A golden visa is, in almost every case, a residency-by-investment program: you make a qualifying investment or contribution and receive the legal right to reside in a country, and often to live and work there. It is not a passport. A few programs offer a path to citizenship after years of residency and integration requirements, but the visa itself grants residence, not nationality, and it is not the same as tax residency, which depends on where you actually live. This guide covers what golden visas are, which golden visa countries remain open in 2026, how investment requirements and routes compare, the tax implications for US and non-US investors, and how a second residency reshapes a global portfolio.

Investors pursue residency by investment for reasons that have little to do with status_ and instead focus on elements like_ geographic and political diversification, a credible relocation option for the family, healthcare and schooling access, Schengen Area mobility, tax optionality exercised only if someone actually relocates, and long-term optionality for children. The expensive mistakes come from conflating residence, citizenship, and tax status, often choosing a program for the wrong reason and finding that the cheapest entry point carried the highest total cost.

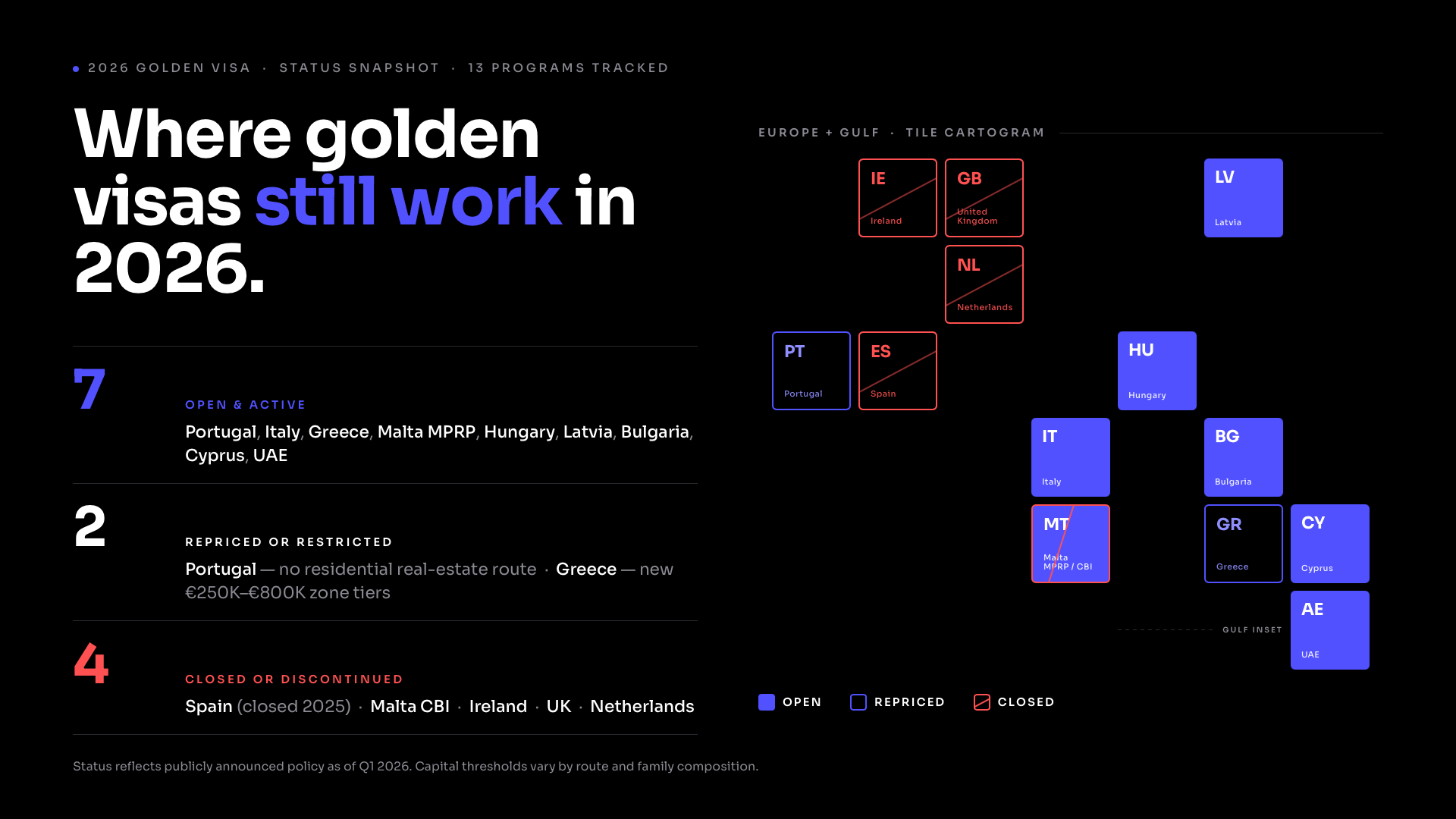

The 2026 landscape is not the one older articles describe. Spain closed its program in 2025, Malta lost its citizenship-by-investment route to a European Court of Justice ruling, Portugal ended residential real estate as a qualifying route in 2023 and spent 2025 and 2026 fighting over the citizenship timeline, and Greece repriced its real estate tiers. The direction across Europe is away from passive property and toward funds, business, job creation, and stricter due diligence,which is exactly why current verification matters far more than it used to.

What is a golden visa?

The term has no legal definition; no government writes "golden visa" into its statutes. Portugal calls its program the ARI, Greece issues a residence permit for investors, and Hungary created the Guest Investor Residence Permit. The shorthand survives because the idea is consistent: a residence permit obtained through a financial investment, where the holder is usually not required to live in the country full-time or become a tax resident to keep the status.

You make a qualifying investment, such as a fund subscription, property purchase, government bond, bank deposit, business stake, job creation infrastructure, or a donation, and receive renewable legal residence. Many programs include family, while some attach a long, conditional path to citizenship.

How it differs from citizenship by investment

Citizenship by investment grants a passport, usually quickly, for a larger and often non-refundable contribution; the Caribbean programs are the best-known examples. A golden visa gives you the right to live somewhere, not nationality. Conflating the two is the single most common error in this field, and marketing material frequently encourages it. If a page calls a residency program a fast track to a passport, read the fine print, because the legal reality is slower and more conditional.

