A high-net-worth divorce is rarely defined by a single dollar threshold. It is defined by the shape of the balance sheet. When a household holds operating businesses, equity compensation, illiquid alternative investments, trust interests, multiple entities, or assets that move across borders, the divorce process becomes a financial engineering problem as much as a legal one.

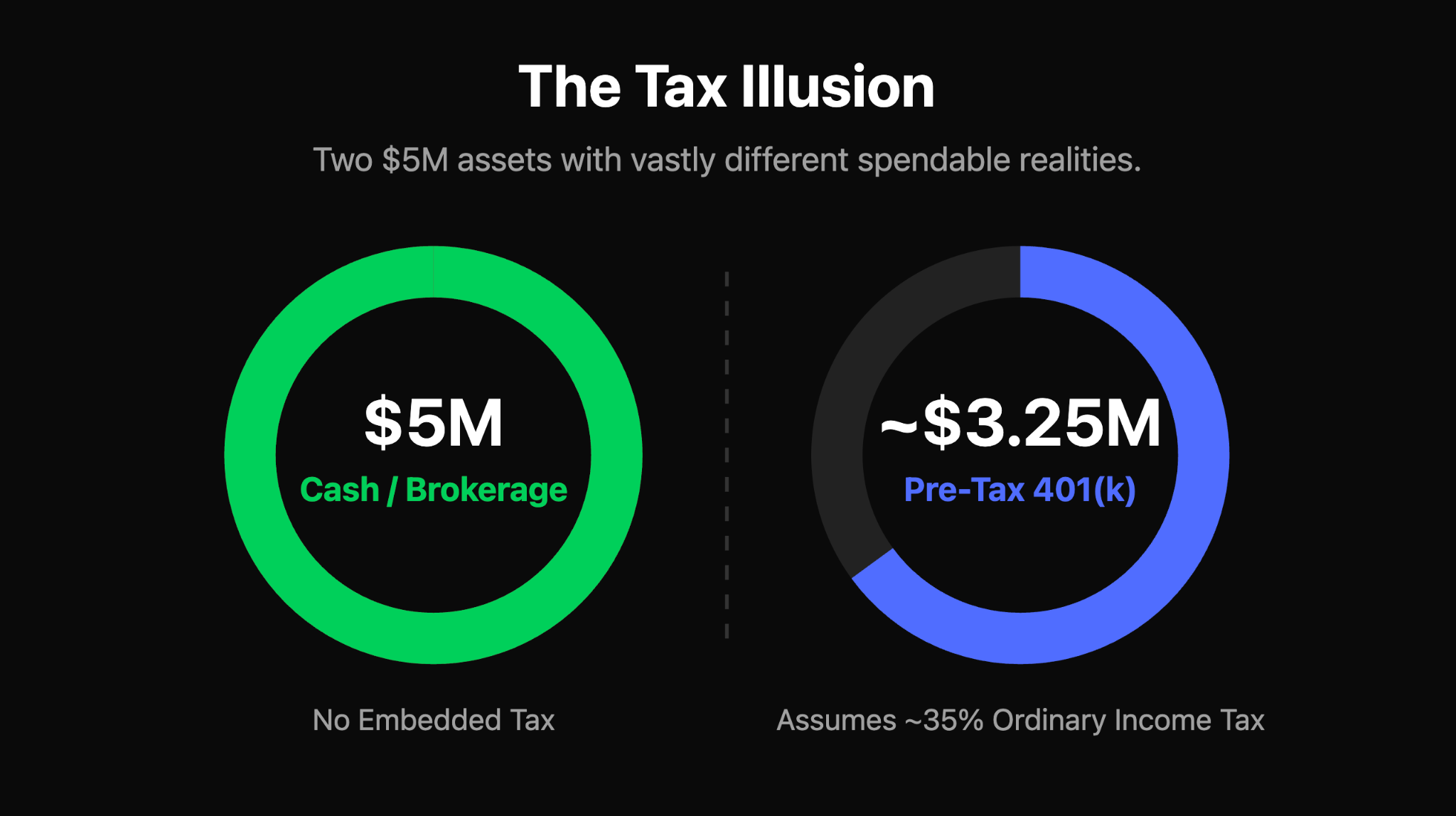

The complexity does not come from wealth alone. It comes from valuation disputes, ownership structures, liquidity mismatches, and tax asymmetry that turn equal-looking settlements into unequal outcomes. A $5 million brokerage account and $5 million in pre-tax retirement assets are not economically equivalent. The legal division can look even, while the economic result is not.

The right question in a high-net-worth divorce is not just how assets get divided. It is how they get identified, valued, taxed, and managed once the marriage ends. The families who come through this process best are usually not the ones with the most aggressive lawyers. They are the ones who get organized early, understand what they own, build the right team, and stop making impulsive financial moves while the legal process runs its course.

