Why QSBS Belongs at the Center of Your Tax Strategy

While most high-net-worth investors know QSBS exists, few use it to its full potential.

The QSBS $15 million exclusion is a powerful federal incentive under Section 1202 of the Internal Revenue Code, allowing you to bypass a 23.8% federal capital gains tax on eligible exits.

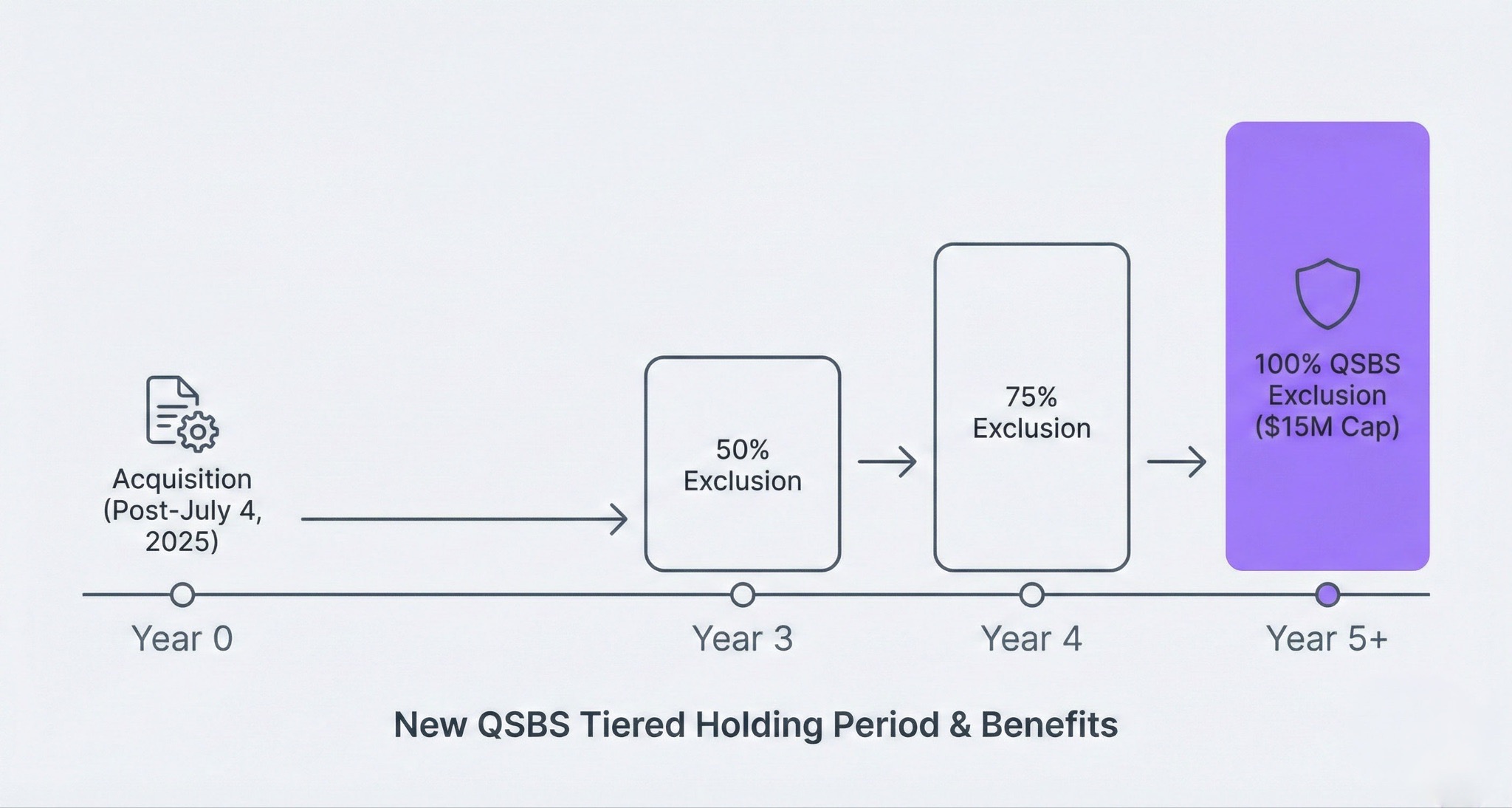

Historically, a strict five-year holding period was required to exclude 100% of gains. However, the 2025 "One Big Beautiful Bill Act" (OBBBA) expansion introduced tiered partial exclusions at three years (50%) and four years (75%) for stock acquired after July 4, 2025, offering unprecedented exit flexibility.

