Section 1202 of the Internal Revenue Code is one of the most powerful provisions available to founders, startup employees, and early investors who hold equity in private companies. When the requirements are met, it can allow a non-corporate taxpayer to exclude a substantial portion of their federal capital gains on qualified small business stock (QSBS) — up to 100 percent for stock acquired after September 27, 2010 and held for more than five years, subject to per-issuer caps. For stock issued after July 4, 2025, the One Big Beautiful Bill Act (OBBBA) expanded the benefit further.

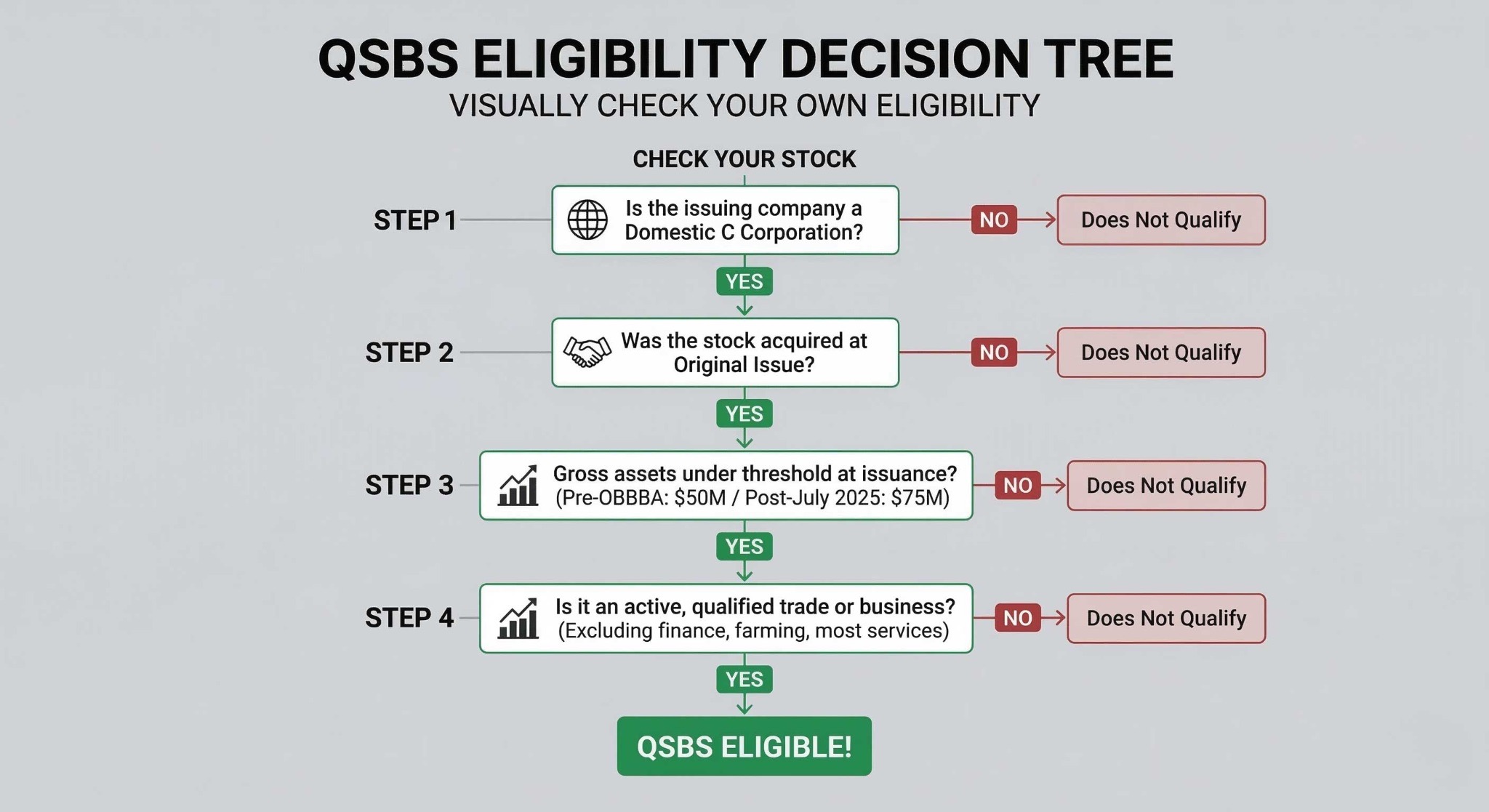

However, the Section 1202 exclusion is not automatic. The stock must be in a qualifying domestic C corporation. It must have been acquired at its original issue. The company must have passed the aggregate gross assets test at the time of issuance. The taxpayer must hold through the required period. Almost every scenario carries nuances that can quietly invalidate an otherwise clean setup. The QSBS tax exclusion rewards careful planning, not passive ownership. For founders and early employees, the most common mistake is not completely overlooking the rule, but rather waiting too long to determine their eligibility.

