What Is a Proof of Funds Letter?

A proof of funds letter is a document confirming that you have available, accessible financial resources to complete a transaction. The purpose is straightforward: a seller, lender, fund manager, or other recipient wants evidence that the money is real before advancing the deal.

You may also see this document called a letter of proof of funds. Both terms describe the same thing. The format varies by context and by what the recipient will accept.

Common formats include:

- A letter from your bank on official letterhead, listing your name, the account type, and the current balance

- A brokerage or investment account statement downloaded directly from the institution

- A formal signed financial summary showing liquid assets across multiple accounts

- A proof of wealth letter or net worth statement that includes assets, liabilities, and a net worth figure

A proof of funds letter differs from a bank statement in one important way. A bank statement is a historical transaction record. A proof of funds letter (or official bank letter) is a current confirmation specifically addressed to the transaction or recipient. Some recipients require the former. Others require the latter. Many accept either.

A proof of funds letter also differs from a proof of financing letter. Proof of financing (such as a mortgage preapproval) shows that a lender has committed to funding a purchase based on your creditworthiness. Proof of funds shows that your own money is present and accessible. In many transactions, a recipient wants to see both.

For a broader picture of your financial position, see our guide to building a statement of net worth and our personal balance sheet guide.

When Do You Need Proof of Funds?

Proof of funds for real estate

Proof of funds for real estate transactions is one of the most common use cases. Sellers and their agents want confirmation that a cash buyer or a financed buyer has the required down payment and closing costs before accepting an offer. In competitive markets, a strong proof of funds document distinguishes serious buyers from those who may not be able to close.

Earnest money deposits also sometimes require proof of funds. The seller wants confidence that you can support your offer, not just that you can write a check today.

Proof of funds for a mortgage

Proof of funds for a mortgage serves a different purpose than a preapproval letter. During underwriting, your lender verifies that the down payment funds exist in your accounts, that you have enough for closing costs, and that post-closing reserves meet program minimums. Lenders typically request two to three months of complete bank statements during this process. A proof of funds bank statement review is a standard part of mortgage underwriting for conventional, jumbo, and non-QM loans alike.

Hard-money and bridge financing

Hard-money lenders and bridge lenders often work on compressed timelines. They want quick evidence that you can fund the equity portion of the transaction and cover carrying costs. A current, well-organized financial summary moves these requests faster than scrambling to assemble individual statements at the last minute.

Private investments

Some platforms and fund managers ask investors to document available capital before accepting a commitment, particularly for high-minimum or illiquid offerings. This is separate from accredited investor verification. The fund wants to know you can fund the commitment you are about to make.

Urgent and time-sensitive transactions

In competitive real estate markets and fast-moving private deals, having clean, current proof of funds ready before you need it gives you a meaningful advantage. Delays in documentation have cost buyers deals. Having a shareable, up-to-date financial snapshot available on short notice puts you in a stronger position.