How it differs from tax residency

Tax residency is decided by facts and local law, not your permit. Most countries treat you as a resident if you spend enough days there, commonly a 183-day threshold in a calendar year, or if your center of vital interests, permanent home, or habitual abode sits there. You can hold a golden visa and remain a tax resident elsewhere because you never moved, and you can become a tax resident somewhere you hold no special visa at all. The permit and the tax status are separate questions.

Golden visa vs citizenship by investment vs tax residency

These three sit at the heart of nearly every misunderstanding, so it is worth laying them side by side.

A working taxonomy of the programs

Search results systematically lump very different programs together. A retirement visa, a digital nomad permit, and a residency-by-investment program are not interchangeable, and choosing the wrong category is just as costly as selecting the wrong country.

In short: a golden visa is the precise tool to execute when the core objective is a durable residence right and sovereignty optionality, with passive capital deployed as the clear price of entry. If the absolute goal is purely a passport, the track is citizenship by investment. If the goal is a structurally minimized tax bill, the asset is a tax-residency regime, and it only delivers results if you physically relocate your life.

The best golden visa programs still open in 2026

"Best" is a function of fit, not price, so treat this as a current map rather than a ranking. Figures reflect program rules reported in early 2026 and should be confirmed against official sources before you commit, because several programs are mid-reform. Best-fit notes appear in the status table that follows.

Portugal 🇵🇹

Portugal is the most scrutinized program in the market and one of the most resilient. The residential real estate route ended in October 2023. What survived is mostly capital and enterprise: roughly EUR 500,000 into qualifying investment funds (now the dominant route), EUR 250,000 for cultural or artistic support, EUR 500,000 for scientific research, or business creation with at least ten jobs. Physical presence is light, an average of about seven days a year, with permanent residency at year five. The open question is citizenship timing: it had been five years, but a late-2025 reform to extend naturalization toward ten years for most non-EU applicants was partly struck down by the Constitutional Court and was still contested into 2026, so the road to a passport is longer and less certain. Processing backlogs have also been severe. If you relocate, the old NHR regime is closed to new entrants; its narrower replacement, IFICI, offers a 20% flat rate on qualifying professional income and some foreign-income exemptions.