What Makes a High-Net-Worth Divorce Different

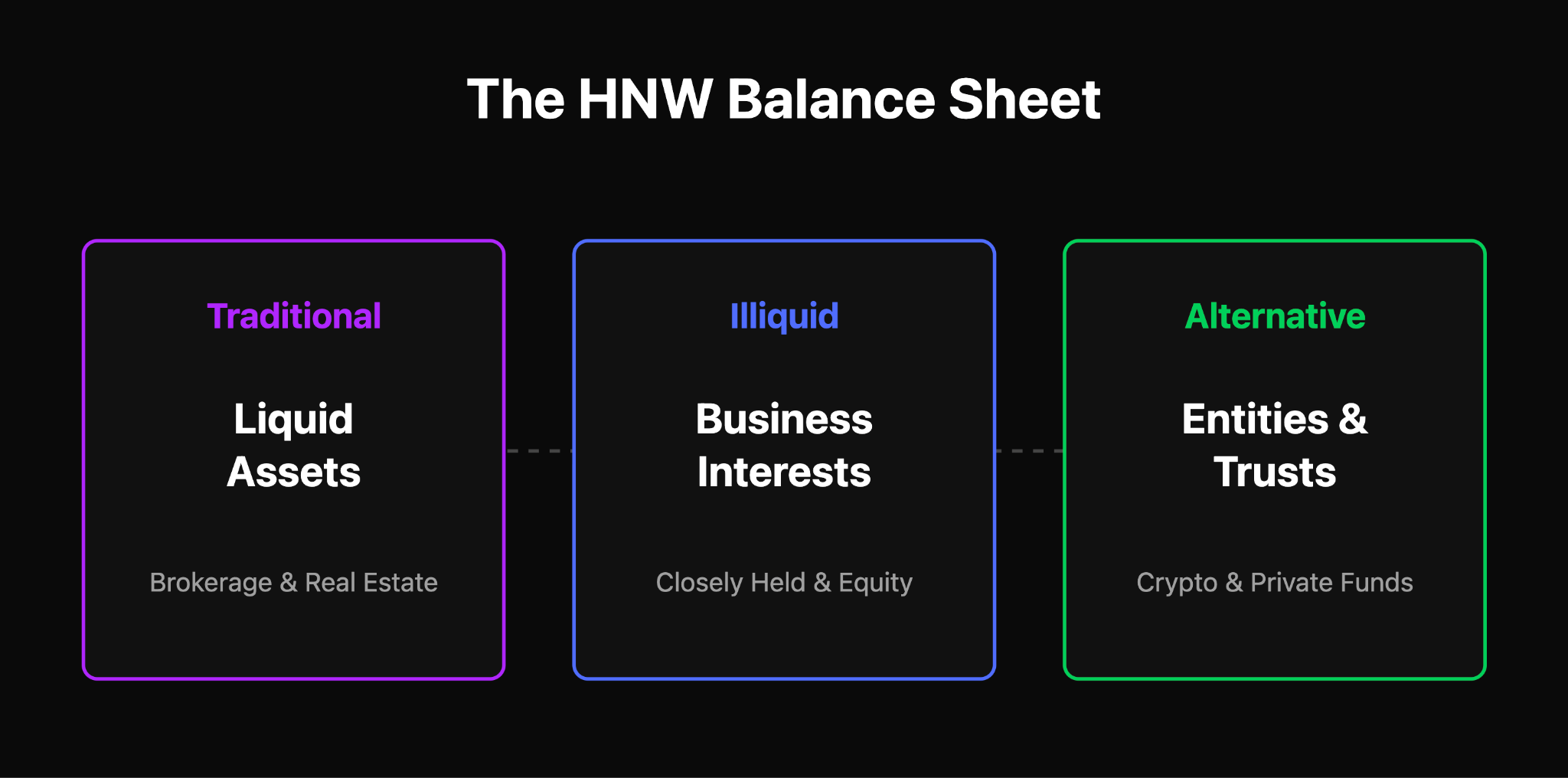

Most divorces center on a home, retirement accounts, and a checking balance. A high asset divorce often involves all of those plus operating companies, founder stock, deferred compensation, partnership interests, real estate held in LLCs, trust beneficiary positions, crypto wallets, art, aircraft, and sometimes assets in two or three jurisdictions.

A few features come up again and again.

- Valuation is contested, not given: A public stock has a price. A minority interest in a closely held company does not. Two reputable valuators can look at the same business and arrive at numbers that differ by 30 percent or more, each defensible.

- Liquidity is uneven: Wealth that lives inside an operating business, a private fund, or a tied-up real estate position cannot easily be split in half on the courthouse steps. Settlements have to be structured around lock-ups, capital calls, redemption windows, and tax timing.