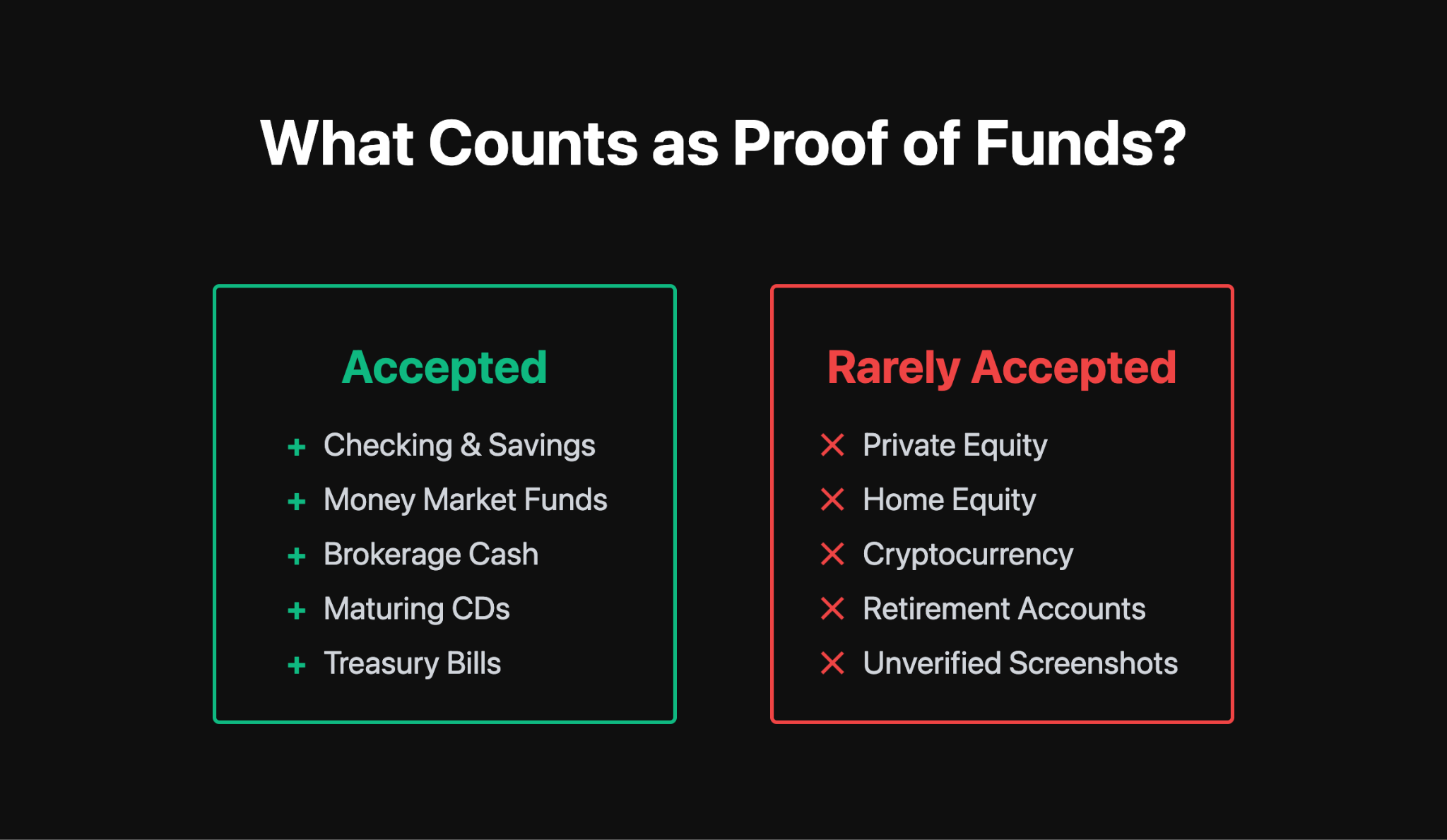

What Counts as Proof of Funds?

Recipients vary in what they will accept. The following assets typically qualify when properly documented:

- Checking and savings account balances at FDIC-insured banks

- Money market fund balances, including money market accounts and fund positions

- Brokerage cash, money market holdings, and cash equivalents

- Certificates of deposit (CDs) that are accessible or maturing before the transaction close date

- Treasury bills and short-term liquid instruments

Some recipients will also accept:

- Marketable securities such as publicly traded stocks and bonds, if the recipient specifies they will accept them and if the account statement shows current market value

The key question in every case is liquidity. Is the money accessible now, in a form the recipient can verify, without significant delays or penalties?

What Usually Does Not Count the Same Way?

Recipients commonly discount or reject the following:

- Illiquid private investments: private equity, venture fund interests, startup equity, and private real estate holdings

- Home equity: this is an asset, but it requires a sale or a cash-out refinance to convert to cash, making it inaccessible for a time-sensitive transaction

- Retirement accounts with access restrictions: early-withdrawal penalties and tax obligations reduce the effective liquidity of these accounts, and many lenders apply a discount or exclude them entirely

- Cryptocurrency: some recipients will not accept it; others may, at a discount. Its value is volatile, and verifying source and ownership can be complicated

- Unverified screenshots: images of account balances taken with a phone, without institutional letterhead or a timestamp, are generally not accepted as documentation

Proof of Funds Letter vs. Bank Statement vs. Proof of Wealth

These three document types are related but serve different purposes. Using the wrong one for a given situation causes unnecessary back-and-forth.