Greece 🇬🇷

Greece repriced its framework via zone-based real estate bands in September 2024: roughly EUR 800,000 for high-demand areas like Athens, Thessaloniki, Mykonos, Santorini, and larger islands; EUR 400,000 for remaining regions (both avenues strictly requiring a single property of at least 120 square meters); and EUR 250,000 for localized conversions of commercial property to residential use or the restoration of listed heritage buildings. Non-real-estate routes include approximately EUR 500,000 in sovereign government bonds or a local bank deposit, and EUR 800,000 in equities or corporate bonds. There is no minimum physical stay, but citizenship eligibility generally triggers only after seven years of continuous tax residence paired with a formal language examination, making the passport a serious relocation commitment. Furthermore, short-term rental of these qualifying properties is now legally prohibited, a critical hurdle for anyone assuming the underlying asset would automatically produce immediate yield.

Italy 🇮🇹

Italy’s Investor Visa offers four targeted investment routes: roughly EUR 250,000 into an innovative startup venture, EUR 500,000 into an established corporate entity, EUR 2 million in government bonds, or a EUR 1 million philanthropic donation. Administrative processing is notably fast, often clearing within three to four months. While there is no explicit calendar stay requirement, applicants must show a genuine intent to reside, and citizenship follows the standard ten-year path. Separately, Italy has aggressively leaned into attracting ultra-high-net-worth individuals through its flat-tax regime: for those transferring their primary tax residence from 2026, the lump-sum tax on all foreign-source income is EUR 300,000 a year (up from EUR 200,000), plus EUR 50,000 per family member, guaranteed for up to 15 years. This applies only if you actually become a tax resident under Italian rules.

Malta 🇲🇹 (Permanent Residence)

Malta’s citizenship-by-investment route ended in 2025 after a European Court of Justice ruling, worth stating plainly because older guides still market a "Maltese passport." What remains is the Malta Permanent Residence Programme, which grants permanent residence from the outset and combines a government contribution, a property purchase or lease, and a philanthropic donation, with total outlay starting around EUR 150,000 when leasing and rising with property and family size. Malta stands out for unusually broad, multi-generation family inclusion, has no minimum stay, and uses English as an official language.

Hungary, Latvia, and the rest of Europe 🇪🇺

Hungary’s Guest Investor Residence Permit (2024) offers about EUR 250,000 into a government-accredited real estate fund or a EUR 1 million university donation, with a ten-year renewable permit, zero presence, and immediate Schengen rights; citizenship, however, requires roughly eight years of continuous full-time residence plus an exam. Latvia runs one of Europe’s cheapest programs, from around EUR 50,000 into a small company, EUR 250,000 in real estate plus a fee, or about EUR 280,000 in a five-year bank deposit (returned at the end), with no minimum stay. Bulgaria offers immediate permanent residency from a fund investment of around EUR 512,000, a flat 10% tax, and recent entry into Schengen and the euro. Cyprus grants permanent residency through a roughly EUR 300,000 property purchase plus a foreign-income requirement, with a single visit every two years and notable non-domicile tax advantages.

UAE / Dubai 🇦🇪

Outside Europe, the UAE answers a different question. The ten-year golden visa is commonly obtained through real estate of at least AED 2 million (roughly USD 545,000), as a single property or a portfolio, with no minimum stay and family inclusion within defined limits; a five-year option exists for older investors at a lower threshold. The headline draw is tax: the UAE levies no personal income tax, which matters for anyone who actually becomes UAE tax resident. Naturalization is rare and not a planning route.

Golden visa countries 2026: program status at a glance

A scannable summary. Treat every figure as a starting point for verification, not a quote, given how often these change.

Tax-residency note for the table above

None of these programs makes you a tax resident simply by issuing a permit. The favorable regimes often mentioned alongside them, Italy’s lump-sum tax, Portugal’s IFICI, the UAE’s absence of personal income tax, Bulgaria’s flat 10%, Cyprus non-dom rules, apply only if and when you actually become tax resident there.

What changed, and what closed

The recent history is as useful as the current menu, because it shows where policy is heading. The pattern across Europe is consistent: pressure over housing affordability plus institutional resistance to passive-investment pathways.

- Spain closed its program in 2025, framed as a response to housing pressure. Remaining residence routes require real physical presence.

