A donor-advised fund (DAF) is a charitable account held at a sponsoring public charity. You contribute cash or assets, claim an immediate DAF tax deduction in the year of the gift, and then recommend grants to qualified charities over time. The contribution is irrevocable, the sponsor holds legal control, and the assets can grow tax-free inside the account until you grant them out.

For affluent families, the core appeal is often not just the charitable act itself, but the timing, flexibility, and tax efficiency around it. A DAF separates the tax event from the charitable decision, which matters most in a high-income year, a liquidity event, or when a family wants to plan multi-year giving without the administrative drag of a private foundation. The donor-advised fund tax benefits are strongest when combined with appreciated-asset contributions, a charitable bunching strategy, or year-end planning around an unusually large income spike.

The real question is not whether a DAF is better than direct giving or better than a private foundation in the abstract. It is whether the lower friction is worth the loss of legal control for your specific goals. This piece walks through the mechanics, the 2026 tax changes, the donor-advised fund vs. private foundation decision, and the practical choices that matter when a DAF balance becomes meaningful relative to the rest of the balance sheet.

What Is a Donor-Advised Fund?

A donor-advised fund, or DAF, is a named giving account held inside a sponsoring public charity. The sponsor might be a national financial-institution charity such as Fidelity Charitable, DAFgiving360 (formerly Schwab Charitable), or Vanguard Charitable. It might be an independent national sponsor such as National Philanthropic Trust. It might be a community foundation, or a mission-specific sponsor tied to a university, faith tradition, or cause.

Whatever the sponsor, the mechanics are the same. You make an irrevocable contribution. The sponsor takes legal title. Because the sponsor is itself a public charity, your contribution qualifies for the most favorable charitable deduction limits available. The assets sit in your DAF account, invested inside the sponsor's menu, and you recommend grants to IRS-qualified public charities on your own timeline.