Proof of funds is narrowly focused: what liquid assets are available for this transaction right now. A proof of wealth letter is broader, showing total financial health across all assets and liabilities. Knowing which one the recipient actually needs saves you time assembling the wrong documentation.

How to Get a Proof of Funds Letter Quickly

Follow these steps to move fast without errors.

- Identify which accounts you will use. Focus on liquid, accessible funds that cover the full transaction amount, estimated closing costs, and any required reserves.

- Get a current statement or bank letter for each account. Most banks issue official letters within one business day for existing customers. For brokerage accounts, download a current statement directly from the platform.

- If the recipient needs a combined view across accounts, prepare a simple one-page summary: institution name, account type, current balance, and your name on each account. Sign and date the summary page.

- Check the freshness requirement. Most recipients want documentation dated within 30 to 90 days. For fast-moving real estate offers, 30 days is the safer standard.

- Deliver in a format the recipient can open and review quickly. PDF is the standard. If you use a secure sharing link, confirm the recipient can access it without creating an account.

Common Real Estate and Mortgage Pitfalls

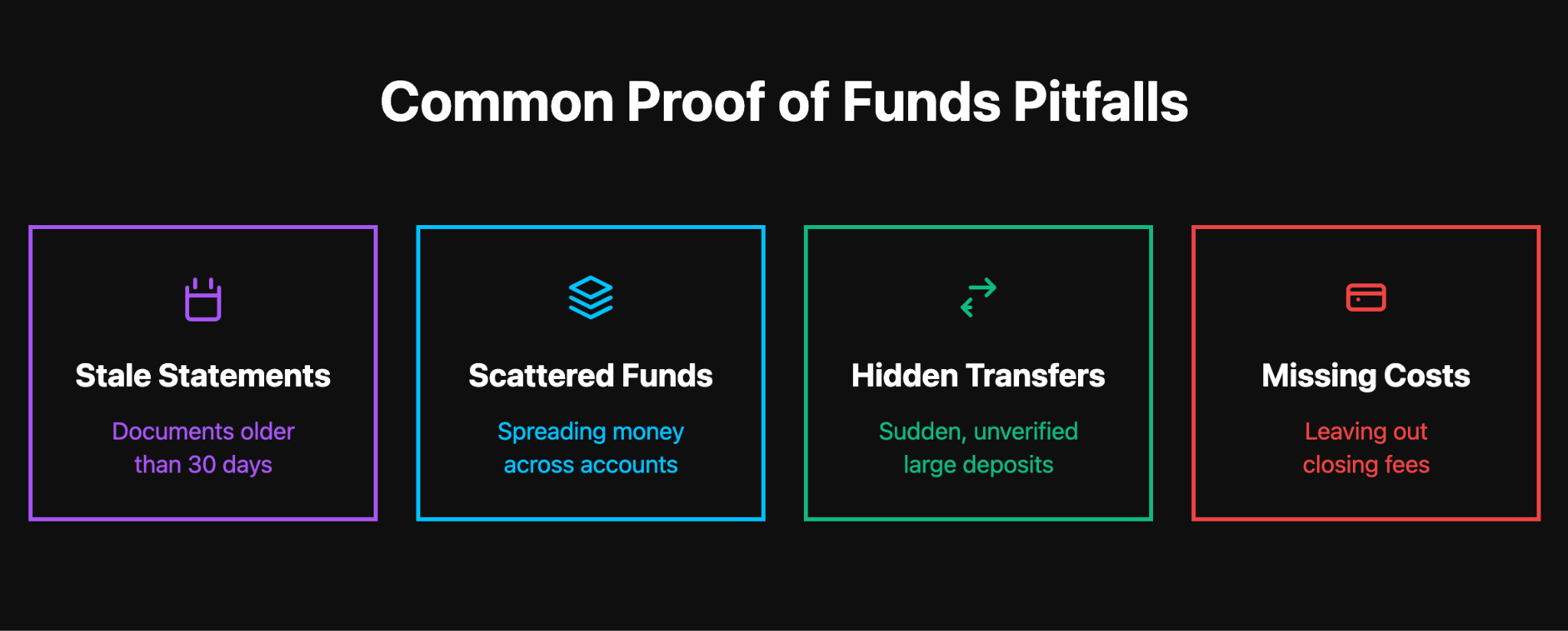

Stale statements

A bank statement from four months ago will likely be rejected. Build in time to pull fresh statements before making an offer or starting the mortgage application process.

