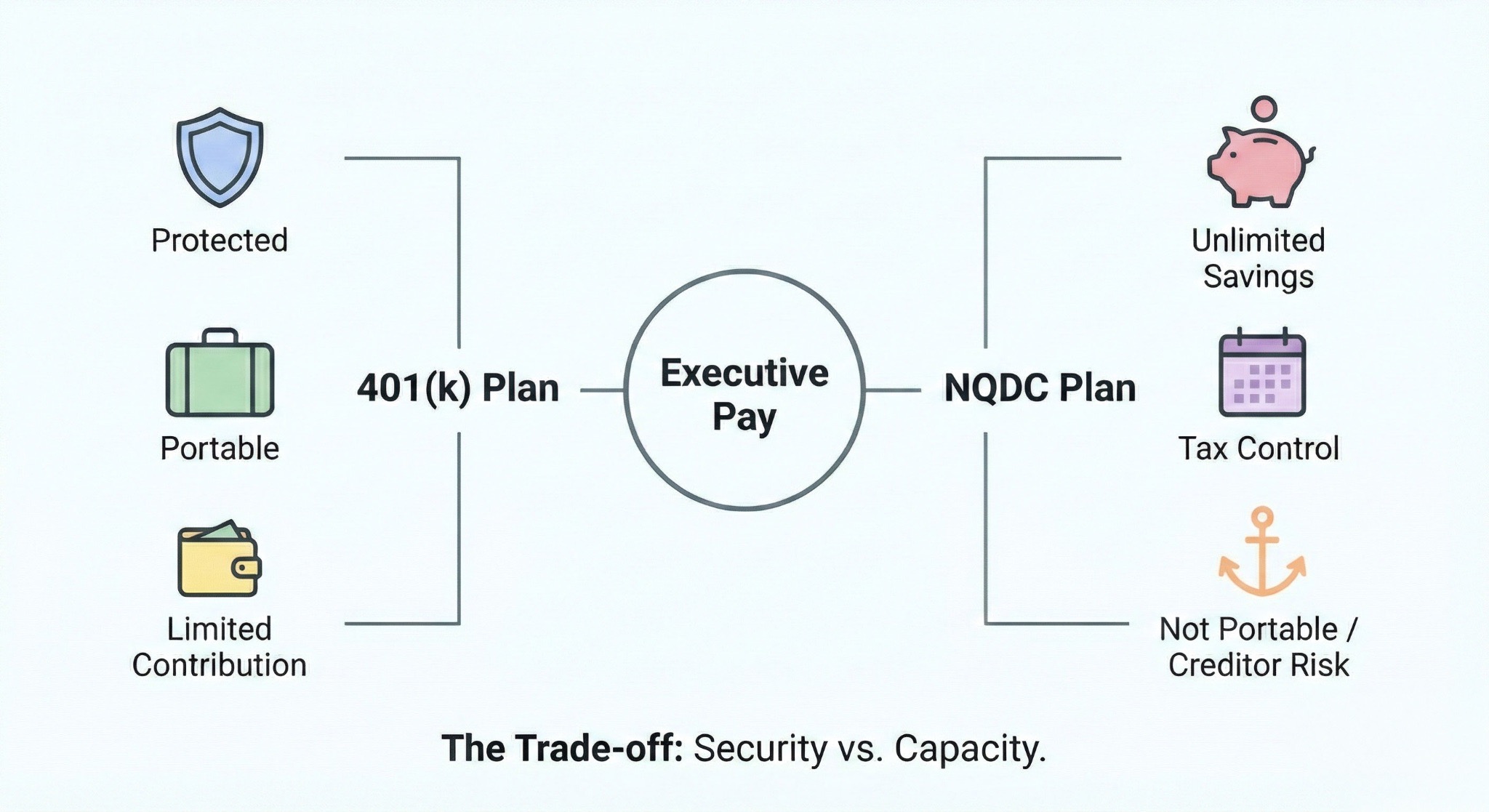

Deferred compensation lets executives postpone receiving a portion of their pay until a future date. This strategy lowers current taxable income, shifting that tax liability to retirement years when you may fall into a lower tax bracket. For high earners who already max out their 401(k) plans, a non-qualified deferred compensation (NQDC) plan unlocks savings potential far beyond IRS limits.

However, there is a distinct trade-off. Your deferred compensation remains a general asset on the company's balance sheet. You effectively become an unsecured creditor of your own employer. That single risk shapes every decision around executive compensation planning.