- Timelines stretch: When valuation experts and forensic accountants get involved, six to eighteen months is common. Two years or more is not unusual when a business or trust is contested.

- Tax asymmetry is everywhere: Pre-tax dollars are not the same as after-tax dollars. Embedded gains in concentrated stock are often invisible in a settlement spreadsheet that only shows market value.

- Privacy and cross-border exposure add further friction: foreign trusts, non-U.S. real estate, and assets held across jurisdictions raise reporting and authority questions that domestic divorces do not.

- Reputational and confidentiality stakes are also higher: Public-company executives, founders with active boards, locally prominent business owners, and family-office households often have specific concerns about what ends up in court filings, what local press might cover, and what employees, investors, or extended family will see. That changes how you think about venue, timing, settlement structure, and whether mediation or collaborative divorce makes sense.

The defining factor is complexity, not zeros. A $4 million estate with a closely held business and an active trust can be harder to divide than a $40 million portfolio of public securities.

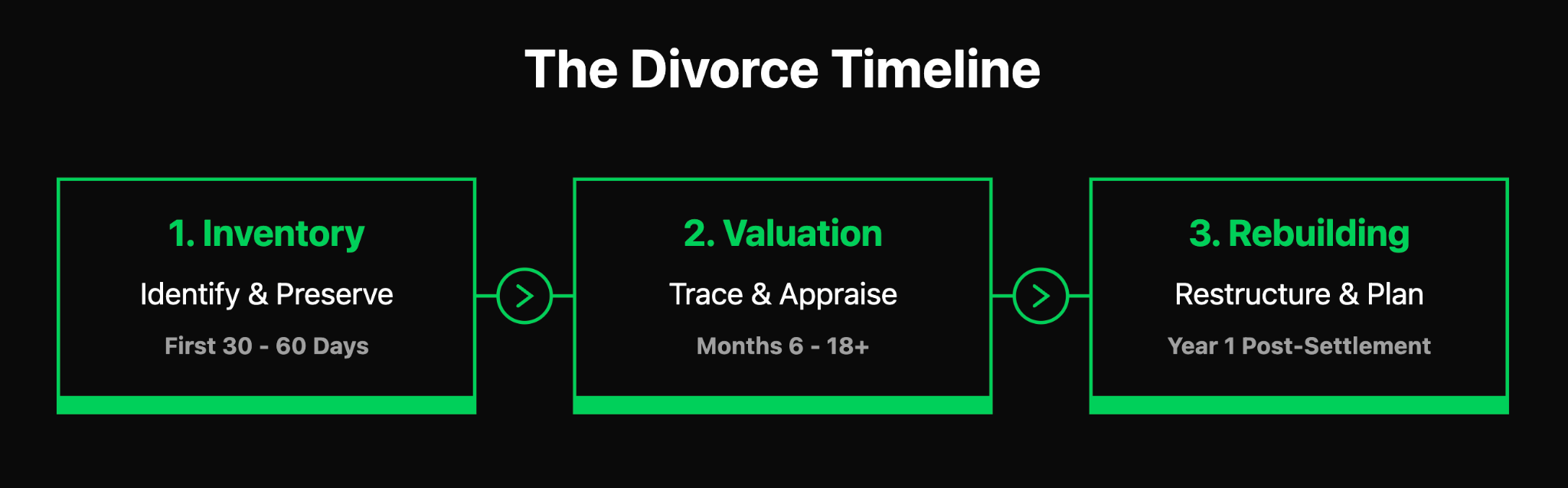

What to Do First in a High Asset Divorce

The early window matters more than most people realize. Decisions made in the first 30 to 60 days often determine how much leverage and clarity you carry into negotiation.

- Build a financial inventory before you build a legal strategy: You cannot protect what you have not identified. The goal is a single picture of every account, entity, asset, and liability, with current statements and supporting documents.

- Preserve records: Pull recent statements for every bank, brokerage, retirement, and credit account. Save tax returns from at least the last five years, plus K-1s, grant agreements, trust documents, operating agreements, and insurance policies. Store them somewhere only you can access.

- Stop making large or unusual financial moves: Many states impose automatic temporary restraining orders the moment a petition is filed. Even where they do not, large transfers, asset retitling, gifts, or unusual spending will almost certainly surface in discovery and damage your credibility.

- Separate emotional decisions from asset decisions: The instinct to hand over the house to end the conflict, or to fight for an asset out of pride, rarely produces a good outcome. Sound financial decisions are made on numbers and time horizons, not on the temperature of the conversation.