- Malta’s citizenship-by-investment route ended in 2025 after an EU Court of Justice ruling. The MPRP residence program survived; the passport route did not.

- Portugal ended residential real estate in 2023, then spent 2025 and 2026 contesting the citizenship timeline; existing applicants filed legal challenges.

- Greece repriced its real estate tiers in 2024 and banned short-term rentals on qualifying properties.

- Ireland, the UK, and the Netherlands all discontinued investor routes in recent years, with no like-for-like replacement.

- Romania: Formally proposed and then abruptly cancelled a new program framework in 2025.

Two implications follow. The direction of travel favors funds, business and job creation, cultural and research contributions, and stricter source-of-funds review over passive property. And investors who already hold residency under prior rules are often treated differently from new applicants when rules change. Grandfathering is common but not guaranteed, and is exactly the kind of point to confirm with local counsel.

Why current verification is not optional?

Every program here is a moving target. A route open today can be repriced, restricted, or closed with limited notice, and citizenship timelines have proven especially unstable. Before committing capital, confirm the live rules against the relevant government source and a qualified local advisor.

Investment requirements compared, and what they actually cost

Comparing programs on the qualifying investment alone is a mistake. That number is the entry ticket, not the price of ownership. Two routes with identical headline figures can differ enormously once you account for fees, taxes, currency, liquidity, and the cost of getting your money back out.

Run any candidate program through the entire financial stack before comparing: government/processing fees, legal/advisory fees, international due diligence costs, multi-year fund charges, property transfer taxes, localized VAT, annual maintenance, structural renewals, and heavy currency exposure. (For instance, a Euro-denominated investment held by a USD-based investor carries real foreign exchange risk on both entry and exit). Price ranks them; it does not rank their fundamental asset suitability.

How to choose: which program fits which goal

There is no universal best golden visa program. The honest answer to "which is best" is "best for what?"

Layer three absolute filters over whatever these frameworks suggest: program stability (a route mid-reform carries heavy sovereign policy risk), investment quality (the commercial viability of the underlying asset matters infinitely more than the permit), and country stability (governance indexes, currency trends, and rule of law), because you are permanently tethering a slice of your asset base to that jurisdiction.

Golden visa tax implications for US citizens

The point US investors most need to hear

A golden visa does not turn off US worldwide taxation. The United States taxes its citizens and green card holders on worldwide income regardless of where they live or hold residence. Acquiring foreign residency, by itself, changes nothing about your US filing and tax obligations. The analysis shifts only if you physically relocate and the facts of where you live and bank change with you.

With that anchor in place, here is the terrain, in general terms and subject to professional advice.

- Worldwide taxation is the baseline: Income generated anywhere on earth remains completely reportable to the IRS; a foreign residence permit excludes none of it.

- Relocation creates dual exposure: Moving can quickly trigger local tax residency, leaving you navigating two parallel fiscal systems managed via exclusions, foreign tax credits, and double-taxation treaties.

- The Foreign Earned Income Exclusion (FEIE) has strict limits: The exclusion cap rests at USD 130,000 per qualifying individual for 2025 and scales to USD 132,900 for 2026, applies solely to earned (not investment/passive) income, and strictly mandates passing the physical presence test (330 full days abroad) or the bona fide residence test. You can review the explicit statutory baseline directly via the IRS Foreign Earned Income Exclusion portal.

- Foreign tax credits offer protection: These credits work to offset double taxation and are frequently more valuable than the exclusion mechanism for high earners managing heavy passive investment income.

- FBAR and FATCA reporting apply to foreign assets: Aggregated foreign accounts exceeding USD 10,000 at any point in the calendar year trigger a mandatory FinCEN Form 114 (FBAR) submission. IRS Form 8938 (FATCA) adds secondary reporting requirements above specific asset thresholds. Opening simple local bank accounts to fund a golden visa trips these filing triggers almost immediately.

- PFIC rules can aggressively penalize foreign fund holdings: Many non-US pooled investments, including the exact fund structures some European golden visas rely on, are classified as Passive Foreign Investment Companies. This triggers punitive tax brackets and incredibly complex accounting requirements. This remains one of the least understood traps for US investors executing a fund-based route, and checking active IRS Passive Foreign Investment Company guidelines with a cross-border CPA is vital.