How a Donor-Advised Fund Works

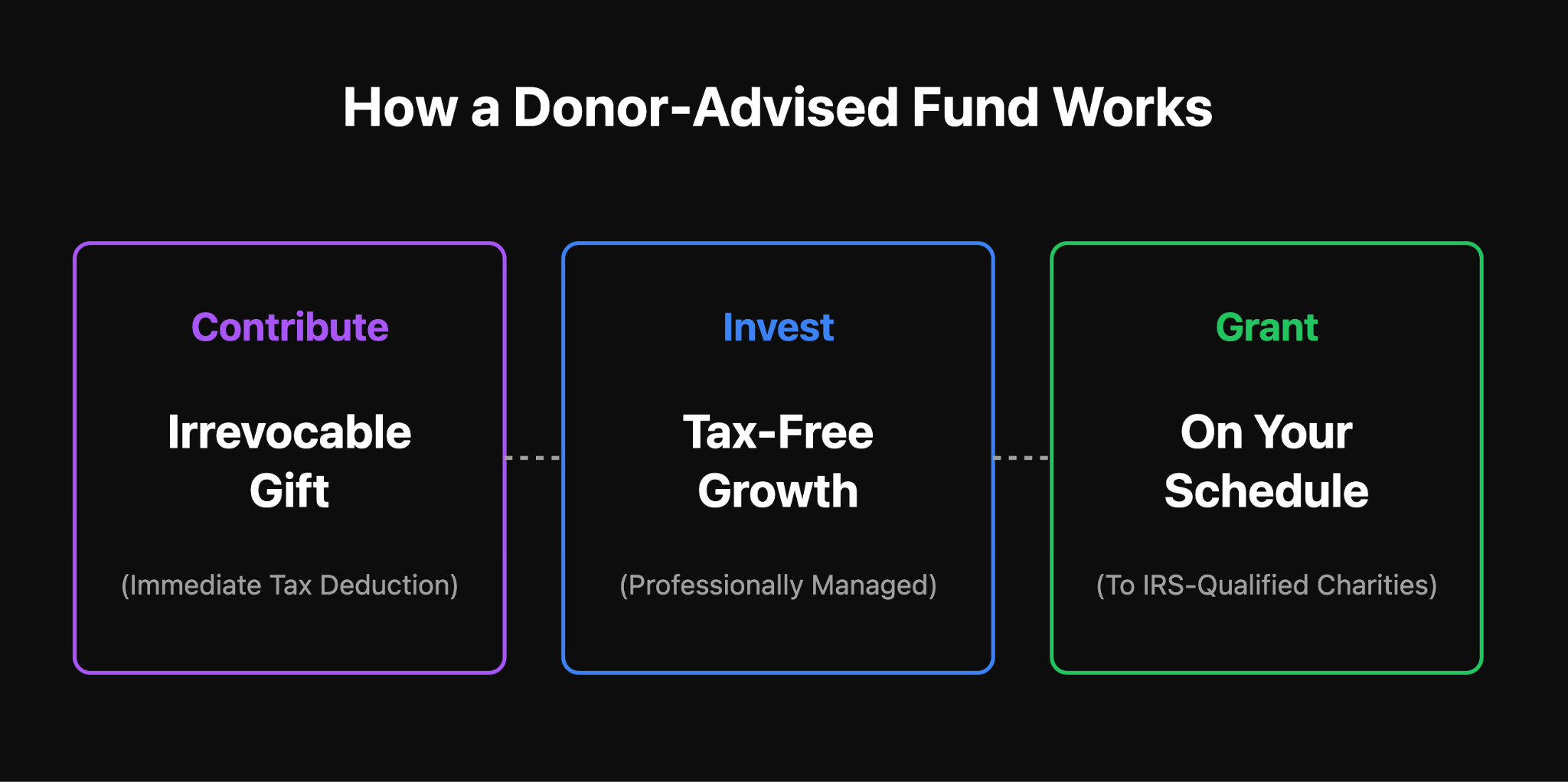

The vehicle has three steps, each doing different work.

1. Contribute

You transfer cash, publicly traded securities, or other accepted assets. The sponsor accepts the gift, generally liquidates non-cash assets, and credits the proceeds to your account. You receive documentation for an immediate income tax deduction in the year of contribution, subject to AGI limits and substantiation rules.

2. Invest

Assets inside the DAF are invested in the sponsor's menu or, at larger balances, in professionally managed accounts directed by your outside advisor. Growth is not taxed. Over long holding periods, that compounding quietly increases what eventually reaches charity.

3. Grant

When you are ready, you recommend grants to qualified public charities. The sponsor performs due diligence, confirms eligibility, and issues the grant. Most recommendations are approved. The sponsor retains legal authority to decline, which is the legal foundation that lets the original contribution qualify as a gift to a public charity.

The power in this sequence is timing: the deduction locks in at contribution, the grants happen on your schedule.

Donor-Advised Fund Tax Benefits

Three donor-advised fund tax benefits do most of the work.

First, the immediate income tax deduction. Cash contributions to a DAF are generally deductible up to 60% of adjusted gross income (AGI). Long-term appreciated assets such as publicly traded stock held more than one year are generally deductible at fair market value up to 30% of AGI. Amounts above those limits can be carried forward for up to five additional tax years.

Second, capital gains tax avoidance. Donating long-term appreciated securities directly to a DAF is usually more tax-efficient than selling and donating the proceeds. The donor avoids recognizing the gain, the DAF sells with no tax, and the full fair market value is available for grants.

Third, tax-free growth inside the account. Investment returns compound without capital gains or dividend tax.

The 2026 planning angle

Two charitable-deduction changes took effect in the 2026 tax year under the One Big Beautiful Bill Act. Itemizers now face a 0.5% of AGI floor, meaning only donations above that threshold count toward itemized deductions. For taxpayers in the 37% bracket, the tax benefit of itemized deductions is capped at 35 cents per dollar rather than 37. The 60% of AGI cash deduction limit to public charities was also made permanent.

These changes make DAF strategies more valuable rather than less. Bunching, front-loading, and appreciated-asset giving all help donors clear the 0.5% AGI floor in a single year rather than losing deductions year after year. For high earners watching the 35% cap, concentrating gifts in years with unusually high income is typically more efficient than spreading the same dollars across normal years.

One precise note: the new above-the-line charitable deduction for non-itemizers, up to $1,000 for single filers and $2,000 for joint filers, does not apply to contributions to donor-advised funds. That deduction is reserved for cash gifts made directly to operating public charities.