The 2025 Principal NQDC study found that 90% of executives consider a non-qualified plan important for retirement readiness. Assets in NQDC plans reached $235.4 billion in 2025, up from $198.8 billion the year before, according to PLANSPONSOR.

Non-Qualified Deferred Compensation Plans: The Executive’s Advantage

Employers design NQDC plans specifically for senior management and highly compensated employees to bridge the retirement savings gap created by qualified plan testing. These plans fall outside most provisions of the Employee Retirement Income Security Act (ERISA), allowing for maximum flexibility in plan design.

The IRS sets no contribution cap on NQDC plans. You may defer as much as you and your employer agree upon. Many executives defer 50% or more of base salary and some defer up to 100% of annual bonuses.

You also customize distribution schedules, aligning payouts with your retirement timeline and broader tax strategy. This flexibility makes NQDC plans a powerful tool for deferring income from peak earning years to lower-income retirement years.

Companies often call these plans "golden handcuffs" because they reward long-term commitment. If you leave the company early, you may forfeit unvested employer contributions. This retention design keeps top talent in place. Learn more about the value of unvested compensation.

Qualified Plans vs. NQDC: What Executives Need to Know

The difference between qualified and non-qualified deferred compensation drives every planning decision. Here is a direct comparison.

Qualified retirement plans like 401(k) plans have strict contribution limits. In 2026, the IRS set the employee deferral limit at $24,500. Employees age 50 and older can add $8,000 in catch-up contributions. Notably, a new "super catch-up" provision allows participants ages 60 to 63 to contribute an additional $11,250.

Executives must also navigate the new "Roth catch-up" rule. Starting in 2026, if you earned more than $145,000 (indexed) in FICA wages the previous year, your catch-up contributions must be made as after-tax Roth contributions.

NQDC plans allow unlimited additional deferrals for executives who max out these qualified plans. However, while qualified plans offer ERISA creditor protection, NQDC assets stay on the company's balance sheet until distribution.

You cannot roll NQDC funds into an IRA. The money stays with your employer until your chosen distribution date. Investment options in NQDC plans mirror popular choices but are technically "notional" investments. They tend to include stock funds, bond funds, and stable value options.