- Expatriation carries heavy exit tolls: Relinquishing residency is completely separate from giving up citizenship; only formal renunciation of the latter terminates US tax obligations. If a US citizen renounces, hitting "covered expatriate" status can trigger a major mark-to-market exit tax on global assets.

For a US person, a golden visa is fundamentally a mobility and asset diversification decision, not a capital gains tax planning strategy. The hidden reporting requirements attached to foreign assets represent the part of the journey that quietly introduces the highest regulatory risk.

Tax residency for non-US global investors

For investors who are not US persons, the central planning fact is that a golden visa and structural tax residency are decoupled: you can hold the legal permit while remaining a tax resident elsewhere. Where you are actually taxed turns exclusively on physical day counts (commonly the 183-day test), your center of vital interests (where your family, primary home, and economic life sit), double-taxation treaty tie-breaker rules, and whether the destination state utilizes a worldwide or territorial tax apparatus.

Several jurisdictions intentionally pair golden visa pathways with highly attractive fiscal regimes for new arrivals:

- Italy offers its premium lump-sum regime on all foreign-source income (set at EUR 300,000 annually for arrivals from 2026).

- Portugal’s IFICI framework provides a flat 20% rate on qualifying professional income lines, though eligibility brackets remain tight.

- Bulgaria applies a uniform flat 10% income tax, while Cyprus offers non-domicile regimes, and the UAE levies zero personal income tax.

Each of these represents a strict tax-residence outcome that mandates you genuinely move and qualify locally; they are never portable benefits that travel with the visa itself.

The application process and due diligence

Programs differ in detail, but the spine is consistent. Treat this as the shape of the journey, not a substitute for a program-specific roadmap from counsel.

- Eligibility and goal review: Confirm the selected program structurally fits your actual timeline and family objectives before deploying capital.

- Source-of-funds documentation: Assemble a clean, perfectly auditable money trail. This has increasingly become the absolute make-or-break compliance step and is routinely slower than applicants expect.

- Background and due diligence checks: Undergo criminal-record, global sanctions, and reputational screening, which have become significantly tighter across all open jurisdictions.

- Choosing the qualifying investment: Select the specific asset class or fund on its standalone economic merits, not merely to clear a residency threshold.

- Legal counsel engagement: Retain specialized local and cross-border tax advice before moving capital across borders.

- Documents, submission, and biometrics: Translate, notarize, and apostille all records to strict sovereign standards, file the application dossier, and attend scheduled in-person biometric appointments.

- Approval and maintenance: Maintain the underlying investment for the mandated holding window, onboard eligible family members, and track renewal dates alongside physical stay rules.

Common delays are predictable: thin source-of-funds evidence, missing translations or apostilles, slow bank or registry documents, and administrative backlog (notably in Portugal). Build a buffer into any timeline tied to a relocation, a school year, or a tax-residency window.

How a golden visa reshapes your portfolio

This is where the conversation must advance beyond basic immigration mechanics. A golden visa rarely arrives in isolation; it brings new assets, foreign accounts, and legal obligations in a foreign jurisdiction that structurally alter the architecture of your wealth.

- New, highly illiquid exposure: A physical property or a locked fund allocation adds localized asset concentration in one country, often tilting an already real-estate-heavy net worth further out of balance.

- Multi-currency net worth dynamics: A slice of your capital is now fully denominated in a foreign currency, moving with global exchange rates entirely independent of the underlying asset's local performance.

- Severe liquidity constraints: Fund routes commonly lock up deployed capital for five to seven years, meaning that capital cannot be tactical or redeployed if market circumstances shift.

- Cross-border estate planning friction: Local forced-heirship rules can completely override your existing estate expectations and differ sharply from structures at home.

- Fragmented reporting and visibility: New offshore accounts and distributed assets trigger siloed statements, making it exceptionally difficult to calculate your true, consolidated wealth position.

The core strategic question is never simply "does this asset qualify me?" The real question is: "What does my personal balance sheet look like the day after this is executed, across every asset class, currency, and country, and is that the shape I want?"