How Section 1202 Works

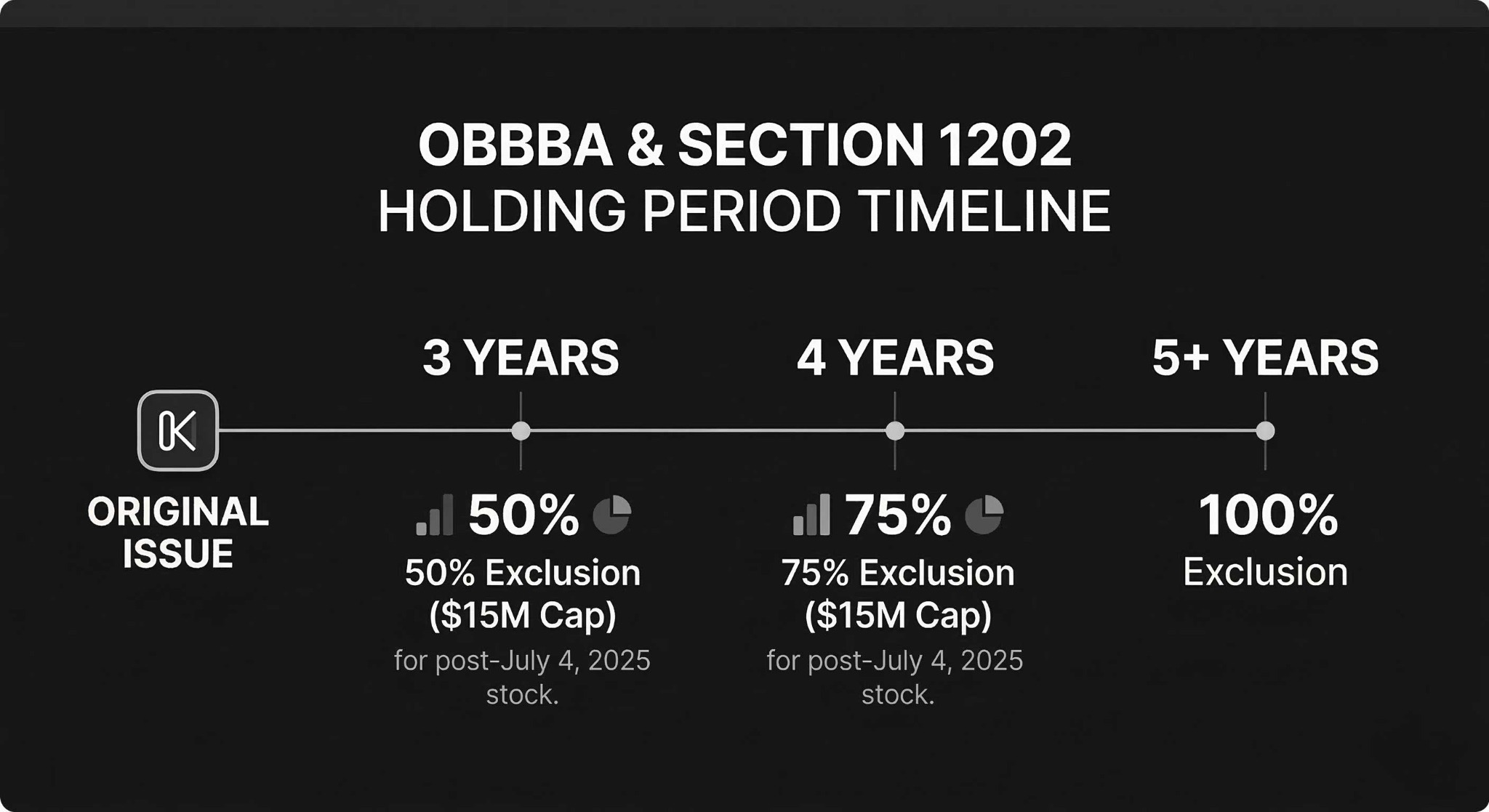

The exclusion percentage depends on when the stock was acquired. For stock acquired after September 27, 2010 and before July 4, 2025, the full 100 percent exclusion has been available after a five-year holding period. For earlier issuances, the exclusion is 50 percent (pre-2009) or 75 percent (2009-2010).

The OBBBA introduced a tiered structure for stock acquired after July 4, 2025: 50 percent after three years, 75 percent after four, and 100 percent after five. Partial exclusions at shorter holding periods are now meaningful, changing the exit-timing conversation for founders and early investors.

The Dollar Caps and 10x Basis Alternative

The per-issuer exclusion cap is the greater of the dollar cap ($10 million or $15 million depending on issuance date, reduced by prior exclusions on the same issuer) or 10 times the taxpayer's adjusted basis in the stock sold. For a founder who paid a nominal price for founder shares, the dollar cap typically governs. For an investor who deployed several million dollars, the 10x calculation can produce a far larger exclusion — potentially unlimited by the base dollar figure

The 100 percent exclusion also eliminates both the capital gains tax rate and the 3.8 percent Net Investment Income Tax (NIIT) on the excluded gain. For qualifying stock acquired after September 27, 2010, the excluded gain is not an AMT preference item. The OBBBA extended that same AMT protection to the new three-year and four-year partial exclusion tiers.

Requirements for QSBS Eligibility

Shareholder Requirements

The exclusion is available only to non-corporate taxpayers - individuals, certain trusts and estates, and partners or S corporation shareholders receiving pass-through treatment. A C corporation cannot claim the exclusion, regardless of how long it holds qualifying stock.

Original Issue Requirement