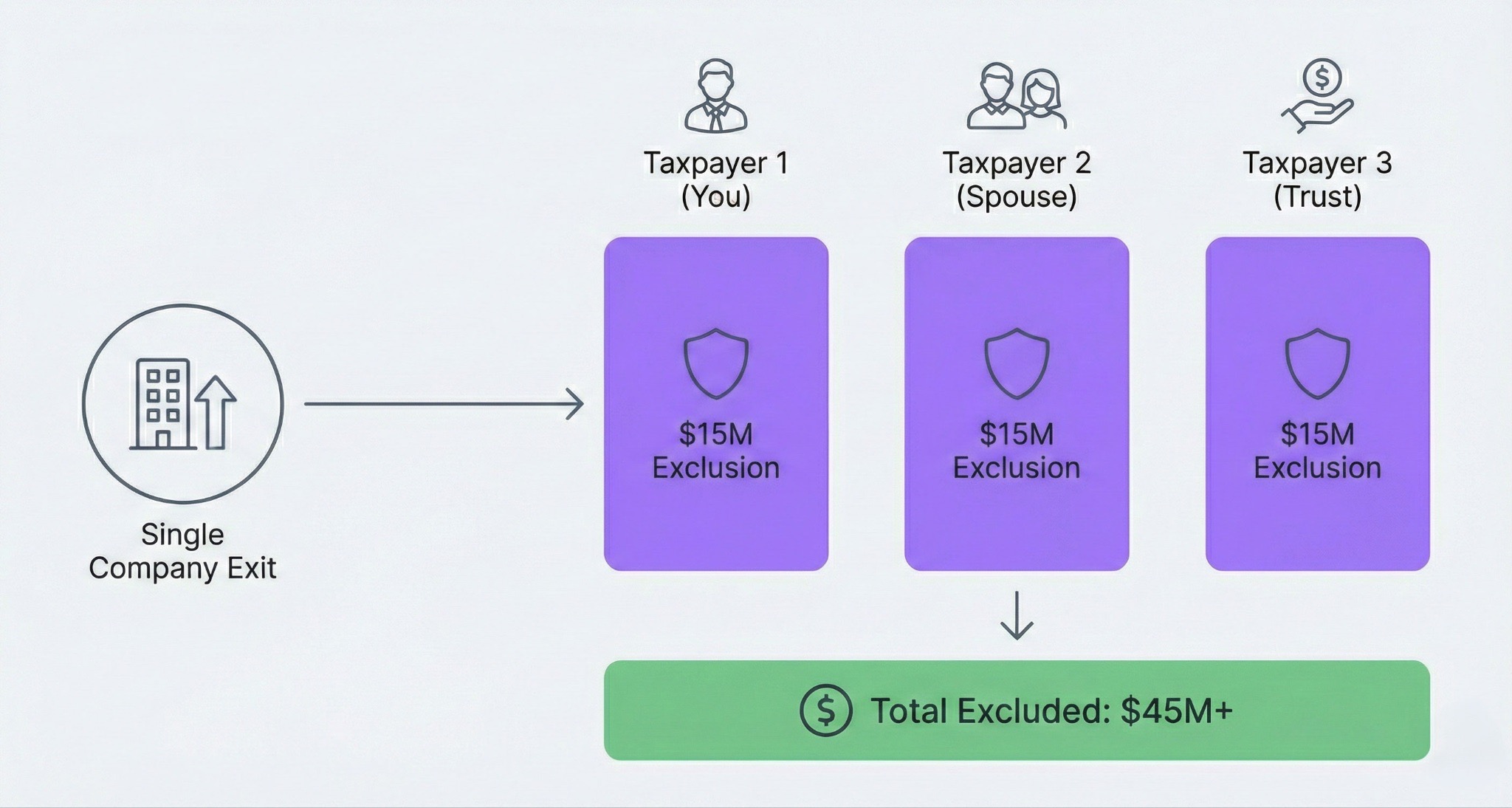

By leveraging a QSBS stacking strategy, you can multiply these gains by distributing shares across multiple taxpayers—spouses, children, and non-grantor trusts—each entitled to their own separate exclusion. Properly planned, a single company exit can shield $45 million or more.