Charitable Giving Strategies That Fit a DAF Well

The charitable bunching strategy

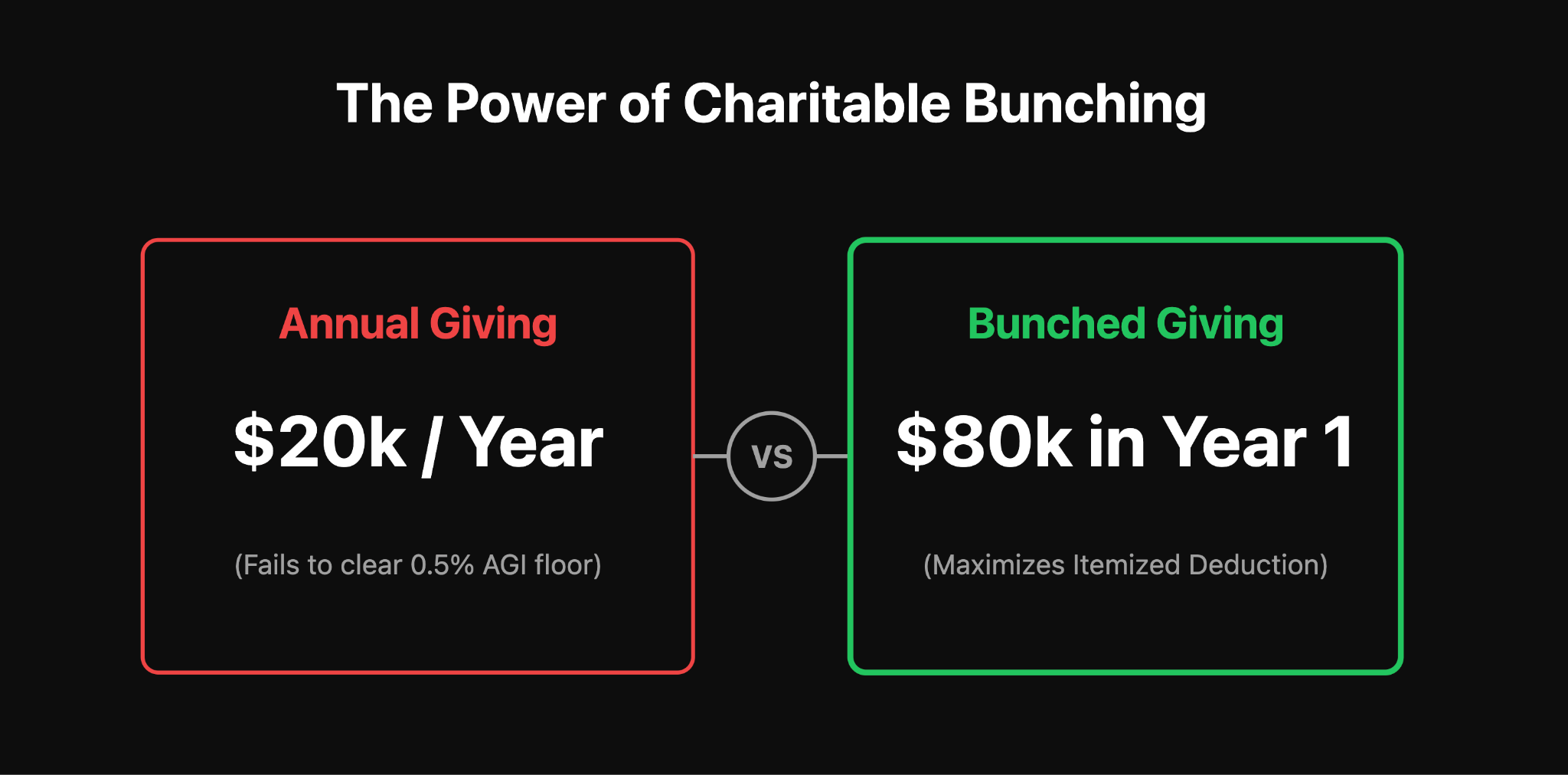

With the 2026 standard deduction at $32,200 for joint filers and a 0.5% AGI floor on charitable deductions on top, many households give meaningfully but never quite clear the itemization bar in any single year. The bunching strategy concentrates several years of planned giving into one tax year, funds a DAF with the lump sum, then grants at a normal pace over the following years. The donor itemizes in the bunching year, takes the standard deduction in the off-years, and keeps charities whole on the ground.