- Identify your team early: A divorce attorney is necessary, but rarely sufficient in a high-net-worth divorce. And learn at a high level what is likely separate versus marital property in your jurisdiction before you sit down with counsel. Where children or significant income gaps are involved, build a preliminary view of what child support and spousal support obligations might look like under your jurisdiction's guidelines, so settlement modeling reflects realistic cash flow on both sides.

Gather These First

A short financial inventory worth working through in the first weeks:

- Recent bank and brokerage statements, including custodial and joint accounts

- Retirement plan statements: 401(k), 403(b), pension, IRA, Roth IRA

- Federal and state tax returns for at least the past five years, with all schedules and K-1s

- Pay stubs, W-2s, and 1099s

- Grant deeds, mortgage statements, and property tax records for all real estate

- Cap tables, equity grant documents, RSU and stock option statements, vesting schedules

- Trust documents, both as grantor and as beneficiary

- Operating agreements, partnership agreements, and shareholder agreements for any entities

- Insurance policies (life, disability, umbrella, long-term care) with cash value statements where applicable

- Loan statements for any debt, including intra-family loans

- Crypto exchange statements and wallet addresses

- Records of significant gifts, inheritances, and pre-marital assets

- Estate planning documents, including any prenuptial or postnuptial agreements

If something cannot be identified, traced, or valued, it becomes much harder to protect or divide fairly.

Do Not Do These in the First Phase

A short list of moves that almost always backfire, regardless of intent:

- Do not move money between accounts without advice from counsel

- Do not retitle assets, change beneficiaries, or transfer ownership of anything

- Do not delete emails, statements, text messages, or shared cloud files

- Do not make unusual gifts, loans, or large withdrawals

- Do not assume an asset is separate property just because it is titled only in your name

These are the moves that show up in discovery, draw court sanctions, and cost more in credibility than they ever save in dollars.

Building Your Professional Team

In a high asset divorce, the team often matters more than any single advisor.

- A divorce attorney, ideally a family law specialist with experience in complex estates, manages process, court strategy, and negotiation. They do not value your business or build your post-divorce financial plan.

- A forensic accountant traces cash flow, reconstructs lifestyle, and finds what spreadsheets miss. They are especially important when one spouse controlled the household finances or when there is any concern about unreported income.

- A credentialed business or asset valuator handles closely held interests, complex real estate, or significant collectibles. Methodology, assumptions, and valuation date can swing the number meaningfully.

- A Certified Divorce Financial Analyst (CDFA) looks at proposed settlements through a long-term financial planning lens, modeling what a settlement actually means in five, ten, and twenty years after taxes, inflation, and cash flow needs.

- A tax advisor flags the after-tax reality of any proposed division: basis differences, embedded gains, retirement account treatment, entity-level consequences. An estate planner revises wills, trusts, beneficiary designations, and powers of attorney, ideally in parallel with the divorce rather than after.

When one spouse has historically controlled the finances, this team becomes even more important. The non-controlling spouse usually needs help reconstructing the full picture before any negotiation can be productive.

Complex Assets That Require Special Valuation

This is where divorce financial planning earns its keep.

1. Operating businesses

Closely held companies are often the largest single asset on the balance sheet. Valuation typically blends the income approach (discounted cash flow), market approach (comparable transactions), and asset approach. Treatment of personal versus enterprise goodwill, marketability discounts, minority interest discounts, and normalization of owner compensation can swing the number significantly. State law varies on whether personal goodwill is divisible at all.

2. Stock options and RSUs

Vested grants are usually easier. Unvested grants are where the disputes happen. Courts in many jurisdictions use formula-based approaches, often called time rules or coverture fractions, to allocate the marital portion of unvested awards based on the time worked during the marriage relative to the total time from grant to vesting. California cases often reference the Hug or Nelson formulas, and other states use their own variants or related approaches depending on the facts. The treatment depends on whether the grant was for past services or future performance, the type of equity compensation, and the specific terms of the grant. Because unvested equity cannot generally be transferred, settlements often use deferred distribution (the employee spouse holds the shares until vesting and remits the non-employee spouse's portion net of taxes) or offset (the employee spouse keeps the equity and trades other assets in exchange).

3. Private equity, venture, and hedge fund interests

LP interests usually carry capital commitments, lockups, and unfunded obligations. Carried interest is complicated, because its value depends on future fund performance and may have minimal current market value despite significant upside. A neutral valuation expert with experience in private fund interests is often necessary.

4. Crypto and digital assets

Bitcoin in a hot wallet is one thing. Staked tokens, DeFi positions, NFTs, locked vesting tokens, and self-custodied assets in cold storage are another. Forensic firms now use blockchain analytics to trace flows. Volatility itself becomes a settlement design problem: do you value at petition date, separation date, or settlement date?

