to sell your shares to cover the bill.

Additionally, the Alternative Minimum Tax (AMT) can trigger significant tax liability on unvested shares for employees who exercise incentive stock options (ISOs) early.

Real-World 83b Election Tax Savings Example

Let's examine a realistic scenario for a startup employee receiving restricted stock. The numbers demonstrate exactly how much money the 83b election can save.

Scenario: You receive 100,000 shares at $0.01 per share. At the time of vesting four years later, shares trade at $1.00 each. You sell at $5.00 per share after the company's exit.

Total savings with the 83b election: $16,830

This example uses the maximum federal tax rate of 37% for ordinary income and 20% for long-term capital gains. Your actual savings depend on your specific tax bracket and state taxes.

QSBS & 83(b) Election: The Ultimate Tax Advantage

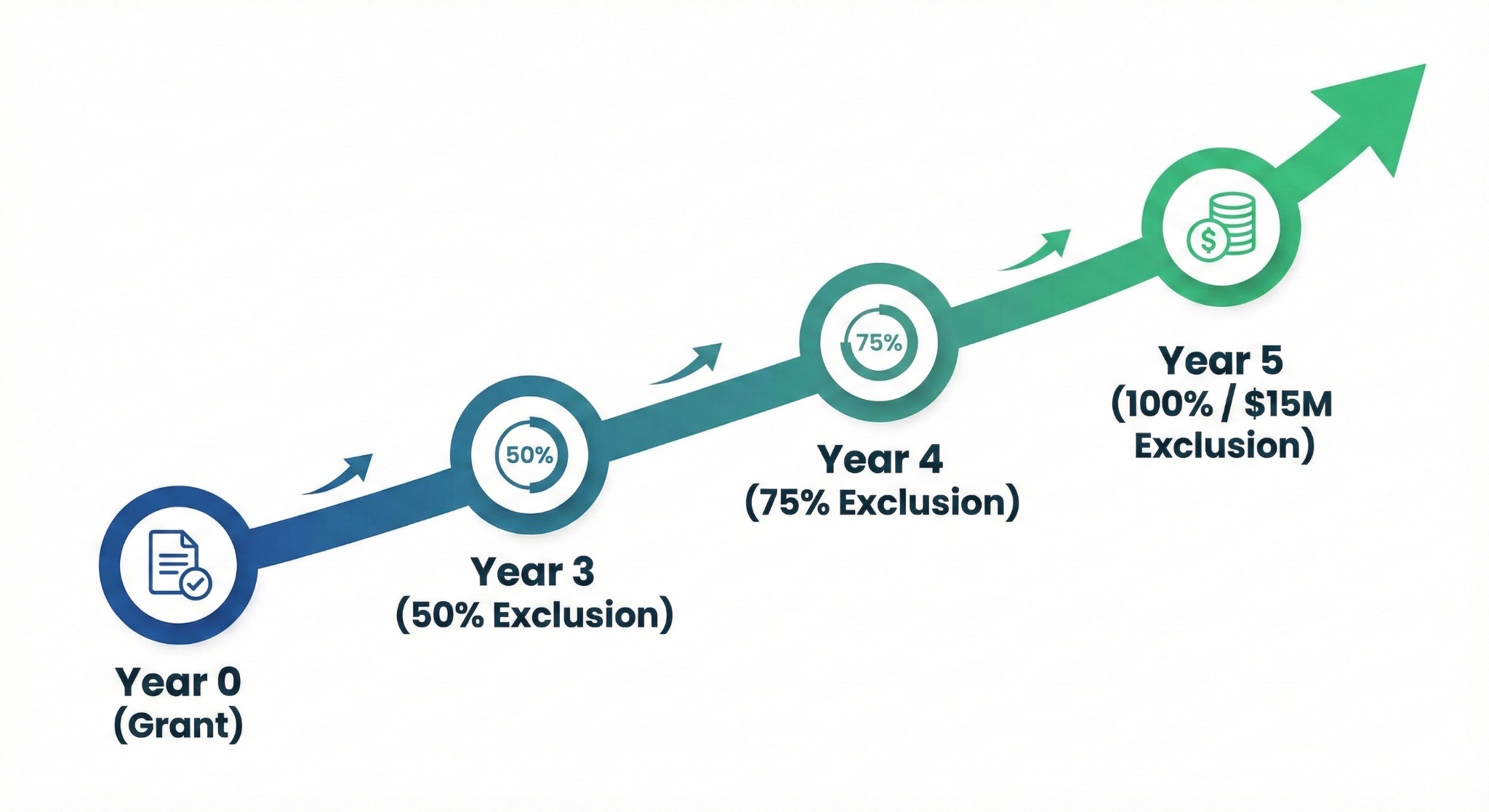

The QSBS 83b election combination immediately starts the holding period for Qualified Small Business Stock (Section 1202). This strategy creates extraordinary tax savings for startup equity.

QSBS rules allow you to exclude millions in capital gains from federal taxes. Under the One Big Beautiful Bill Act signed in July 2025, this exclusion increased to $15 million (inflation-adjusted starting in 2027) for stock issued after July 4, 2025.

Crucially, the new law also introduced tiered benefits for shorter holding periods:

Filing the 83(b) election proves critical for maximizing QSBS benefits. Your holding period begins at the time of granting when you file the election. Without filing, your holding period starts only when shares become fully vested.