Example: bunching

Take a married couple with $450,000 of AGI, $25,000 of deductible state and local taxes, $8,000 of mortgage interest, and a habit of giving $20,000 a year. Under the 2026 rules, their $20,000 charitable gift is reduced by the 0.5% AGI floor of about $2,250, leaving $17,750 deductible. Combined with SALT and mortgage interest, total itemized deductions reach about $50,750, beating the $32,200 standard deduction by roughly $18,550 in a normal year.

If they bunch four years of planned giving into one, funding a DAF with $80,000, the floor still takes $2,250, leaving $77,750 of deductible charity that year. Total itemized deductions approach $110,750, beating the standard deduction by about $78,550. They take the standard deduction in the following three years while granting from the DAF at a normal pace. The charities see the same flow. The tax outcome is materially better.

Example: appreciated stock

A founder holds long-held public stock with a fair market value of $500,000 and a cost basis of $50,000. Selling the shares would trigger roughly $90,000 in federal long-term capital gains tax at the 20% rate, plus the 3.8% net investment income tax, plus state tax. Donating the shares directly to a DAF sidesteps the capital gains tax entirely. The donor generally captures a $500,000 fair-market-value deduction, subject to the 30% of AGI limit with a five-year carryforward, and the full $500,000 is available inside the DAF for grants.

Pre-liquidity events and business sales

Founders approaching a sale, executives with vested equity, and investors near a significant gain often have the largest deductible capacity they will ever have in a single tax year. Contributing shares to a DAF before the transaction closes, rather than donating post-sale cash, usually produces a meaningfully better outcome. One caution: if a sale is already contractually committed when the shares are contributed, the anticipatory-assignment-of-income doctrine can cause the donor to be taxed on the gain anyway. Involve a tax advisor and financial advisor early.

What Assets Can You Contribute to a DAF?

Sponsors accept a broader range of assets than most operating charities. What they accept readily and what takes lead time varies. The table below is directional, not universal. Confirm current policy with any sponsor before planning a complex contribution.

For anything beyond cash and publicly traded securities, sponsor choice and lead time become the variables that matter. Involve a tax advisor early, and counsel for private company interests or real estate.