Funds spread across too many accounts

If your down payment is distributed across eight accounts at five different banks, assembling documentation is time-consuming and easy to get wrong. Consolidating funds into fewer accounts before a transaction reduces complexity for everyone.

See our guide to organizing bank accounts for practical steps on simplifying your account structure.

Undocumented transfers

Large recent deposits or transfers between accounts trigger source-of-funds questions from lenders and issuers. For mortgage applications, lenders typically want funds seasoned in your accounts for at least 60 to 90 days. Document any recent large transfers proactively with supporting records.

Confusing reserves and down payment

Lenders verify down payment funds and post-closing reserves separately. Reserves are funds you retain after closing. Make sure your documentation covers both, not just the down payment amount.

Forgetting closing costs

Proof of funds should cover the full transaction: down payment plus estimated closing costs. Many buyers document only the purchase amount and arrive at closing short. Closing costs on a conventional mortgage typically run 2 to 5 percent of the loan amount.

For more on how funds work in mortgage contexts, see our articles on asset-based mortgages and margin loans vs mortgages.

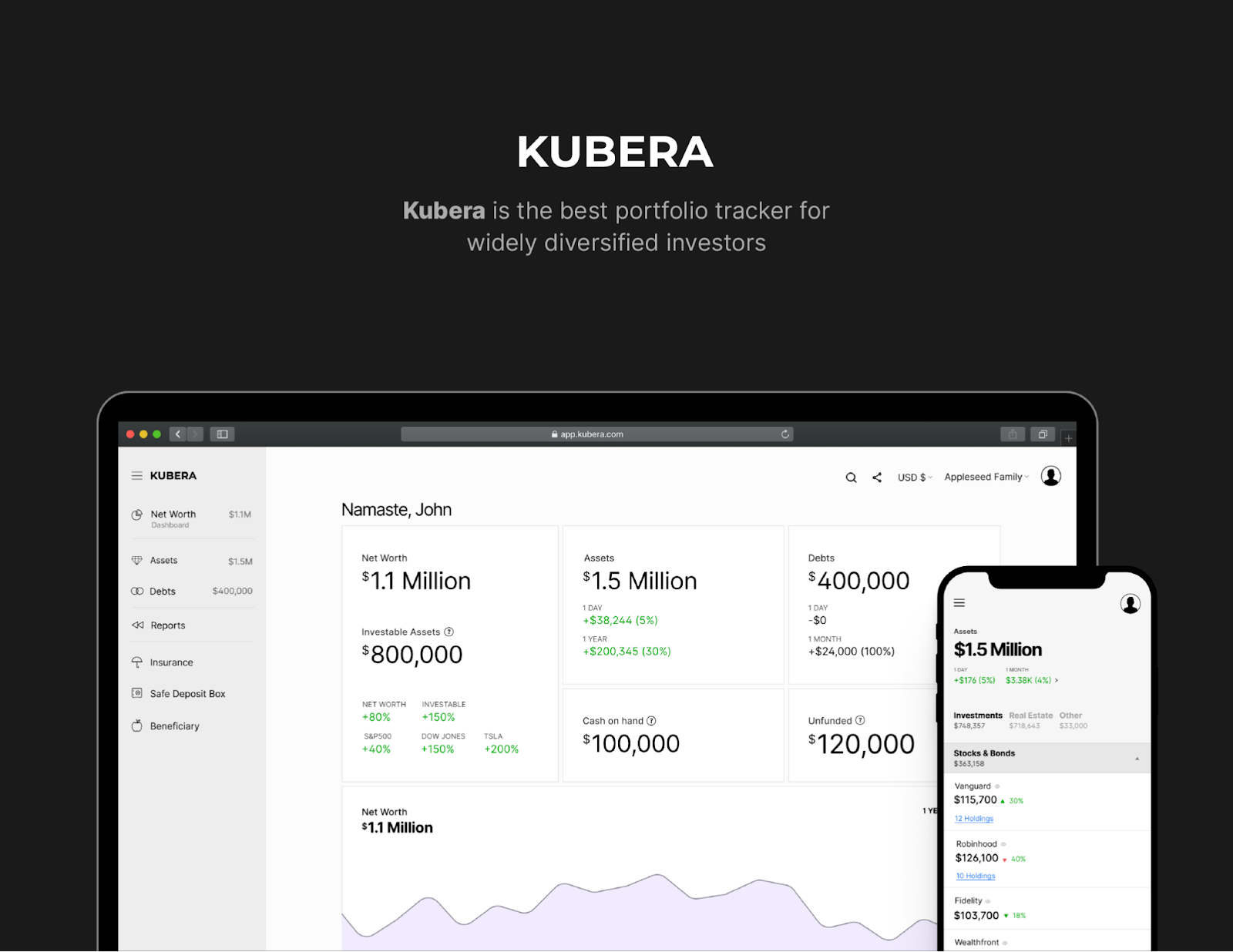

Where Kubera Fits

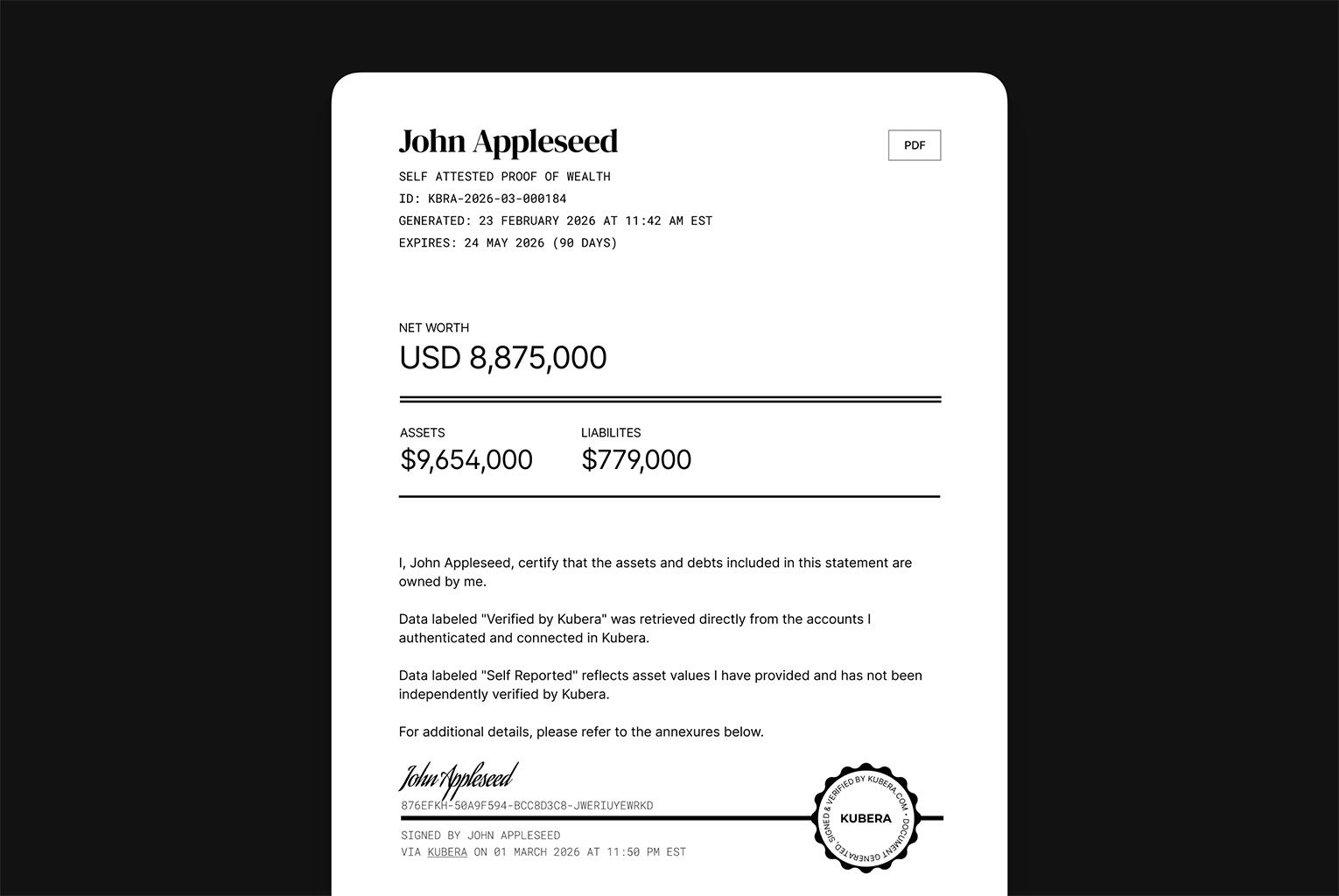

Kubera’s Proof of Wealth generates a signed, dated, shareable financial snapshot from your connected bank and brokerage accounts. For proof-of-funds contexts, this produces a clean, organized summary that recipients can review without accessing your actual accounts. You can share it as a link or download it as a PDF. Learn more at kubera.com/proof-of-wealth.