5. Real estate, art, and collectibles

Each has its own valuation considerations. Cap rates and comparable sales for real estate. Specialist appraisals for art, jewelry, and collectibles. Insurance schedules typically overstate liquidation value. Real estate held inside LLCs adds another layer.

6. Trust interests

Whether a trust interest is divisible depends heavily on state law, the trust language, the type of interest (vested, contingent, discretionary), and how distributions have historically been handled. A discretionary beneficiary interest in a properly structured irrevocable trust is often, but not always, treated as separate property. Tracing of distributions during the marriage matters.

7. Retirement accounts versus taxable accounts

This is structural rather than asset-specific, but it deserves emphasis. A pre-tax retirement account dollar is not equal to a taxable brokerage dollar. The difference can be 25 to 40 percent depending on the recipient's marginal rate, and it usually shows up only when you build the after-tax model.

One issue cuts across all of these: the valuation date. For volatile or illiquid assets, whether you value at the date of separation, the date of filing, the date of trial, or some negotiated date can move the number significantly. State law and judicial discretion shape the answer, and the choice is often more consequential than the methodology itself.

Separate Property, Marital Property, and Commingling

The line between separate and marital property can look straightforward in theory and become genuinely difficult in practice.

In broad terms, separate property typically includes assets owned before the marriage, gifts and inheritances received individually during the marriage, and certain assets covered by a prenuptial or postnuptial agreement. Marital property generally includes assets and earnings acquired during the marriage. The treatment of appreciation on separate property, and of income generated by separate property, varies by state. Community property states and equitable distribution states approach this differently, and within equitable distribution states the rules and judicial discretion vary.

Commingling is where good separate-property arguments often fall apart. Inherited cash deposited into a joint account and used for household expenses can lose its separate character. A pre-marital brokerage account that received post-marriage contributions becomes a tracing exercise. A house owned before the marriage that was later refinanced, retitled, or substantially improved with marital funds may have a marital component.

Title alone is not always decisive. A house held only in one spouse's name is not automatically separate property if marital funds went into it. An account in a joint name is not automatically marital if the funds can be traced to clearly separate sources.

Records make the difference. The strongest separate-property claims tend to be supported by clean documentation: account statements at the date of marriage, inheritance documentation, gift letters, deed history, and a clear paper trail showing that separate funds were never mixed with marital funds.

This is a place where general rules are limited and specifics matter. State law, title structure, tracing records, and the language of any trust or agreement all affect the outcome.

Hidden Assets: How They Are Found and Why Hiding Them Backfires

In high-net-worth households, one spouse often has substantially more visibility into the finances than the other. That asymmetry creates room for concealment, both real and suspected. In many cases, what looks like concealment at first is partly a documentation problem, a control problem, or a complexity problem. The distinction usually only gets clearer once records are complete.

Common patterns that come up in forensic work include income deferred or routed through closely held entities, personal expenses run through a business, "loans" to friends or family that are never repaid, gifts to relatives with informal repayment understandings, crypto holdings in self-custodied wallets that never appear on exchange statements, foreign accounts and offshore entities, and bonuses or carry distributions delayed until after settlement.

Forensic accountants approach this through document review, lifestyle analysis (does reported income support actual household spending), tax return analysis, transaction review, and cross-referencing with public records. Blockchain analytics tools have made crypto concealment significantly harder than it was even five years ago.

Hiding assets carries real costs beyond getting caught. Courts in most jurisdictions can sanction the offending spouse with adverse inferences, fee shifting, and in serious cases an unequal division of the discovered asset, sometimes awarding the entire concealed asset to the other spouse. Perjury and contempt are also possibilities. The reputational cost in a small professional or industry community can outlast the financial cost. The smarter posture is usually full disclosure paired with strong valuation work and a credible separate-property case where one exists.

Tax Traps in Divorce Asset Division

Tax is often the difference between a settlement that looks fair on paper and one that is fair in practice. In divorce asset division, a handful of issues come up repeatedly.

1. Section 1041 and transfers between spouses

Under Internal Revenue Code Section 1041, no gain or loss is generally recognized on transfers of property between spouses or between former spouses if the transfer is incident to the divorce, meaning it occurs within one year of the divorce or is otherwise related to the cessation of the marriage. The receiving spouse takes the transferor's basis. This is helpful, but it also means that built-in gains transfer with the asset.

2. Embedded gains and basis differences

A taxable brokerage account showing $5 million in market value with $1 million in cost basis is not economically equal to $5 million in cash. If the receiving spouse needs to liquidate, the embedded gain becomes their tax bill. Two assets at the same headline value can produce very different after-tax dollars.

3. Pre-tax retirement accounts

Traditional 401(k) and IRA balances are pre-tax. Every dollar withdrawn is taxed at ordinary income rates. A Roth account of the same balance is fundamentally different.