This requirement causes more issues for secondary-market buyers than any other rule. The taxpayer must have acquired the stock at its original issue - directly from the issuing corporation, in exchange for cash, property (not including stock), or services. Stock purchased from a prior holder, on a secondary platform, or in an employee-to-employee transfer generally does not qualify. Rollover equity and secondary purchases, even of otherwise-qualifying shares, typically fail this test.

Holding Period Requirements

For pre-OBBBA stock, there is no partial benefit before year five. The holding period runs from the acquisition date - which for employees who early-exercise options under an 83(b) election begins at exercise, not at vesting. This timing difference is critical: an employee who vests over four years but waits to exercise until vesting may find that the five-year clock extends beyond the company's probable exit window. Early exercise is worth understanding before the company raises its next round.

Corporation Requirements for Qualified Small Business Stock

Domestic C Corporation Only

Only a domestic C corporation can issue QSBS. S corporations, partnerships, and LLCs taxed as partnerships do not qualify. An LLC that has elected C corporation tax treatment may be able to issue qualifying stock, provided the entity structure is properly established. A company that converts from an S corporation to a C corporation may issue QSBS after conversion - the clock starts at that point, not from the original formation date.

Aggregate Gross Assets Test

At the time the stock was issued and immediately after, the issuing corporation's aggregate gross assets must not have exceeded the applicable threshold: $50 million for pre-OBBBA issuances, $75 million for stock issued after July 4, 2025 (indexed for inflation beginning in 2027).

The test is applied at issuance. If a company later grows past the threshold, that does not retroactively disqualify previously issued stock. But new stock issued after the company crossed the threshold will not qualify — a timing point that matters in fast-scaling companies.