Strategic Benefits of Deferred Compensation for Wealth Building

Tax Optimization and Timing

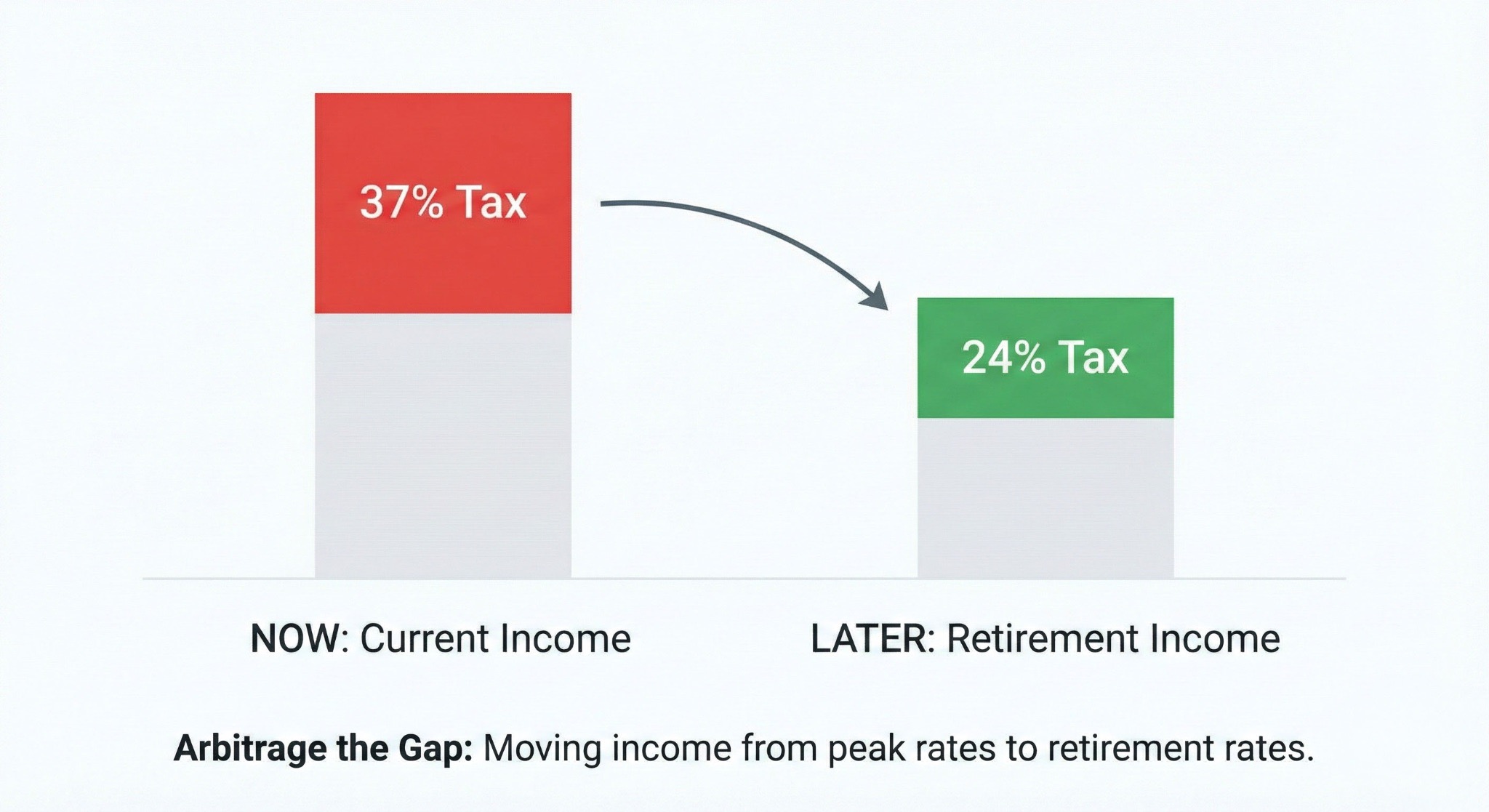

The core deferred compensation tax strategy works like this: You defer income from high-earning years, then receive that income in retirement years when you have less wage income. This shifts your tax bracket downward in both periods.

Deferring income reduces your current adjusted gross income (AGI). A lower AGI can preserve eligibility for other tax benefits and deductions. Crucially, it can also reduce exposure to the 3.8% Net Investment Income Tax (NIIT) and Medicare surtax by keeping your Modified AGI (MAGI) below the threshold triggers ($200,000 for singles; $250,000 for couples).

Your invested balances grow tax-deferred inside the plan. You pay no annual tax on investment gains. This compounding advantage grows larger with bigger balances and longer time horizons.

Strategic distribution timing lets you manage tax brackets in retirement. You coordinate distributions with Social Security, pensions, and investment income. The goal is to minimize your lifetime tax burden. Many executives spread distributions over 10 to 15 years to keep each year's taxable income in a favorable range.

Note on 2026 Tax Law: The One Big Beautiful Bill Act, signed in July 2025, permanently extended the lower individual income tax rates established by the TCJA. The top marginal rate remains at 37% rather than reverting to 39.6%. Additionally, the State and Local Tax (SALT) deduction cap has been raised to $40,000 for married couples filing jointly (up from $10,000), offering deeper tax relief for executives in high-tax states.

Practical Example: Tax Bracket Management

Sarah earns $800,000 per year as a CFO. She defers $200,000 annually into her NQDC plan. This drops her current taxable income to $600,000. She saves approximately $74,000 per year in federal taxes at the now-permanent 37% top marginal rate.

At retirement, she takes installment distributions of $100,000 per year. Combined with other income, she stays in the lower 24% tax bracket. She saves roughly 13 percentage points on every deferred dollar. Over 15 years of distributions, that adds up to significant tax savings.

Wealth Accumulation Beyond Standard Limits

NQDC enables executives earning $500,000 or more to save far beyond 401(k) limits. A $24,500 annual 401(k) deferral barely moves the needle for someone earning seven figures. NQDC plans close that gap.

Compound growth on larger balances creates substantially greater retirement wealth. An executive who defers $200,000 per year for 15 years at a 7% return accumulates over $5 million. The same return on $24,500 annual 401(k) deferrals produces roughly $630,000.

You can also defer bonuses, equity compensation vesting events, and other irregular income. This flexibility smooths your cash flow across years. It supplements traditional retirement accounts and taxable investment portfolios. Consider diversifying further with alternative investments.

Succession and Estate Planning Advantages

You can structure distributions to align with your lifestyle and legacy goals. Many plans let you designate beneficiaries who receive death benefits according to plan terms.