This guide covers every dimension of QSBS for high-net-worth individuals: company and shareholder eligibility, the 2025 legislative changes, stacking mechanics, state tax pitfalls, estate planning integration, and the documentation required to defend your exclusion under IRS scrutiny.

The $15 Million Tax-Free Opportunity

QSBS Allows Up to $15 Million Per Company

The Section 1202 capital gains exclusion applies per taxpayer, per qualifying company. If you invest in five qualifying companies and each generates $15 million in gains, you owe zero federal tax on all of them.

This is not a loophole - Congress deliberately designed QSBS to reward startup risk-taking.

The 2025 Expansion Raised Both Caps

Signed into law on July 4, 2025, the One Big Beautiful Bill Act (OBBBA) represents the most significant expansion of QSBS tax benefits since 2010.

For QSBS acquired on or after July 4, 2025, the exclusion cap increased from $10 million to the greater of $15 million or 10 times the taxpayer's adjusted basis.

Each Portfolio Company Provides a Separate Exclusion

The exclusion resets for every qualifying company you invest in. A ten-company angel portfolio could generate $150 million in combined federal exclusions, making QSBS one of the most powerful wealth-building tools under the Internal Revenue Code (IRC).

What Is Qualified Small Business Stock?

Section 1202 Tax Incentive for Small Business Investments

Qualified Small Business Stock (QSBS) refers to shares in a domestic C-corporation that meet specific requirements under Internal Revenue Code (IRC) Section 1202. Congress created this incentive to channel private capital toward early-stage American businesses.

The benefit targets founders, employees, and outside investors, applying strictly at the individual taxpayer level, not the company level.

The 100% Federal Capital Gains Tax Exclusion

At the five-year mark, qualifying investors pay zero federal capital gains tax on their gains, up to the exclusion cap. For a startup executive who grows their stock value from $200,000 to $18 million, the federal tax savings can exceed $3.6 million.

New Tiered Holding Periods Reduce the Wait

For QSBS acquired after July 4, 2025, taxpayers can now exclude gains based on a new tiered schedule:

- 3 years: 50% exclusion (effective federal rate ~15.9%)

- 4 years: 75% exclusion (effective federal rate ~7.95%)

- 5+ years: 100% exclusion (zero federal tax)

Before the One Big Beautiful Bill Act (OBBBA), investors had to wait five full years for any exclusion at all.

Company Eligibility Requirements

Qualifying Business Structure

To qualify, the issuing company must pass three strict structural tests:

- Domestic C-corporation: LLCs, S-corps, and partnerships do not qualify.

- Gross assets under $75 million: Measured both before and immediately after the stock issuance.

- 80% active assets: At least 80% of the company's assets (by value) must be used in the active conduct of a qualified trade or business.

Crucially, the aggregate gross assets test measures assets at tax basis, not fair market value. A company worth $200 million on paper may still qualify if its book-value assets stay under $75 million.

Excluded Industries

Under Section 1202(e)(3), Congress explicitly excluded specific industries from QSBS treatment:

- Personal services: law, health, accounting, consulting, financial services, brokerage

- Hospitality: hotels and restaurants

- Banking, insurance, leasing, and investing

- Farming and natural resource extraction

Conversely, technology, life sciences, software, and manufacturing companies commonly qualify.

Shareholder Eligibility Requirements

Must Purchase Stock at Original Issuance Directly from the Company

The QSBS original issuance requirement is strict. You must receive shares directly from the issuing corporation itself.

Secondary Market Purchases Do Not Qualify

This rule catches many sophisticated investors off guard. A secondary purchase of Series B preferred shares looks identical to a primary issuance on paper, but only the primary buyer is eligible for the QSBS exclusion.

Eligible Holder Types

Eligible holders include individuals, certain non-grantor trusts, partnerships, LLCs taxed as partnerships, and S-corporations. The tax benefits must pass through to non-corporate taxpayers at the ultimate level.

Corporations Cannot Claim QSBS Benefits

A C-corporation that invests in another C-corporation cannot use the Section 1202 exclusion. The QSBS benefit exists exclusively for non-corporate taxpayers.