Active Business and Qualified Trades or Businesses

During substantially all of the taxpayer's holding period, the corporation must be actively conducting a qualified trade or business. Section 1202 specifically excludes certain service-based businesses, such as those in health, law, engineering, accounting, consulting, financial services, brokerage, banking, insurance, leasing, and farming.

The line between qualifying and excluded businesses is not always obvious. A software company generally qualifies. A staffing firm often does not. Companies that pivot after initial investment should reassess whether the active business requirement continues to be satisfied throughout the holding period. A holding company structure layered above an operating C corporation requires its own analysis.

Section 1202 for Startup Founders and Employees

For founders and employees, QSBS planning begins before the stock is issued — not at the liquidity event. The decisions made at incorporation and at the time of initial equity grants shape whether Section 1202 is even available years later.

Early Exercise and the 83(b) Election

Filing an 83(b) election after early-exercising unvested stock options starts the Section 1202 holding period clock at exercise, not at vesting. Combined with a low 409A valuation at the time of exercise, early exercise can mean the five-year (or three-year, for post-OBBBA stock) clock completes well before a likely exit. The planning window is tight: early exercise typically needs to happen before a large funding round pushes the company's aggregate gross assets past the applicable threshold.

Timing Exercises and the Asset Threshold

Employees and founders who want to protect QSBS eligibility need to know where the company sits on the asset scale at the time of their exercise. If the company has raised enough capital to exceed $50 million (or $75 million for post-OBBBA grants) in aggregate gross assets, stock acquired at that exercise will not be QSBS. This is a real planning decision that requires a definitive answer from a tax advisor before each exercise, rather than a mere theoretical edge case or rough guess.

Understanding stock options tax treatment alongside QSBS eligibility also matters for AMT planning. For ISOs, early exercise can trigger AMT in the year of exercise, and the interaction between AMT and the Section 1202 exclusion is worth modeling before a decision is made. See also different types of equity compensation for a broader look at how RSUs, ISOs, and NSOs each interact with Section 1202.

Family Stacking and Estate Planning

The per-taxpayer, per-issuer structure of Section 1202 creates planning opportunities for families. Each individual taxpayer has a separate cap for each qualifying issuer. Transferring shares to other family members, either by gift or bequest, can preserve the donor's holding period while creating additional cap capacity for the recipient — provided the recipient is a qualifying non-corporate taxpayer.

Non-grantor irrevocable trusts are treated as separate taxpayers and may be able to claim their own per-issuer exclusion. For families in non-conforming states, trusts administered in no-income-tax jurisdictions have attracted planning attention. This structure has real potential, but it requires genuine non-grantor status, proper administration, and economic substance. Poorly executed variations produce adverse results. Families exploring it should read how to set up a family trust and work with estate planning counsel who has specific QSBS experience.

Gifting QSBS shares to charity raises different questions. A charitable remainder trust can be part of a QSBS exit strategy, but the mechanics differ from a taxable sale, and the Section 1202 exclusion does not apply in the same way. Charitable planning alongside Section 1202 requires coordination across the estate plan, tax return, and philanthropic goals. These decisions also interact with essential estate planning documents - wills, trust agreements, and beneficiary designations that should reflect the QSBS positions explicitly.

State Tax Treatment: Where the Federal Benefit Does Not Travel

Section 1202 is a federal provision. States set their own conformity rules. In most states, the federal exclusion is also respected at the state level. But several states do not conform:

- Non-conforming (no exclusion): California, Alabama, Mississippi, and Pennsylvania. In these states, gains that are fully excluded federally are taxable at the state's ordinary or capital gains rates.

- Partial conformity: Hawaii and Massachusetts offer limited state-level benefits.

- New Jersey: Enacted conformity in 2025, effective for tax years beginning January 1, 2026.

- Washington, D.C.: Enacted emergency legislation in late 2025 to decouple from key OBBBA Section 1202 enhancements, adding complexity for D.C. residents.