Donor-Advised Fund vs Private Foundation

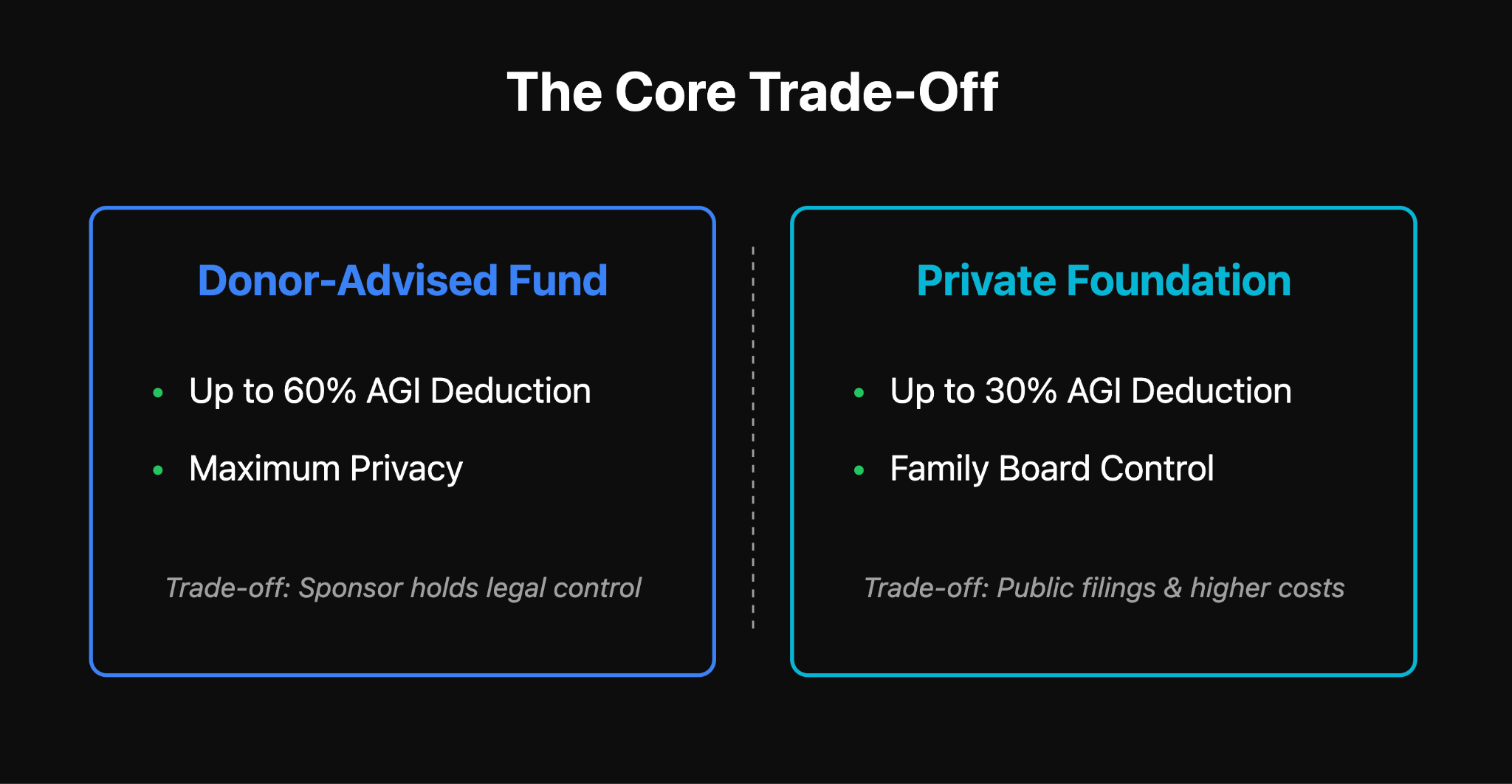

The donor advised fund vs private foundation question is the one most high-net-worth families end up wrestling with, and the one most often oversimplified. Both are legitimate charitable vehicles built for different goals.

For most donors, the DAF wins on three axes: higher deduction limits, no mandatory payout, and no compliance burden at the donor level. The two vehicles are not mutually exclusive. Plenty of families operate a foundation for legal control and pair it with a DAF to capture the broader tax advantages on appreciated-asset gifts and anonymous grants.

Privacy and anonymity

One underdiscussed difference between the two vehicles is how public they are. A DAF grant can be made anonymously, with only the sponsor's name appearing in the recipient's acknowledgment. For donors who give to controversial causes, sensitive religious or political organizations, or simply prefer not to be added to every mailing and gala list, this matters. Private foundations, by contrast, file a public Form 990-PF each year that discloses grants, trustees, compensation, and investment holdings. Some families welcome that transparency. For others, it is the single largest reason the DAF wins. Anonymity is also useful during family formation, when adult children are still defining their own giving identities and may not want their early grantmaking on the permanent public record.

When a private foundation clearly wins

A private foundation is the right vehicle, not the consolation prize, when the family's charitable work genuinely needs its own legal form. Scholarship programs that select individual recipients. Disaster-relief grants made directly to families. Program-related investments below market rate. Paid executive director roles filled by the next generation. Mission-related investing that wants flexibility beyond what a sponsor's menu allows. In any of these cases, the DAF's restrictions become binding rather than trivial. The cost and compliance burden of a foundation is then not a tax inefficiency to minimize but a price paid for the vehicle that actually fits.

Estate Planning and Family Legacy Uses

A DAF intersects estate planning in several ways. Naming the sponsor as the beneficiary of a traditional IRA or qualified plan is often the most tax-efficient charitable bequest available. Pretax retirement assets pass to the DAF without income tax and are removed from the taxable estate, while after-tax assets pass to heirs.