High-net-worth individuals understand that preserving wealth requires minimizing tax drag on appreciation wherever legally possible. The QSBS 83(b) election combination represents one of the most powerful wealth-building tools available to startup employees.

Who Should File the 83b Election?

Startup Founders and Early Employees

Tax advisors almost universally recommend the 83(b) election for startup employees joining pre-Series A companies. The stock value at this stage typically remains extremely low, resulting in minimal tax at grant.

Early employees receive shares worth fractions of a penny. Filing the election costs almost nothing in immediate taxes.

Tech Professionals at High-Growth Companies

Employees receiving restricted stock awards (RSAs) benefit significantly from filing. Anyone early-exercising stock options at companies with substantial growth potential should strongly consider this election.

Recipients of Specific Equity Types

The 83b election applies to:

- Restricted Stock Awards (RSAs)

- Early-Exercised Incentive Stock Options (ISOs)

- Early-Exercised Non-Qualified Stock Options (NSOs)

- Profits Interests in LLCs

Understand the value of unvested stock options before making your decision.

When the 83b Election Does Not Apply

The election does not apply to:

- Fully vested stock with no restrictions

- Standard stock options you have not early-exercised

- Restricted Stock Units (RSUs) from public companies

RSUs work differently than restricted stock. You never own actual shares until they vest.

If startup equity represents less than 10-15% of your total net worth, the forfeiture risk becomes easier to absorb. You can take more aggressive positions when unvested equity does not dominate your financial picture.