For a California founder with $10 million in federally excluded QSBS gain, the state bill can exceed $1.3 million. Some founders consider establishing a domicile in a conforming state before a liquidity event. That strategy is legitimate in principle but requires genuine behavioral change, documented well in advance. California in particular has a long history of asserting residency claims on gain accrued during a California residency period. More aggressive approaches, such as using offshore structures, carry distinct risks and are analyzed separately in discussions of tax havens.

Common Section 1202 Disqualification Pitfalls

Redemption Rules

Section 1202 contains specific anti-abuse rules around stock redemptions. If the corporation redeemed stock from the taxpayer, or from a related person, within a defined window around the issuance of the QSBS, that stock may be disqualified. Separate rules apply to significant company-wide repurchases. Companies that process departing employee buybacks or run tender offers near a QSBS issuance need to assess these rules carefully.

Business Pivots

The active business requirement applies during substantially all of the holding period. A company that pivots from a qualifying industry into an excluded one — say, from software into financial services — may jeopardize the QSBS status of existing shares. Investors in early-stage companies that evolve substantially over a five-year holding period should assess this question before assuming their exclusion is still clean.

Documentation Failures

The burden of proof rests entirely with the taxpayer. The IRS does not have an obligation to prove disqualification. At minimum, the taxpayer claiming Section 1202 benefits should have: the original stock purchase or option exercise agreement, a representation or attestation letter from the company confirming its qualified status and asset levels at issuance, evidence of the active business throughout the holding period, and a clear basis calculation. These records may be needed a decade after issuance, at a time when companies have been acquired, wound down, or had key personnel depart. See also protecting your assets for a broader look at documentation disciplines that support legal and tax defensibility.

Real-World Scenarios

The Employee Who Early-Exercised Before the Raise

An engineer joins a Series A company in 2021, early-exercises options in 2022, and files an 83(b) election within 30 days. The company's aggregate gross assets at the time are well below $50 million. She holds through a 2027 acquisition. Her five-year clock completed before the exit. She lives in Texas. The combined result is no federal and no state income tax on the excluded gain. The planning moment was the early exercise in 2022 - before a subsequent fundraising round pushed the company past the threshold.

The Founder Navigating an Earlier Exit Under the OBBBA

A founder issues stock after July 4, 2025, with the company's gross assets below $75 million. An acquisition offer arrives in year four. Under prior law, a year-four sale would have produced no exclusion. Under the OBBBA, a 75 percent exclusion is now available. The founder models the after-tax proceeds at year four versus year five, accounts for the timing risk of holding longer, and makes an informed decision. That is precisely what the new tiered structure was designed to enable.

The California Founder Who Needs a Different Strategy

A California-based founder faces $12 million in federally excluded QSBS gain and a potential state tax bill exceeding $1.5 million. She and her advisors evaluate relocation, a charitable remainder trust strategy for a portion of the position, and gifting shares to family members in conforming states. After weighing the realistic feasibility of each approach - including the documentation burden of establishing genuine California non-residency - she proceeds with the federal exclusion and plans the state liability as part of managing the overall financial windfall.

Portfolio Strategy and Concentration Risk

The Section 1202 exclusion improves the after-tax math on private investment substantially. It does not change the underlying investment risk. A concentrated position in a single private company carries real liquidity and business risk regardless of how favorable the wealth management process makes the tax treatment look.

Investors with qualifying positions in multiple companies can potentially capture the exclusion across multiple issuers, each with its own cap. That makes disciplined portfolio construction across qualifying private companies genuinely tax-advantaged. Compare this to dollar-cost averaging vs. lump sum deployment in public markets — the QSBS structure rewards concentration in qualifying private companies that most public-market strategies would discourage.

For ultra-high-net-worth investors managing large private equity allocations, understanding the interaction between QSBS, deferred compensation, and other tax-deferred positions matters.

Tracking Your Section 1202 Positions

Most Section 1202 planning work happens before a liquidity event. The operational work - tracking holding periods, basis, company qualification evidence, prior exclusions, and associated documents — happens continuously over years, across positions that may be held by different family members, trusts, and entities.