4. QDROs

A qualified domestic relations order (QRDO) is the legal instrument used to divide most ERISA-governed retirement plans, including 401(k)s and traditional pensions, between divorcing spouses. Per the IRS and the Department of Labor, a properly structured QDRO allows the alternate payee (typically the non-employee spouse) to receive their share without triggering the 10 percent early-withdrawal penalty. IRAs do not require a QDRO; they are divided by a transfer incident to divorce, ideally as a direct trustee-to-trustee transfer to avoid distribution treatment. QDRO drafting matters: outstanding plan loans, gain-loss allocations, and the treatment of post-decree appreciation should all be specified explicitly.

5. Alimony post-2018

For divorce or separation agreements executed after December 31, 2018, the IRS treats alimony as neither deductible by the payer nor includible in the recipient's gross income. This was a significant change from the prior regime and often shifts the practical economics of support negotiations. Pre-2019 agreements generally remain under the old rules unless modified to opt into the new treatment.

6. Capital gains on the marital home

Section 121 allows up to $250,000 of gain exclusion for a single filer, or $500,000 for joint filers, on the sale of a primary residence, subject to ownership and use tests. Timing of sale relative to the divorce, and the rules for former spouses, matters.

7. Business and entity-level consequences

A redemption of a spouse's interest by the company itself, rather than a direct interspousal transfer, can create taxable income for the redeemed spouse. Buyouts of operating partners often need to be structured carefully.

8. State income tax differences

The economic value of an asset can change if the recipient lives in a different state from the transferor, especially when capital gains, retirement income, or trust income is involved.

Note: These examples are simplified and exclude state-specific rules, timing differences, transaction costs, and the interaction with other items on the return. They are intended to show directional after-tax differences, not precise outcomes for any specific household.

The point is not to chase a particular number. The point is that two settlement piles described as $5 million each can be worth materially different amounts in real, spendable dollars. Modeling the after-tax economics is one of the most valuable things a CDFA or tax advisor does in a high-asset divorce.

How to Protect Assets in Divorce, Lawfully and Effectively

The phrase "protect assets in divorce" gets misused. It does not mean hiding, retitling, or moving marital property to keep it away from a spouse or the court. Those moves typically violate automatic standing orders, expose the moving spouse to sanctions, and undermine credibility on every other issue. They also rarely work.

Protecting wealth in a high-net-worth divorce, in the lawful and effective sense, looks like this.

- Document everything: account statements at the date of marriage, inheritance and gift records, the provenance of pre-marital assets, the history of any closely held business including capitalization and ownership changes.

- Build and maintain a clean financial inventory: a current, complete view of the balance sheet is the single most useful tool in negotiation.

- Understand any prenup or postnup carefully: A well-drafted prenuptial or postnuptial agreement can shape division of assets and spousal support in ways the default rules do not. Enforceability depends on disclosure at signing, lack of duress, and state-specific requirements.

- Respect automatic temporary orders: Many jurisdictions impose automatic restraining orders the moment a divorce petition is filed, prohibiting unusual transfers, asset retitling, beneficiary changes, and large gifts. Read the order carefully and behave accordingly.

- Do not dissipate marital assets: lavish spending, gambling losses, and large gifts during the divorce process can be reconstructed by a forensic accountant and credited back against the dissipating spouse's share.

- Consider mediation or collaborative divorce where appropriate: When both spouses have a genuine interest in privacy, a faster resolution, or preserving an ongoing business relationship, these paths can produce better outcomes than litigation. They are not right for every case, particularly where there is a serious power imbalance or concealment risk.

The strongest asset protection in a divorce is almost always informational: knowing what you own, having the records to prove it, and having a team that can model the consequences.

Rebuilding Your Financial Life After a High-Net-Worth Divorce

Settlement is not the finish line. The financial reorganization that follows often takes longer than the divorce itself.

Cash flow needs to be rebuilt around a single household. Many affluent households spend at a level that quietly assumes both incomes and pooled wealth, and a new budget grounded in the new reality is the foundation. Where applicable, that budget needs to reflect both inflows and outflows from child support and spousal support, the tax treatment of each, and any step-downs or termination dates built into the agreement. Investment policy needs to be rewritten around one set of goals, time horizons, and risk tolerances, with attention to concentrated stock, embedded gains, and any over-allocations that survived the division.

Estate planning updates are where most people drop the ball. Wills, trusts, powers of attorney, and health care directives all need review, as do trustees and successor trustees who may be associated with the former spouse. Beneficiary designations are the single most commonly missed step. Retirement accounts, life insurance, and transfer-on-death accounts pass by beneficiary designation regardless of what a will says.