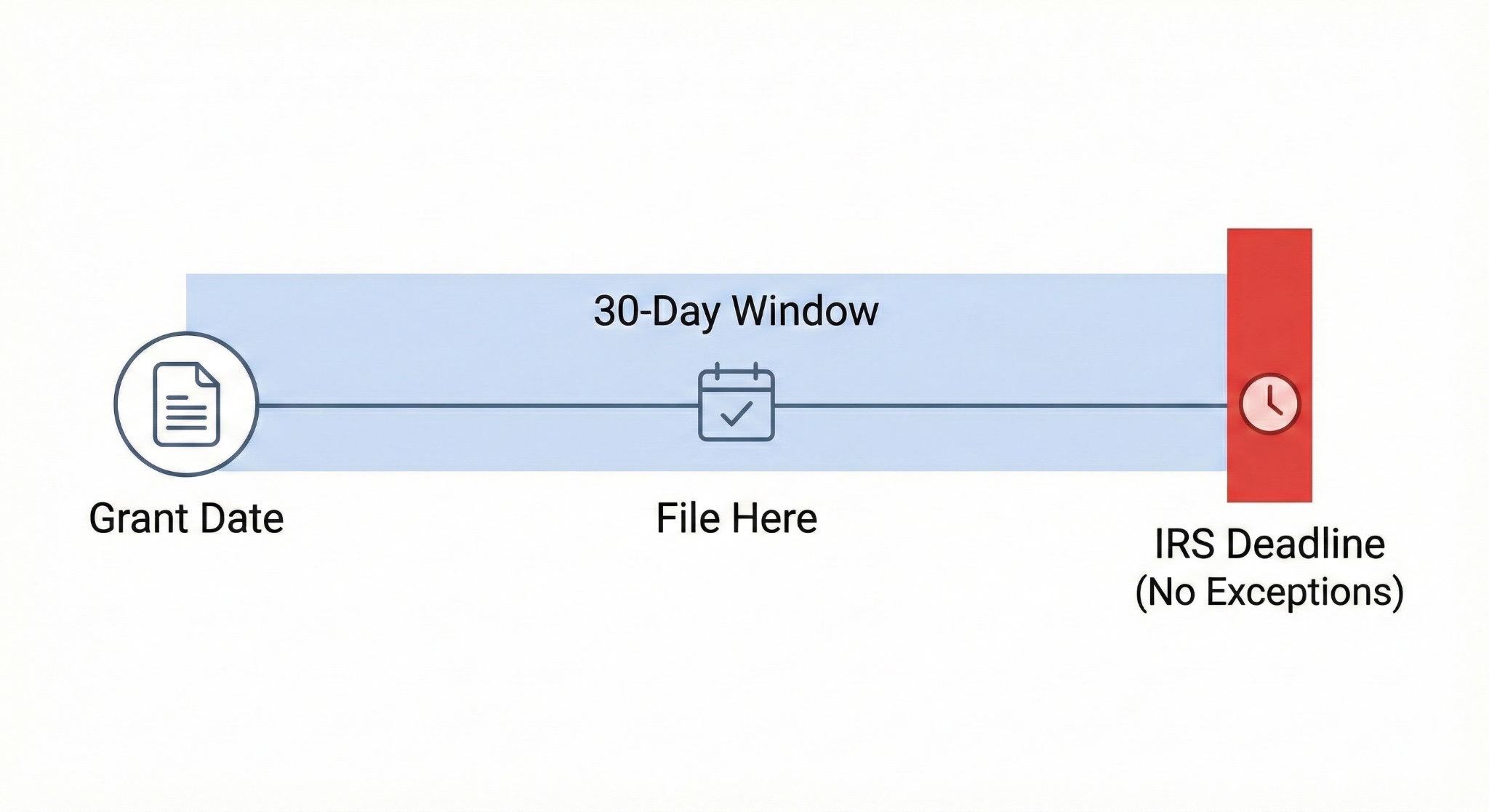

The 83(b) Election Deadline: Non-Negotiable 30-Day Window

The 83(b) election deadline requires you to file within 30 calendar days of your equity grant date. The IRS provides zero exceptions and grants no extensions for this deadline.

Your grant date typically represents the board approval date. This date often precedes when you receive official paperwork from HR by days or weeks.

If the 30th day falls on a weekend or federal holiday, your deadline extends to the next business day. Beyond this narrow exception, the deadline remains absolute.

The most common pitfall involves waiting for your company's HR department to notify you. Proactive employees track their grant dates independently and file the election themselves.

83b Election Filing Instructions: Step-by-Step Process

Understanding the 83(b) election filing instructions helps you avoid costly mistakes. In late 2024, the IRS introduced Form 15620 specifically for 83(b) elections to standardize the process. As of July 2025, the IRS also accepts electronic filing through their website.

Step 1: Prepare the Election Form

You can now use IRS Form 15620 or a standard written statement. Complete all required fields including your name, address, Social Security number, and detailed stock information.

You must include the fair market value at grant, the amount you paid, and a description of the property transferred. Keep a copy of the election for your records.

Step 2: Create Multiple Copies

If filing by mail, print at least three copies of your completed election. You need one for the IRS, one for your employer, and one for your personal records.

Step 3: Submit to the IRS

- Electronic Filing (Preferred): You can file electronically through the IRS portal using ID.me verification. This provides immediate confirmation of receipt.

- Mail Filing: If you prefer paper, send your election via certified mail with a return receipt requested to the IRS Service Center where you file your annual tax return.