Platforms like Kubera are designed for balance sheets with this level of complexity. Kubera allows founders, investors, and financial advisors to track private equity positions alongside public holdings, real estate, and other assets in a single view — including acquisition dates, custom notes for holding period milestones, and document storage for QSBS qualification records.

For families managing QSBS across multiple companies and multiple taxpayers, a consolidated platform materially reduces the risk that something important falls through the cracks across a decade-long planning horizon. The tax planning itself belongs with your CPA and tax attorney. The tracking belongs in a system you own and review regularly.

Tax Filing and Compliance

Gain from QSBS is reported on Schedule D and Form 8949, with the Section 1202 exclusion identified separately. The IRS generally has three years from the filing date to assess additional tax, which extends to six years for substantial understatements of income. Large Section 1202 exclusions can attract scrutiny, and the taxpayer's ability to defend the position depends on records that may have been created years earlier.

Working with a tax advisor who specializes in QSBS is not optional at this end of the process. For complex positions — multiple companies, trusts, gifted shares, early exercises — the filing itself is technical work. The deferred compensation and equity compensation planning that preceded a QSBS exit needs to be reflected accurately in the return. Engage a specialist, preserve your records, and treat audit readiness as a standing practice, not an afterthought.

Frequently Asked Questions

Does an S corporation qualify to issue qualified small business stock?

No. Only domestic C corporations can issue QSBS. An LLC or S corporation that converts to a C corporation may issue qualifying stock from the conversion date forward, provided all requirements are met at that time.

What happens to QSBS eligibility if the company grows past the asset threshold after I invest?

The aggregate gross assets test applies at issuance. Stock issued while the company was under the threshold is not retroactively disqualified if the company later exceeds it. But new stock issued after the company crossed the threshold will not be qualified small business stock.

Do the OBBBA changes apply to stock I already hold?

No. The OBBBA enhancements — higher cap, lower holding period, higher asset threshold — apply only to QSBS acquired after July 4, 2025. Pre-OBBBA stock follows the prior rules, including the five-year holding period and $10 million cap.

Can I defer gain if I sell QSBS before the required holding period?

Section 1045 allows taxpayers to defer gain from a QSBS sale before the holding period is satisfied by rolling proceeds into replacement QSBS within 60 days of the sale. This defers rather than excludes the gain, and the replacement stock must independently qualify.

How does Section 1202 interact with stock options?

QSBS eligibility attaches to shares, not to the options themselves. For employees, the relevant acquisition date is when the options are exercised, not when they were granted. Early exercise with an 83(b) election starts the holding period earlier and is a common strategy for maximizing QSBS benefit.

My company is in California. Does that change anything for QSBS?

California does not conform to Section 1202. A California-resident shareholder will owe full California income tax on gains that are federally excluded, regardless of where the corporation is incorporated. This is a shareholder-level issue, not a company-level one.

Can a trust hold QSBS and claim the exclusion?

Non-grantor irrevocable trusts are treated as separate taxpayers and may be able to claim their own per-issuer exclusion cap. Grantor trusts are treated as the grantor for tax purposes and generally do not create a separate cap. See how to set up a family trust for background on trust structures.

Conclusion

Section 1202 can be enormously valuable - but only for founders, investors, and employees who qualify, plan deliberately, and document carefully. The OBBBA made the qualified small business stock rules more accessible: a higher asset threshold, a higher per-issuer cap, and partial exclusions at shorter holding periods for stock acquired after July 4, 2025. That is meaningful progress. But it did not simplify the underlying requirements.

The right time to understand your Section 1202 position is before the stock is issued and before any exercise decisions are made. Engage a CPA and tax attorney who specialize in QSBS. Preserve records from day one. Track your positions with the discipline the benefit demands. And if you are managing this across multiple companies, family members, or trusts, consider whether a dedicated wealth management process — and a tracking platform built for private wealth complexity — is doing the operational work that your tax outcome depends on.

The tax benefit is powerful. The documentation burden is real. For readers who treat both seriously, the result can be extraordinary.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or investment advice. Tax rules are complex and fact-specific. Consult a qualified CPA or tax attorney before acting.