Recipients decide whether the format is sufficient for their requirements. Kubera Proof does not replace a formal bank letter where one is specifically required. But it accelerates the assembly process and provides a reviewable overview to accompany account-level statements.

For time-sensitive transactions, having a shareable snapshot ready in advance removes a common delay point. Buyers who have their documentation organized before an opportunity arises move faster when it matters.

Frequently Asked Questions

What is a proof of funds letter?

A proof of funds letter verifies that you have liquid, accessible assets available to complete a specific financial transaction. It is most commonly used for real estate offers, mortgage underwriting, bridge financing, and private investment subscriptions.

Is a bank statement enough as proof of funds?

Often yes, particularly for mortgage underwriting. A bank statement should show your name, the institution, the account number (or last four digits), the current balance, and recent transaction history. Check with the specific recipient for their requirements. Some will accept a statement; while others want a formal bank letter on official letterhead.

Can I use investments as proof of funds?

It depends on the recipient and the asset type. Liquid investments such as publicly traded stocks and money market funds are sometimes accepted. Illiquid private investments generally are not. Retirement accounts with access restrictions may qualify only at a discount. Always confirm with the recipient before relying on investment accounts.

What is the difference between proof of funds and preapproval?

Preapproval shows that a lender is willing to fund a purchase based on your credit and income. Proof of funds shows that you have the assets to cover the down payment, closing costs, and reserves. Both are often required in financed real estate transactions. They serve complementary but distinct purposes.

How recent does proof of funds need to be?

Most recipients require documentation dated within 30 to 90 days. For competitive real estate offers, 30 days is a common standard. For mortgage underwriting, 60 days is typical. Always confirm the freshness requirement with the specific recipient before submitting.

Can I use proof of funds for a private investment?

Some platforms and fund managers ask for documentation of available capital as part of the subscription or onboarding process, especially for high-minimum offerings. Requirements vary. Ask the specific platform or issuer what documentation they will accept.

What is the difference between proof of funds and proof of wealth?

Proof of funds focuses on liquid assets available for a specific, current transaction. A proof of wealth letter or net worth statement is a broader financial picture covering all assets, debts, and total net worth. Proof of wealth is used for accredited investor verification, private banking, and similar contexts where a complete financial picture is needed, not just transaction-ready cash.

Get a signed, shareable snapshot of your wealth

Kubera connects your bank accounts, brokerage accounts, and other assets in one place. Generate a signed, dated, shareable proof package to share with lenders, sellers, or fund managers without sending raw account credentials.

Sign up now for a 14 day trial to get started!

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Proof-of-funds documentation requirements vary by recipient, transaction type, and jurisdiction. Consult a qualified professional for guidance on your specific situation.