Step 4: Distribute Copies

Provide one copy to your employer's HR or payroll department. They need this documentation for their tax records and to withhold applicable taxes.

Step 5: Document Everything

Store a copy of your election with your important financial documents. Record the grant details, fair market value, tax paid, and filing date for future reference.

Risk Assessment: When Filing May Not Make Sense

Forfeiture Risk Analysis

Data from Carta shows that within 37 months, most startup employees have left their company. The median tenure for startup employees stands at just over 2 years according to Ravio's 2026 compensation trends report.

Standard four-year vesting schedules mean many employees never fully vest their shares. Evaluate honestly how long you intend to stay before filing.

Company Viability Assessment

The IRS provides no refunds if your company fails or its value declines. You cannot recover taxes paid on stock that becomes worthless. This risk deserves careful consideration in your overall wealth protection strategy.

Immediate Tax Cost

Employees at later-stage companies face potentially significant upfront tax bills. If your stock has substantial fair market value at grant, the immediate tax cost may outweigh future benefits.

Alternative Considerations

Some employees at later-stage companies prefer deferring tax until liquidity events occur. This approach makes sense when you expect company value to decline or remain flat.

Consider how this equity fits into your broader portfolio diversification strategy. Making decisions in isolation from your overall wealth picture leads to suboptimal outcomes.

Tracking Your Equity Compensation as Part of Your Total Net Worth

Grant dates, vesting schedules, exercise windows, AMT implications, and holding periods all impact your wealth trajectory. Each variable requires careful tracking and timely action.

Equity compensation involves too many moving parts and date-sensitive decisions to track manually with spreadsheets. Missing a single deadline can cost you thousands of dollars in tax liability.

Understanding how unvested equity, exercised options, and stock holdings fit alongside liquid investments matters enormously. Your startup equity exists within the context of bank accounts, crypto assets, and traditional retirement accounts.

Storing 83(b) election forms, grant agreements, exercise records, and tax documents in a centralized system prevents costly mistakes. Learn about essential estate planning documents every equity holder needs.

Planning for how equity value changes affect your overall net worth and portfolio allocation requires visibility. Work with a qualified financial advisor who understands startup equity.