Managing international assets after the visa

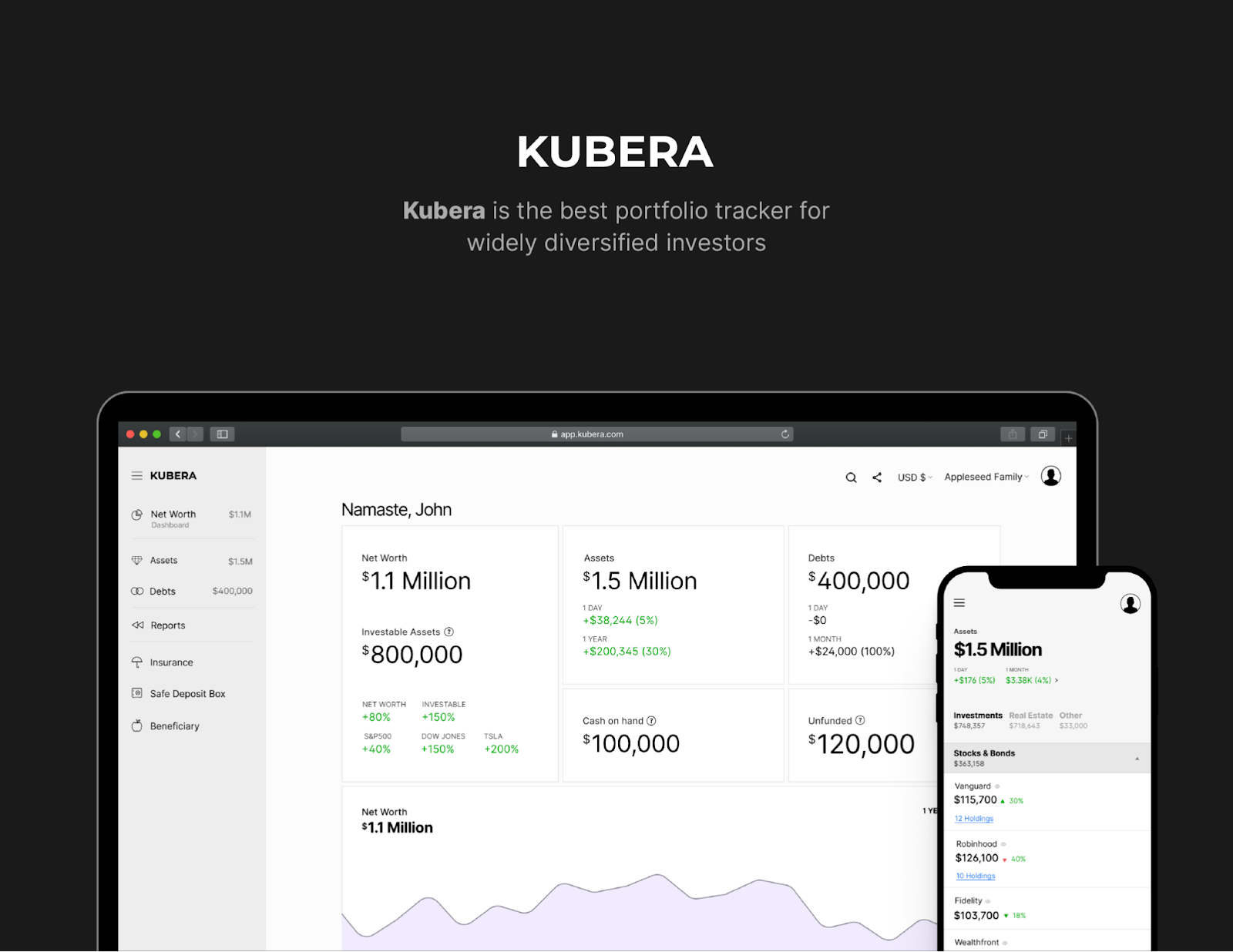

Once a golden visa is in place, the day-to-day reality is fragmentation: accounts in multiple countries and currencies, a foreign property needing periodic valuation, a fund reporting its NAV on its own schedule, statements in different languages and formats, and tax documentation assembled country by country. A spreadsheet that worked for a single-country portfolio becomes brittle once it has to reconcile several currencies, illiquid private assets, and accounts that connect to nothing, and advisors end up working from partial information. The need is straightforward: one consolidated, current picture of everything, across jurisdictions and currencies, that the right people can see.