The estate and gift tax exemption was made permanent at $15 million per individual and $30 million for married couples starting in 2026, with inflation adjustments thereafter. Estate taxes are no longer the driver of charitable planning for most households, but for families above the exemption, charitable transfers at death still reduce the taxable estate meaningfully.

During life, successor advisors are the mechanism that turns a DAF into multigenerational philanthropy. Adult children, and in some cases grandchildren, can be named as successors. When the primary advisor dies, successors assume advisory privileges on the account or on separate accounts carved from the balance. Sponsor rules on how long that continuity persists vary, and reading them before funding significant balances is a decision many families wish they had made earlier.

How to Compare Donor-Advised Fund Sponsors

Sponsor choice affects fees, flexibility, service, and succession. Rather than publishing a sponsor-by-sponsor price sheet that will age quickly, the framework below covers the variables that matter. Confirm current specifics directly with any sponsor under consideration.

- Minimums. Some national sponsors (including Fidelity Charitable and DAFgiving360) have no minimum to open. Others (Vanguard Charitable, National Philanthropic Trust, many community foundations) require an initial contribution in the $10,000 to $25,000 range.

- Administrative fees. Most large sponsors use tiered schedules that commonly start around 0.60% on the first tier and step down as balances grow. Investment expenses sit on top. At higher balances, total cost compresses.

- Minimum grant size. Some sponsors allow grants as small as $50; others set higher minimums. Donors who grant to many small charities should confirm this.

- Investment menu. Menus range from a handful of asset-allocation pools to hundreds of options, with professionally managed accounts directed by an outside advisor typically available above a balance threshold.

- Complex-asset acceptance. Private company stock, real estate, restricted securities, and alternative-fund interests require sponsor experience. National sponsors and specialized independents handle these routinely; smaller sponsors may not.

- Succession terms. Some sponsors allow perpetual family advisory rights through named successors. Others sunset them after one or two generations. Read the specifics before funding.

- Service model. National sponsors offer scale. Community foundations add local nonprofit knowledge. Mission-specific sponsors serve particular traditions or causes.

The table below groups sponsors by archetype rather than by current price sheet, capturing where each type tends to fit best.

The practical difference shows up most clearly between straightforward donors and complex-asset donors. For cash-and-stock donors, sponsor differences are modest; for real estate, private stock, or fund interests, they become decisive. A donor who plans to contribute cash and publicly traded stock, grant to a handful of mainstream charities, and leave things there will have a nearly identical experience across the national sponsors. Fees compress at scale, grants clear quickly, and the service model is light by design. A donor contributing private company stock, real estate, or restricted securities lives in a different reality. Sponsor diligence, qualified appraisals, legal review, and internal acceptance committees stretch the timeline into weeks or months. Here, sponsor experience with the specific asset class matters far more than the published fee schedule, and the right sponsor is the one that has done the exact gift type recently.

Rules and Restrictions Worth Knowing

A few constraints trip up even experienced donors.

- No grants to individuals. Scholarships running through a qualified public charity are fine; direct individual grants are not.

- No political contributions. DAFs cannot grant to 501(c)(4) organizations for lobbying purposes, PACs, or candidates.

- No more than incidental personal benefit. A grant that pays for a gala table where the donor receives a meal or entertainment generally is not permitted from a DAF.

- Pledges. Grants generally cannot be used to satisfy a legally binding pledge in ways that produce more than incidental benefit to the donor. Sponsors have specific language on this.

- Qualified Charitable Distributions (QCDs) from an IRA cannot go directly to a DAF. They must go to an operating public charity. Donors 70½ and older need to plan around this.

- The sponsor has legal authority to decline a grant recommendation. In practice this is rare for mainstream charities. Sponsor policies sometimes interpret these rules more strictly than the legal minimum. A grant that clears quickly at one sponsor may trigger extra review at another.

What Happens to a Donor-Advised Fund When You Die?

This is the question most donors put off the longest and one of the most important to answer before funding meaningful balances. If a successor advisor was named, that person assumes advisory privileges under the sponsor's rules. Some sponsors split the balance proportionally into separate accounts for multiple successors; others keep the account intact with shared advisory privileges. If charitable beneficiaries were designated, the balance passes to those charities on a schedule the donor chose.