QSBS Stacking: Multiplying the $15M Exclusion

Per-Taxpayer Benefit Structure

Here's what you need to know about stacking: The $15 million exclusion belongs to the taxpayer, not the investment itself. This structure creates powerful planning leverage:

- The $15 million exclusion applies per taxpayer, per company.

- Strategic gifting to a spouse creates two entirely separate exclusions.

- Non-grantor trusts qualify as independent taxpayers under the IRC.

Family Wealth Transfer Strategy

A client can set up non-grantor trusts for each child, granting each trust its own QSBS exclusion. With four children and post-July 4, 2025 QSBS, that adds $60 million in exclusions beyond the parents' base $15 million limit.

Example: $45 Million Family Exclusion

- Taxpayer 1 (you): $15 million exclusion on Company A

- Taxpayer 2 (spouse): $15 million exclusion on same Company A

- Taxpayer 3 (irrevocable trust): $15 million exclusion on same Company A

- Total excluded from federal tax: $45 million - on a single company exit

Section 1045 Rollover Strategy

If an attractive acquisition offer arrives before your five-year clock expires, a Section 1045 rollover lets you defer full taxation by reinvesting the proceeds into new QSBS.

- Minimum 6-month holding period required before you can execute the rollover.

- You must reinvest the proceeds within a strict 60-day window.

- Reinvest 100% of proceeds to defer the entire gain—partial reinvestment shelters only the portion rolled.

- Tacks (carries over) your original holding period onto the new QSBS position. Contrary to a common misconception, the clock does not restart! This keeps you perfectly on track for the 100% exclusion.

QSBS in Estate Planning

Transferring Without Losing QSBS Status

Most non-arm's-length transfers preserve the stock's QSBS qualification and holding period:

- Lifetime gifts preserve the original holding period for the recipient.

- Inheritance maintains the decedent's original acquisition date and holding period.

- Divorce settlements do not disqualify the transferred shares.

Transfers That Destroy QSBS Eligibility

Beware of these three transfer types that void QSBS status permanently:

- Sales or exchanges for value to another party.

- Contributions to C-corporations—transferring QSBS into a C-corp kills the exclusion.

- Certain transfers to foreign or offshore entities.

Always work with a qualified estate attorney before moving shares into any new structure.

Portfolio Strategy for QSBS Investments

Balancing Risk and Tax Benefits

QSBS represents concentrated private equity exposure by definition. While the tax exclusion drastically improves your risk-adjusted return, it cannot eliminate the fundamental risk of startup failure.

See Kubera's analysis of dollar-cost averaging vs. lump-sum investing to understand how to deploy capital across multiple QSBS positions systematically.

Exercising Stock Options for QSBS

Early exercise of stock options is a powerful QSBS strategy. Because the holding period strictly begins at the date of exercise (not the grant date), exercising early starts your clock sooner and locks in your eligibility before the company's gross assets breach the $75 million threshold.

Coordinate this decision carefully with AMT implications and personal liquidity needs.

Cross-Border Considerations

Non-U.S. residents generally cannot claim QSBS benefits, while U.S. citizens abroad face complications because the IRS taxes worldwide income. Global entrepreneurs often hold startup equity through U.S. LLCs to preserve eligibility, but you must coordinate with advisors in both jurisdictions before structuring international holdings.

State Tax Treatment

Non-Conforming States

This is the most overlooked QSBS risk: Federal exclusion does not guarantee state exclusion. As of late 2025, several states actively diverge from the federal QSBS exclusion:

Residency Planning

To maximize your exit, consider establishing legal domicile in a tax-friendly state before a liquidity event occurs.

However, state tax authorities heavily scrutinize moves that happen close to major liquidity events. Establish genuine residency well in advance—move your primary residence, voter registration, banking, and professional relationships years before an exit.

Disqualification Risks

Company Actions That Void QSBS

The company itself can accidentally void your QSBS status through:

- Certain stock redemptions in the one-year period before or after your issuance date.

- The business model shifts into excluded industries (e.g., pivoting to financial services).

- Note: Breaching the $75 million gross asset threshold during later fundraising rounds does not void your existing QSBS. It only prevents the newly issued shares from qualifying.

The Gross Assets vs. Valuation Distinction

A company with a $200 million post-money valuation may still qualify for QSBS issuances if its gross assets—measured at tax basis—stay under $75 million. Software and IP-heavy companies typically qualify well into their growth stage.