When technology helps

Once your wealth spans countries, the hardest part is often not any single decision but seeing the whole position clearly and keeping it current. A tool like Kubera is built for this kind of globally distributed balance sheet. It can bring together bank and brokerage accounts, foreign real estate, investment funds, private equity, crypto, and manually tracked assets and liabilities into one view, with multi-currency net worth calculated for you. You can organize holdings by jurisdiction, see how much of your net worth sits in real estate, and compare your portfolio before and after acquiring a second residency.

It is also a way to keep international business and personal accounts visible in one place and to share a complete picture with advisors or family-office staff. For investors weighing a rental property abroad, a second home, or broader wealth protection across jurisdictions, that consolidated visibility is the foundation everything else rests on.

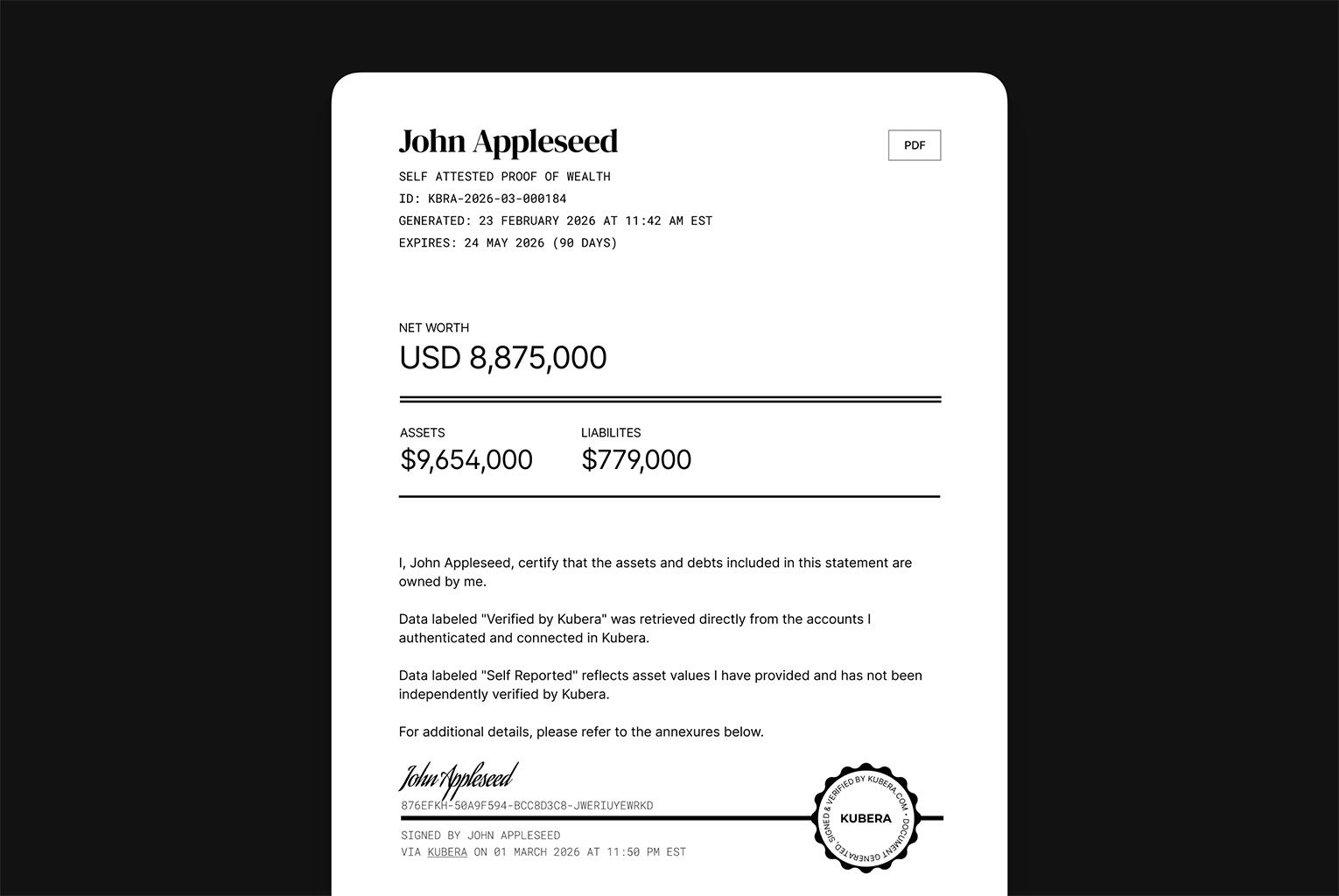

Because almost every golden visa hinges on documenting funds, this visibility has a second, practical use. Kubera's Proof of Wealth feature lets you generate a signed, self-attested statement of your assets, debts, and net worth as of a specific date, drawn from connected accounts rather than assembled by hand, and share it through a link the recipient can view without logging in.