Coordinate NQDC distributions with trust planning and other wealth transfer strategies. Timing large distributions in specific years can fund irrevocable life insurance trusts or charitable vehicles. This layer of financial planning turns deferred compensation into an estate planning tool. Understand the tax implications through this guide to capital gains tax.

Critical Risks Every Executive Must Understand

Executive deferred compensation risks are real. They deserve the same attention as the tax benefits. Every deferral decision involves a trade-off between tax savings and financial exposure.

Creditor Risk: Your Money Sits on the Company’s Balance Sheet

NQDC balances represent unsecured general obligations of the employer. If your company files for bankruptcy, you stand in line with other general creditors. You could lose part or all of your deferred compensation.

This risk is not theoretical. The Enron collapse taught executives a painful lesson about unsecured deferred compensation when executives lost millions in deferred pay. Section 409A of the Internal Revenue Code, effective January 1, 2005, made early withdrawals from NQDC plans even harder to prevent executives from pulling cash out before a collapse.

Unlike 401(k) assets which are held in a protected trust, NQDC funds remain on the company balance sheet. Even a Rabbi Trust does not protect you from insolvency. Those assets still belong to the company's creditors in bankruptcy; the trust only protects against a new management team refusing to pay you.

Assess your employer's financial health and credit rating before deferring large amounts. Diversify risk by not concentrating all retirement savings in NQDC. Spread your wealth across qualified plans, taxable accounts, and other assets.

Liquidity and Access Restrictions

Deferral elections are typically irrevocable. You make them in the calendar year before you earn the income. Once you commit, you cannot change your mind.

You cannot access funds early except in very limited situations. Severe financial hardship or plan termination may qualify. But IRS Section 409A rules make early access extremely difficult and penalties for non-compliance are severe (immediate taxation plus a 20% penalty).

You must maintain enough liquid assets and cash flow to support your lifestyle while deferring income. Executives who defer too aggressively sometimes face cash flow crunches. Plan your deferral amounts carefully with 12 months of living expenses as a minimum liquidity buffer.

Portability Limitations When Leaving the Company

You cannot roll NQDC balances to an IRA or a new employer's plan. Leaving the company may trigger an accelerated distribution of your entire account balance. That creates an unfavorable tax event by bunching all that income into a single year.

This portability limitation creates genuine financial "handcuffs." It complicates career mobility. Before accepting a new position, calculate the full tax cost of a forced distribution from your current NQDC plan.

Concentration Risk: Too Much Tied to One Employer

Many executives already depend heavily on a single employer. They earn a salary, receive stock options, hold RSUs, and participate in NQDC plans. All of these tie directly to one company's performance.

Company stock often appears in NQDC investment options. This compounds single-company risk. If the company struggles, your current income, equity holdings, and deferred compensation all decline at the same time.

Distribution Planning and Tax Management

How Should You Structure Your Distribution Strategy?

Here is what you need to know: You choose your distribution dates at the same time you make your deferral election. Common election options include a specific age, a calendar year, retirement, or separation from service.

- Choose your trigger event. Retirement, separation from service, a fixed date, disability, death, or a change in control all qualify under Section 409A. Financial hardship is also a trigger, but only for "unforeseen emergencies" as strictly defined by the IRS.

- Decide between lump sum and installments. Balance the tax hit against your income needs and investment preferences.

- Set your distribution timeline. Align it with your broader retirement income plan. Many executives choose 10-year or 15-year installment schedules to smooth out the tax liability.

- Review change-of-control provisions. Mergers, acquisitions, or company sales can trigger mandatory lump-sum distributions regardless of your original election.

Tax Implications at Distribution

Distributions from NQDC plans face taxation as ordinary income. Federal, state, and local taxes all apply. State tax rates vary widely. An executive in California pays a top effective state rate of 14.4% (13.3% income tax + 1.1% uncapped payroll tax). One in Texas pays zero.

FICA taxes apply earlier, under the "Special Timing Rule." Social Security and Medicare taxes hit your paycheck when the money vests (i.e., when there is no longer a substantial risk of forfeiture), not at distribution. This is a key difference from qualified plans.

Consider future tax rate projections and potential tax law changes. Coordinate distributions with Social Security timing, Roth conversions, and other taxable events. Multi-year installment distributions spread your tax burden across lower brackets.

Key Tax Fact: You pay FICA taxes on deferred compensation when you earn (or vest in) it. You pay income taxes when you receive it. This split means your distribution checks in retirement only face income tax, not payroll tax. Plan accordingly.