Documentation Requirements

The IRS places the burden of proof entirely on the taxpayer in QSBS disputes. Document everything at the time of investment by maintaining airtight records:

- QSBS attestation letters from the issuing company confirming eligibility at issuance.

- Stock purchase agreements showing shares came from original issuance, not secondary sales.

- Continuous ownership records proving an unbroken holding period.

Multi-Company QSBS Strategy

The per-company structure of QSBS turns a diversified angel portfolio into a tax optimization engine. Ten qualifying exits, each generating $15 million in gains, produce $150 million in total federal exclusions across a single investor.

- Compounding Benefits: Active angel investors build exclusion potential that compounds with each new investment.

- Strategic Sequencing: Sell positions that have crossed the five-year mark first for maximum tax benefit.

- Section 1045 Utilization: Roll shorter-held positions if an early exit is necessary.

- Meticulous Tracking: Each QSBS position has its own acquisition date—track each holding period separately to optimize your tiered exclusions.

Legislative Changes and Future Outlook

The 2025 Expansion at a Glance

(Note: Gain subject to the 50% exclusion carries an effective federal rate of 15.9%. Gain subject to the 75% exclusion carries an effective federal rate of 7.95%.)

Political Risk Factors

QSBS has enjoyed bipartisan support for decades, with expansions in 2009, 2010, and again in 2025. But deficit pressures create real risk that future Congresses could modify the rules.

The prudent strategy is to execute QSBS plans under current law rather than waiting for future improvements that may never arrive.

Tax Filing and Compliance

Required Forms and Documentation

- Form 8949: Report the sale with the Section 1202 exclusion code.

- Schedule D: Calculate the net excluded and taxable Section 1202 gains.

- Supporting documents: Attestation letters, purchase agreements, and ownership records for audit defense.

IRS Audit Triggers

QSBS exclusions attract IRS scrutiny in four areas. The burden of proof rests with the taxpayer in all of them:

- Company qualification challenges: Did the issuer actually meet all requirements at issuance?

- Original issuance verification: Did you buy from the company or from another investor?

- Holding period calculation disputes: Did you actually hold the stock long enough?

- Documentation gaps: Missing attestation letters or ownership records.

Real-World Scenarios

Scenario 1: Startup Executive: $200K to $18M

- Starting position: $200,000 in founder shares

- Holding period: 6 years (exceeds 5-year threshold)

- Exit value: $18 million | Gain: $17.8 million

- Federal tax exclusion: $15 million (The flat cap applies because 10x basis is only $2 million).

- Federal tax owed: $890,400 (The remaining $2.8 million in unshielded gain is taxed at the 31.8% QSBS non-excluded rate).

- Federal tax savings: ~$3.57 million (Compared to paying the standard 23.8% rate on the full $15M).

- California state tax (if resident): ~$2.37 million still owed (13.3% on the full $17.8M gain).

- Relocation strategy: Establishing domicile in Texas/Florida before exit eliminates state tax entirely.

Scenario 2: Angel Investor in 10 Companies, $80M in Gains

- Total qualifying gains across 10 companies: $80 million

- Four taxpayers (family members + non-grantor trusts) x $15M = $60 million excluded.

- Remaining $20 million managed via Section 1045 rollovers into new QSBS.

- Coordinated exit timing maximizes annual benefit.

- Net federal tax exposure: Significantly reduced with proper planning.

Scenario 3: Global Entrepreneur U.S. Citizen in Singapore

A U.S. citizen founder runs her company from Singapore. While Singapore's territorial tax system may not tax foreign-sourced gains, the U.S. taxes its citizens on worldwide income regardless of where they live.

She holds startup equity through a U.S. LLC to preserve QSBS eligibility for the federal exclusion, coordinating with tax advisors in both jurisdictions to avoid double taxation and structure her exit efficiently.

Implementing Your QSBS Strategy

Portfolio Assessment — Start Here

- Identify all private company positions: Including unvested options, restricted stock, and convertible notes.

- Review stock options for exercise timing: Early exercise before the $75M asset threshold breach preserves eligibility.

- Calculate potential exclusions: Map each holding period against the tiered schedule.

- Prioritize QSBS within your overall tax plan: Coordinate with Opportunity Zones and charitable giving strategies.