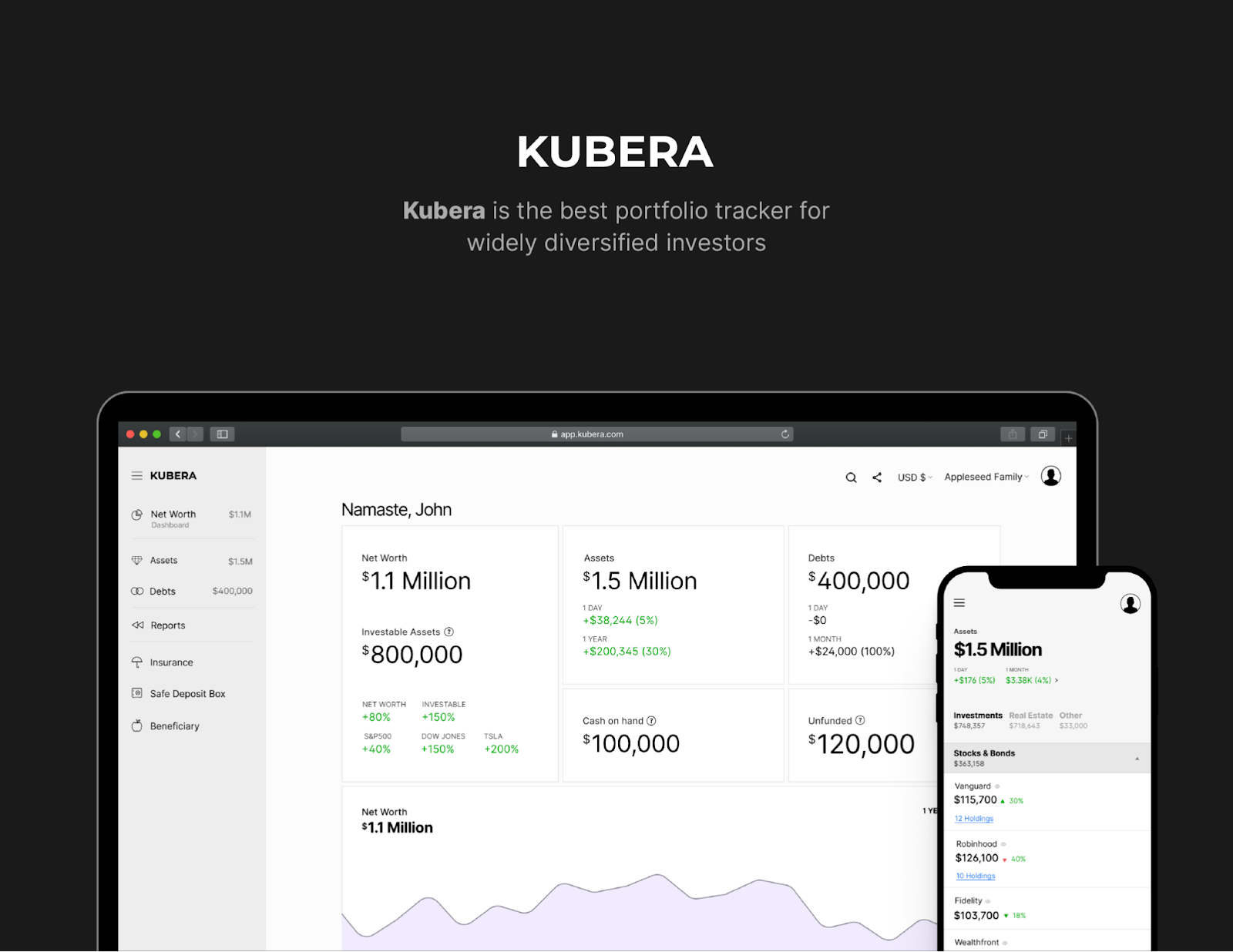

Using Kubera to Manage Equity Compensation and Total Wealth

Track all your assets in one place. Monitor startup equity alongside traditional investments, bank accounts, crypto holdings, and real estate.

Keep 83(b) election forms, grant agreements, and equity-related tax documents accessible in your centralized wealth dashboard. Never scramble to find critical paperwork again.

See how your equity value and total portfolio changes over time as your company grows. Real-time visibility enables better decision-making at every stage.

Kubera serves startup employees and high-net-worth individuals specifically. The platform handles complex, cross-border, and multi-asset-class portfolios that simple tools cannot manage.

Ready to organize your equity compensation and complete financial picture? Sign up for Kubera today.

Frequently Asked Questions About the 83b Election

What happens if I miss the 83(b) election deadline?

Here's what you need to know: You cannot file the election late. The IRS provides no extensions and accepts no late filings. You will pay ordinary income tax on your stock's appreciation as it vests rather than at grant.

Can I revoke an 83(b) election after filing?

No, the election is irrevocable. The IRS only permits revocation in extremely rare cases involving a mistake of fact about the underlying transaction. Disagreement about valuation does not qualify.

Do I need to use the new IRS Form 15620 for my 83(b) election?

While not strictly mandatory (you can still use a compliant written statement), Form 15620 is highly recommended as it standardizes the information required. Using the electronic filing version of this form via the IRS website is the fastest way to ensure timely receipt.

Does the 83(b) election guarantee I will save money on taxes?

No guarantee exists. If you leave before vesting or your company fails, you lose the taxes paid upfront with no refund. The 83(b) election tax benefits only help those who stay through vesting at companies that increase in value.

Can I file an 83(b) election for RSUs?

No, RSUs do not qualify. Restricted Stock Units represent a promise to deliver shares in the future rather than actual ownership. The 83(b) election applies only when you receive actual property subject to vesting.

How does the QSBS 83(b) election strategy work together?

Filing the 83(b) election starts your QSBS holding period at grant rather than vesting. This allows you to reach the required holding period years earlier. Combined with the potential $15 million gain exclusion, this creates substantial tax savings.

What is the grant date for the 83(b) election deadline?

The grant date typically represents when the company's board approves your equity award. This date often precedes when HR provides your official documentation. Ask your company directly if you remain uncertain about when to file the 83(b) election.