Insurance often needs to be restructured. A spouse who relied on the other's employer-sponsored health plan needs a new plan. Existing life insurance may need to be retained, replaced, or repurposed (sometimes as security for support obligations). Title and ownership on real estate, vehicles, and entities need to reflect the settlement.

The year of divorce, and the year after, often involve unusual tax events: asset sales, basis adjustments, support payments, and changing filing status. A coordinated tax plan avoids surprises.

This phase is the one most affected by emotional fatigue. The instinct after a long settlement is to stop thinking about money for a while. That instinct is understandable and expensive. The first 12 months after settlement are often when the most leverage exists to set the next decade up correctly.

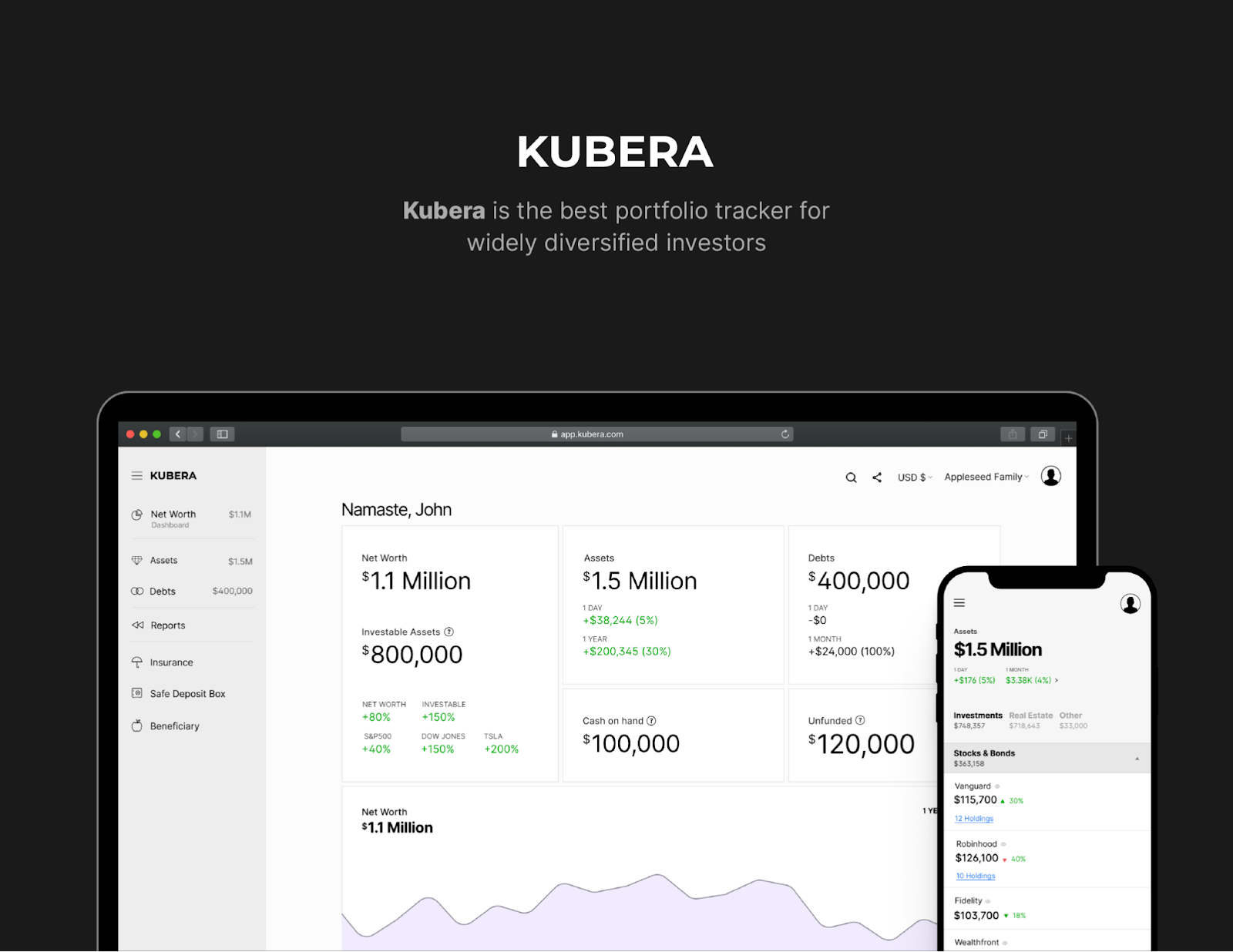

The Operational Challenge of Seeing the Full Picture

A specific problem keeps showing up in high-net-worth divorces: nobody has a single view of the full balance sheet.

Bank accounts at three institutions. Brokerage at two more. Retirement accounts at the current and former employers. A trust statement that arrives quarterly by mail. Crypto across two exchanges and a hardware wallet. Real estate held across several LLCs. Private fund interests reporting NAV once a quarter on K-1s. Operating company financials handled by a CFO who reports to one spouse.