Advisor Coordination

QSBS planning demands a team of specialists:

- QSBS-focused tax attorneys for complex transactions, trust structures, and gifting strategies.

- CPAs specializing in Section 1202 for annual filing, documentation, and audit readiness.

- Wealth advisors to integrate QSBS into your broader investment and estate plan.

- Annual reviews to track each position's qualification status as companies evolve.

Track Your QSBS Portfolio with Kubera

Managing multiple QSBS positions creates real complexity. Each position carries its own acquisition date, holding period clock, exclusion cap calculation, and supporting documentation.

Critical documentation—attestation letters, stock purchase agreements, and capitalization table records—must remain accessible and auditable for years after the exit. Spreadsheets cannot handle real-time updates or secure storage across multiple entities.

Kubera's QSBS Management Solution

Kubera provides a purpose-built platform for managing complex private wealth portfolios, including all QSBS positions:

- Centralized dashboard: Track all private company holdings across every entity.

- Secure document vault: Store QSBS attestation letters, purchase agreements, and critically, date-stamped 83(b) election filings to prove early exercise for unvested shares.

- Custom sheets and sections: Mark QSBS-eligible positions and distinguish them from non-qualifying shares.

- Acquisition date tracking: Map out your exact timeline for the new 3-, 4-, and 5-year tiered exit strategy using Fast Forward.

- Stock Options Tax tracking: Monitor ISOs and NSOs, track exercise dates, and forecast stock options tax implications to optimize your long-term capital gains vs. ordinary income rates.

- Multi-entity support: Execute stacking strategies across family members and trusts using nested portfolios.

- Unified view: See your QSBS investments alongside traditional assets—equities, real estate, crypto, and bonds.

- Advisor access sharing: Ensure your CPA and estate attorney work from the same live data.

Start Managing Your QSBS Strategy Today

QSBS represents one of the most powerful federal tax incentives available to individual investors and founders. The 2025 expansion made it more accessible, more flexible, and more valuable than at any point in the law's history.

Maximizing QSBS—through stacking, Section 1045 rollovers, tiered exit timing, and residency planning—requires meticulous recordkeeping and multi-year coordination.

Frequently Asked Questions

What is QSBS?

QSBS stands for Qualified Small Business Stock. It refers to shares in a domestic C-corporation that meet IRS requirements under Section 1202 of the Internal Revenue Code. Qualifying investors can exclude up to $15 million in capital gains per company from federal taxes.

What is the QSBS five-year holding period rule?

Historically, investors who held QSBS for more than five years could exclude 100% of qualifying gains from federal tax. Under the 2025 OBBBA expansion, investors holding post-July 4, 2025 QSBS for three years exclude 50%, and those holding it for four years exclude 75%.

What is the QSBS $75 million asset test?

The issuing company must have gross assets—measured at tax basis (original cost)—of $75 million or less at the time of stock issuance and immediately after. This threshold applies to stock issued after July 4, 2025. Shares issued before that date use the old $50 million limit.

Can California residents use the QSBS tax exemption?

No. California does not conform to the federal QSBS exclusion. California residents owe state income tax at up to 13.3% on gains that qualify for full federal exclusion. Establishing legal domicile in a no-income-tax state before an exit eliminates this state tax liability.

What is QSBS stacking?

QSBS stacking refers to strategies that multiply the per-taxpayer $15 million exclusion across multiple people or entities. Gifting shares to a spouse, children, or non-grantor trusts before a liquidity event creates separate $15 million exclusions for each recipient.

What is the Section 1045 rollover?

Section 1045 lets investors sell QSBS before the five-year mark and defer the gain by reinvesting 100% of the proceeds into new QSBS within 60 days. The investor must have held the original QSBS for at least six months before the sale.

What types of companies qualify as QSBS issuers?

Qualifying companies must be domestic C-corporations with gross assets under $75 million at issuance, with 80% of assets used in active business operations. Technology, life sciences, software, and manufacturing companies commonly qualify. Law firms, banks, restaurants, hotels, and investment funds are strictly excluded.

Disclaimer: This article provides general educational information about QSBS under Section 1202 of the Internal Revenue Code. It does not constitute tax, legal, or financial advice. Consult a qualified tax attorney and CPA before implementing any QSBS strategy.