For the proof-of-funds stage of a residency application, that can be a cleaner, faster way to present a comprehensive financial picture than a single bank statement or a stack of separate documents. It supports the application; it does not replace the formal source-of-funds dossier and legalized paperwork that programs require, which still has to be prepared with your advisors and counsel.

Frequently asked questions

What is a golden visa?

Generally a residency-by-investment program: you make a qualifying investment and receive the legal right to reside in a country, often to live and work. It grants residence, not citizenship, and does not by itself make you a tax resident.

Which countries have golden visas in 2026?

In Europe: Portugal, Greece, Italy, Malta (permanent residence), Hungary, Latvia, Bulgaria, and Cyprus. Outside Europe, the UAE. Spain closed in 2025, and Ireland, the UK, and the Netherlands ended theirs earlier. Always confirm current status.

What are the best golden visa programs?

There is no single best program. The right choice depends on the goal: EU mobility with low presence, lowest cost, family inclusion, tax efficiency if you relocate, a second home, or a future passport. A program ideal for one objective is often poor for another.

How much does a golden visa cost?

Qualifying investments range from around EUR 50,000 (Latvian business) to EUR 800,000 or more (premium Greek real estate), with the UAE around AED 2 million. The qualifying investment is only the entry point; total cost adds fees, taxes, fund charges, currency exposure, renewals, and exit costs.

Does a golden visa make you a tax resident?

No, not by itself. Tax residency is determined by where you actually live and local rules, commonly a 183-day or center-of-vital-interests test, not by holding a permit. You can hold a golden visa and remain tax resident elsewhere.

Can US citizens reduce taxes with a golden visa?

Not on its own. The US taxes citizens and green card holders on worldwide income regardless of foreign residence. Only a genuine relocation, and any foreign tax residency that follows, changes the analysis, and US filing continues. Foreign accounts and funds also bring FBAR, FATCA, and possible PFIC reporting.

What is the difference between residency by investment and citizenship by investment?

Residency by investment grants the right to live in a country; citizenship by investment grants a passport and nationality. A golden visa is the former. Some residency programs offer a long, conditional path to citizenship, but that is separate from the visa.

Do golden visas lead to citizenship?

Some do, eventually and on separate terms, usually requiring years of residency, language and integration tests, and in several countries real physical presence. Timelines have been extended and contested recently, notably in Portugal, so treat any timeline as subject to change.

What happens if a golden visa program closes?

Investors who already hold residency under prior rules are often, though not always, treated differently from new applicants (grandfathering). The exact treatment depends on the country and the law and can be litigated, so confirm your position with local counsel.

Conclusion

A golden visa can be genuinely valuable. For the right investor it buys mobility, a credible relocation option, regional access, family planning room, and a way to diversify across countries and currencies. But the value is conditional, and the conditions are the whole game: program stability, because the 2026 map is still moving; investment quality, because the asset behind the permit matters more than the permit; tax residency, decided by where you live, not what you hold; family needs and the fine print of who is included; clean source of funds; and, underneath all of it, your full global balance sheet.

Get those right, with current information and the right professional advice, and a golden visa becomes a considered part of a wider plan rather than a purchase. Get them wrong, and the cheapest program on the page can become the most expensive decision in the portfolio. The work is in matching the program to the goal, verifying the rules as they stand today, and keeping a clear, consolidated view of everything you hold while you do it.

Disclaimer

This article is general information for educational purposes and reflects program and tax details reported in early 2026. It is not legal, tax, immigration, or investment advice, and is not a recommendation of any program. Rules, minimums, stay requirements, citizenship timelines, and tax regimes change frequently and vary by nationality, family structure, source of funds, physical presence, and local law. Verify all details against official sources and consult qualified professionals before acting.