Integrating Deferred Compensation into Your Comprehensive Wealth Plan

NQDC should serve as one component of a diversified retirement strategy. Combine it with 401(k) plans, IRAs, taxable accounts, real estate, and alternative investments. No single vehicle should carry all your retirement weight.

Review your deferral elections annually. Base decisions on income projections, tax situation, and your employer's financial health. A company downgrade from a credit rating agency should prompt a deferral reassessment before the next enrollment window closes.

Model different distribution scenarios to optimize tax efficiency. Run projections under various tax rate assumptions. The difference between a lump sum and a 15-year installment plan can equal hundreds of thousands in tax savings by keeping you out of the top 37% bracket and reducing exposure to the 3.8% Net Investment Income Tax.

Coordinate NQDC with equity compensation. RSUs, stock options, and ESPP shares all create taxable events. Stacking a large NQDC distribution in the same year as a major RSU vesting event pushes you into the highest tax bracket. Stagger these events across years whenever possible.

Maintain enough liquidity in other accounts. You want to avoid forced early withdrawals from qualified retirement accounts. Keep taxable brokerage accounts and cash reserves accessible for near-term needs so your NQDC plan can remain untouched until its scheduled payout.

Document all plan details, elections, and distribution schedules. Store them in a secure, centralized location. Your future self will thank you when distribution dates arrive.

Tracking Deferred Compensation as Part of Your Total Net Worth

NQDC balances frequently exist outside your typical brokerage and bank accounts. Even if your plan is administered by a major firm, these assets often do not appear on your standard retail dashboard alongside your IRA or taxable brokerage account. This makes them easy to overlook.

Executives often lose track of their total compensation value. Multiple plans, accounts, and asset types spread across different providers create financial blind spots. You need a complete picture that includes unvested equity, deferred comp,qualified plans, and all investable assets.

Keep NQDC plan documents, benefit statements, and election forms organized. Review them at least once per year.Update beneficiary designations after any major life event, as NQDC plans bypass your will and pay out directly to named beneficiaries.

Make sure your spouse, family member, or estate executor can locate all deferred compensation information. A well-documented plan protects your family if something unexpected happens.