If no successor or beneficiary was named, the sponsor's abandoned-account procedures take over. Those typically direct the balance to the sponsor's general charitable purposes or to prior grantees in some proportion, which is almost never the outcome the donor would have chosen. Sponsors also differ on how long advisory rights persist across generations: some allow perpetual family advisory rights through named successors, others sunset those rights after one or two generations and distribute according to donor instructions or sponsor defaults. For families planning multigenerational philanthropy, these terms are worth reviewing before a contribution becomes irrevocable.

Tracking a DAF Inside the Household Balance Sheet

DAF balances often grow larger than donors expect. Contributions, grants, appraisal documents, and quarterly statements accumulate across a sponsor that sits outside the family's primary custodian. Once contributions span multiple alternative asset types and grants run across many charities, a platform built for tracking total wealth, like Kubera, can help. It gives families one place to track DAF balances, store contribution confirmations and appraisals, log grant history, and connect the DAF to the rest of the balance sheet. The goal is not to replace sponsor statements but to make future giving decisions against the full picture rather than a partial one.

Frequently Asked Questions

What is a donor-advised fund?

A charitable giving account held by a sponsoring public charity. The donor contributes assets, receives an immediate income tax deduction, and recommends grants to qualified charities over time. The contribution is irrevocable, and the sponsor holds legal title.

What are the main donor-advised fund tax benefits?

An immediate income tax deduction, deductibility at fair market value for long-term appreciated securities, capital gains avoidance on donated appreciated assets, tax-free growth inside the account, and a five-year carryforward above the AGI limits.

Is a donor-advised fund better than direct giving?

It depends on the goal. Direct giving is simpler and can qualify for the new above-the-line deduction for non-itemizers. A DAF is usually more efficient for large gifts, appreciated-asset gifts, bunching, and situations where the donor wants time to decide which charities to support.

What is the difference between a donor-advised fund and a private foundation?

A DAF is an account inside a public charity. A private foundation is a separate legal entity controlled by the donor. DAFs offer higher deduction limits, no excise tax, no mandatory payout, and more privacy. Foundations offer legal control, paid family roles, and the ability to grant to individuals or run programs a DAF cannot.

Can you donate appreciated stock, crypto, or real estate to a DAF?

Yes at most major sponsors, though timelines differ. Publicly traded stock is processed quickly. Cryptocurrency is accepted at most national sponsors. Real estate, private company stock, and alternative-fund interests require sponsor review, qualified appraisals, and usually weeks to months of lead time.

What is a charitable bunching strategy?

Bunching concentrates several years of planned giving into a single tax year, usually by funding a DAF with the lump sum. The donor itemizes in the bunching year and takes the standard deduction in the off-years while continuing to grant from the DAF at a normal pace.

Can I make a QCD to a donor-advised fund?

No. Qualified Charitable Distributions from an IRA must go to an operating public charity, not to a donor-advised fund, a private foundation, or most supporting organizations.

What happens to a donor-advised fund when I die?

If successor advisors are named, they assume advisory privileges under the sponsor's rules. If charitable beneficiaries are designated, the balance passes to those charities. If neither is in place, the sponsor's default policies apply.

A Balanced Final Word on the Donor-Advised Fund

A donor-advised fund is not a universal answer. It is a well-engineered vehicle for a specific set of problems: capturing a deduction in the year that matters, giving appreciated assets without tax friction, bunching to clear new itemization thresholds, and spreading charitable decisions over a longer horizon than any single tax year allows. For affluent families whose giving is already meaningful and whose tax picture has real variability, a DAF usually earns its place.

It does not replace everything else. For legal control, paid family roles, or the granular grantmaking that defines a dedicated family philanthropy, a private foundation still fits better. For donors 70½ and older with large IRAs, Qualified Charitable Distributions remain one of the most efficient tools available and bypass the DAF entirely. The right plan often uses more than one vehicle.

The questions worth answering before opening a DAF are mostly human. What should your giving look like over the next decade? Who should carry it forward? How much legal control are you willing to trade for simplicity? The structural answers follow from the human ones.