Advisors usually see only their slice. The attorney has the case file. The accountant has the tax returns. The CDFA has the assets they were told about. There is rarely a clean, current, single-page view of the entire household balance sheet, with documents attached and everything reconciled. That gap costs money: decisions get made on partial information, and professional time gets consumed reconstructing the picture every time a question comes up, often at the worst possible moments.

When Technology Helps

Spreadsheets and scattered PDFs work until they do not. Once the balance sheet involves multiple entities, illiquid assets, crypto, real estate, and documents that need to live somewhere durable, it usually makes sense to centralize.

A platform like Kubera is built for exactly this kind of household. It tracks bank and brokerage accounts, retirement accounts, real estate, alternative investments, crypto holdings, and collectibles in one place, alongside the documents that support them.

For a divorce process, two features tend to matter most: consolidation into a single view, and read-only sharing with a spouse, attorney, accountant, or CDFA, so that the same number is in front of everyone working on the case. It does not replace the legal or accounting work. It does make the operational layer of a high-net-worth divorce much less painful.

To maintain a comprehensive view of the full balance sheet, consider using Kubera to centralize your accounts, entities, and supporting documents in one place.

Frequently Asked Questions

What is considered a high-net-worth divorce?

In practice, a high-net-worth divorce is usually defined less by a single dollar threshold and more by complexity. When a divorce involves operating businesses, equity compensation, trusts, or significant illiquid holdings, it becomes a high-net-worth divorce in the way that matters financially. Practitioners still use rough thresholds, often around $1 million in investable assets, with ultra-high-net-worth starting higher depending on the source.

Is inherited money subject to division in divorce?

Generally, inheritances received by one spouse during the marriage are treated as separate property in most jurisdictions. The protection erodes when inherited funds are commingled with marital assets, deposited into joint accounts, or used to acquire jointly titled property. State law varies, and tracing records often determine the outcome.

How are stock options or RSUs divided in divorce?

Vested grants made during the marriage are typically divisible. Unvested grants are usually allocated using a time rule or coverture fraction, with the marital share based on the period between the grant date and the relevant cutoff (often the date of separation or filing) relative to the full vesting period. California cases often reference the Hug or Nelson formulas, and other states use their own variants. The intent of the grant, past services or future performance, is often a key fact.

Are retirement accounts split 50/50?

Not automatically. They are typically divided based on the rules of the jurisdiction (community property or equitable distribution) and the marital portion of the account. A QDRO is required to divide most ERISA-governed plans without triggering early withdrawal penalties. IRAs are divided by a transfer incident to divorce. What matters more than the headline split is the after-tax value each spouse actually receives.

What is a forensic accountant in divorce?

A forensic accountant traces cash flow, reconstructs lifestyle, identifies unreported income, evaluates closely held business records, and helps locate or value assets that might otherwise be hidden or misrepresented. They are particularly valuable when one spouse controlled the household finances or where a business is involved.

How do you protect separate property in divorce?

By documenting it. The strongest separate-property claims are supported by clear records: account statements at the date of marriage, inheritance and gift documentation, deed history, and a paper trail showing that separate funds were not commingled with marital funds. Title alone is rarely sufficient. A prenuptial or postnuptial agreement can provide additional protection.

What happens to a business in divorce?

The business is valued, and the marital portion of its value is divided. Common outcomes include one spouse buying out the other (often through cash, notes, and offsetting asset), continued co-ownership with clear governance terms (less common, often awkward), or sale of the business. Valuation methodology, treatment of personal goodwill, and discounts for marketability or minority interest all matter.

Are hidden assets common in high asset divorce?

Concerns are common. Actual concealment is less common than people fear, but it does happen, especially in households where one spouse controls the finances or where there are closely held entities and crypto holdings. Forensic accounting and modern tracing tools have made concealment significantly harder. The risk of getting caught, and the penalties when it happens, generally make full disclosure the better strategy.

Conclusion

A high-net-worth divorce is a legal process layered on top of a financial-planning problem. Courts divide rights and obligations. The harder work is understanding what the balance sheet is actually worth, how the tax burdens travel, and what life looks like once the household is no longer one unit.

The families who do this well are usually not the ones with the most aggressive courtroom strategy. They are the ones who get organized early, build the right team, treat valuation and tax with the seriousness they deserve, and stop making impulsive moves while the process runs. None of that removes the difficulty of the situation. It does shift the odds in favor of an outcome you can live with.

Disclaimer: This article is general information, not legal, tax, or investment advice. Outcomes in any specific divorce depend on state law, court discretion, the structure of the marital and separate estates, plan and trust documents, valuation assumptions, and the terms of any settlement.