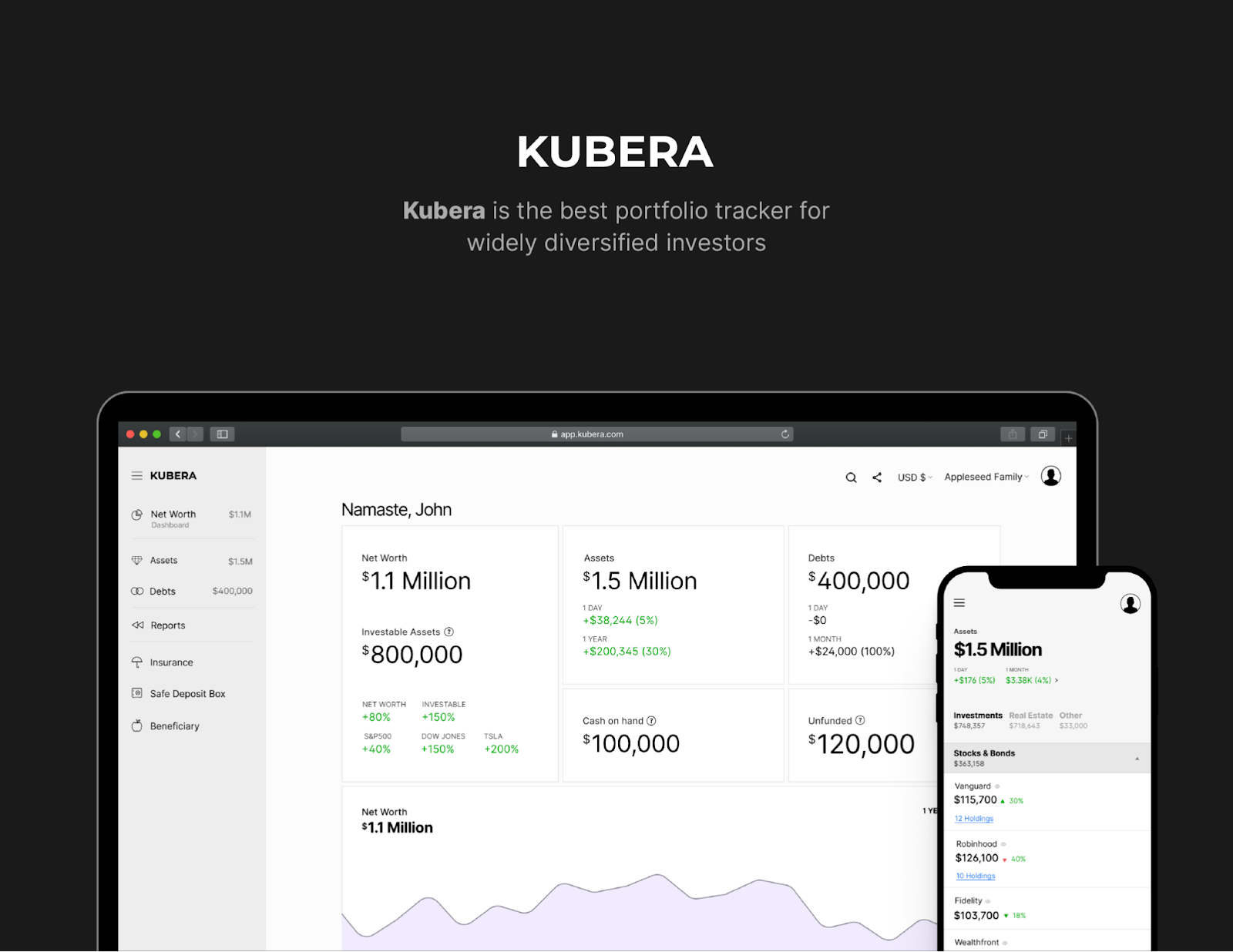

Track Your Complete Financial Picture with Kubera

High-net-worth individuals and executives need more than a standard budgeting app. You need a comprehensive balance sheet that captures complex assets, including NQDC, unvested equity, and alternative investments.

Kubera gives you a centralized dashboard to monitor every component of executive wealth. Track bank accounts, investment portfolios, retirement accounts, deferred compensation balances, real estate, crypto, and private equity in one place.

- Track "Shadow" Assets: Manually add and track NQDC balances and unvested stock options alongside your liquid assets for true net worth visibility.

- Digital Safe Deposit Box: Store critical documents like plan agreements, irrevocable election forms, and distribution schedules securely. Ensure your documents are accessible when future distribution triggers occur.

- Estate Preparedness: Purpose-built sharing controls let you grant read-only access to your spouse, estate executor, or financial advisor to ensure no asset is lost.

Stop relying on spreadsheets to track your financial future. Sign up for Kubera today.

Frequently Asked Questions About Deferred Compensation

What is non-qualified deferred compensation (NQDC)?

Non-qualified deferred compensation is an arrangement where an executive defers a portion of salary, bonuses, or other pay to a future date. Unlike 401(k) plans, NQDC plans have no IRS contribution limits. They fall outside most ERISA protections. Employers design these plans specifically for highly compensated employees and senior leadership.

Can I lose my deferred compensation if my employer goes bankrupt?

Yes. NQDC balances are unsecured general obligations of the employer. In a bankruptcy, participants stand in line with other general creditors. Unlike 401(k) assets which are held in trust and protected under ERISA, NQDC funds remain on the company's balance sheet. This creditor risk is the most significant downside of any deferred compensation plan.

How is deferred compensation taxed at distribution?

Distributions face taxation as ordinary income at federal, state, and local levels. However, FICA taxes (Social Security and Medicare) apply in the year the compensation is earned or vested, not at distribution. Executives can spread their tax liability by electing installment payments over multiple years.

Can I roll my NQDC plan into an IRA if I leave my job?

No. You cannot roll NQDC balances into an IRA or a new employer's qualified plan. Leaving the company may trigger an accelerated distribution of the entire balance. This creates a potentially large tax event in a single year.

What is the difference between qualified and non-qualified deferred compensation?

Qualified plans like 401(k)s follow strict IRS contribution limits and offer ERISA creditor protection. NQDC plans have no contribution limits, offer no statutory creditor protection, and cannot be rolled into IRAs. NQDC plans supplement qualified retirement plans for executives who max out standard limits.

How much can I defer in a non-qualified deferred compensation plan?

The IRS sets no limit on NQDC deferrals. You and your employer agree on the amount. Many executives defer 50% or more of base salary and up to 100% of bonuses. The only limit comes from the plan's own terms and your need for current cash flow.

When should I start taking distributions from deferred compensation?

You choose distribution timing at the time you make your deferral election. Common triggers include retirement, a specific age, a fixed calendar year, or separation from service. Coordinate timing with Social Security, Roth conversions, and other income sources to minimize your lifetime tax burden.