Concierge medicine is a membership-based model of primary care. The patient pays an annual retainer, often structured as a monthly fee, and the practice limits the size of its physician panel so each member gets more time, faster responses, and a deeper doctor-patient relationship. In return, members usually get longer appointments, same-day or next-day availability, direct contact with their primary care physician, and tighter coordination across labs, imaging, specialists, and hospital care. It is not insurance. It typically supplements an insurance plan instead of replacing one.

For affluent families, the question is rarely whether concierge medicine sounds appealing. It usually does. The real question is whether the annual fee buys enough access, coordination, and prevention to justify the cost, and how the spending fits into the broader operating budget of a wealthy household. This article covers what concierge medicine actually costs at different tiers, how it differs from direct primary care, what the retainer covers (and what insurance still handles), where the value tends to be real, and where it tends to be oversold.

What Concierge Medicine Actually Is

Concierge medicine is sometimes called retainer medicine, membership medicine, or boutique medicine. The core idea is straightforward. A primary care physician shrinks the patient panel from the traditional 2,000 to 3,000 patients down to a few hundred. Some ultra-premium practices go further and cap the panel at 50 families. With a smaller panel, the physician can spend more time with each patient, return calls personally, hold longer appointments, and coordinate care with specialists in a way that traditional primary care rarely supports.

The patient pays an annual or monthly fee for that access. The fee is the practice’s way of replacing the revenue it would otherwise generate from a higher volume of insurance-billed visits. In most concierge models, the practice still bills insurance for medical services that are eligible for reimbursement. The retainer pays for everything insurance does not, such as longer visits, direct communication, extended care planning, and the simple fact of being a member rather than a name on a long roster.

What the membership generally buys

- Longer appointments, often 30 to 60 minutes for routine visits and multi-hour annual physicals at premium practices.

- Same-day or next-day appointments for urgent concerns.

- Direct phone, text, or email access to your concierge doctor.

- A more proactive approach to prevention, screening, and chronic condition management.

- Care coordination across specialists, labs, imaging, and hospital admissions.

- Annual physicals that go beyond the standard insurance-billed visit, sometimes including extended labs and risk assessment.

What it generally does not buy

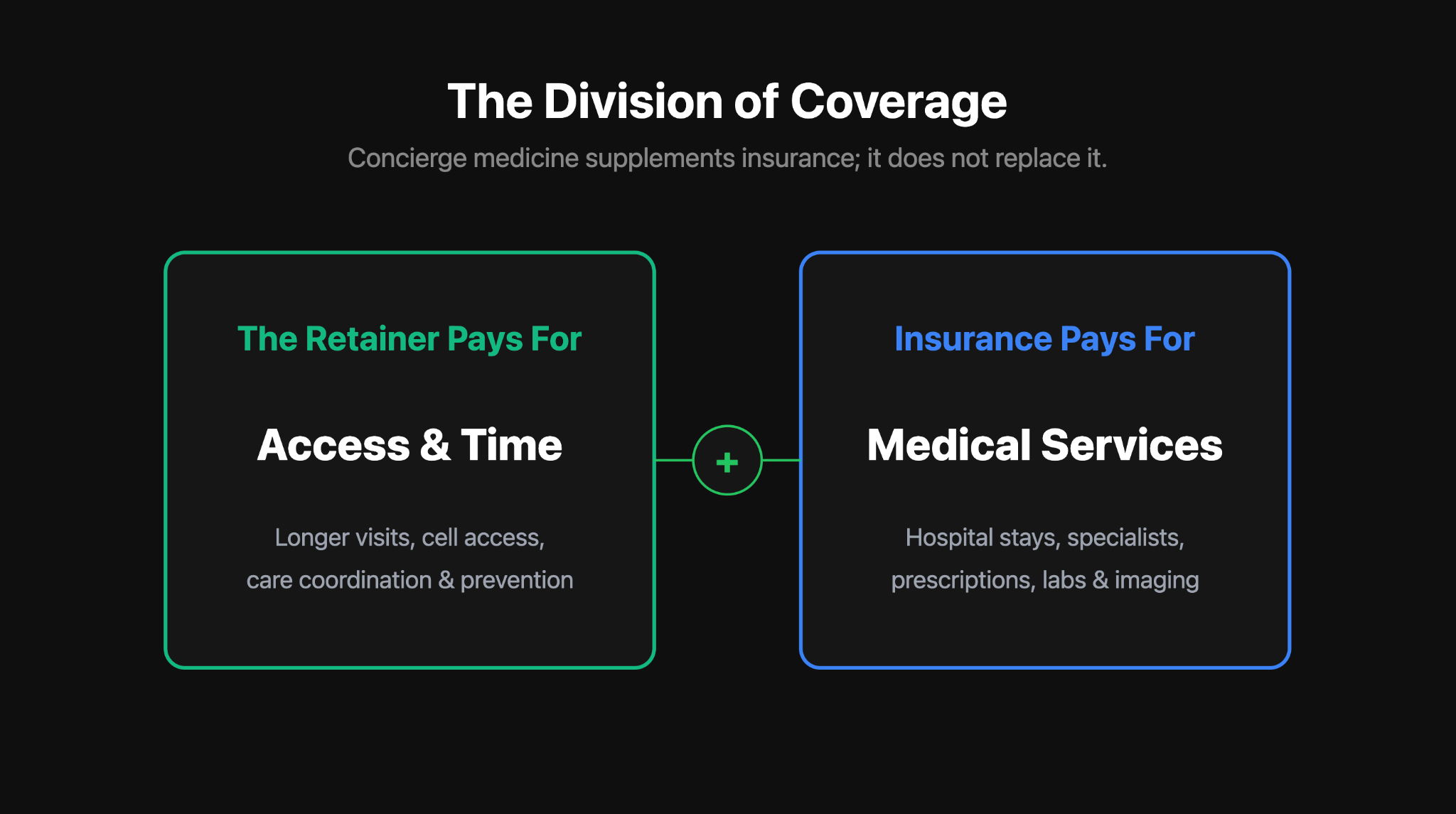

Concierge medicine is a primary care services model. It does not replace specialists, surgery, hospital care, or emergency services. It does not eliminate the need for an insurance plan, and it does not change how serious medical events are billed. Buying a concierge membership without keeping a health insurance plan in place is, in most situations, a planning mistake. The retainer is an access fee layered on top of insurance, not a substitute for it.

Important: concierge medicine supplements insurance; it does not replace it. Hospital stays, specialist visits, imaging, surgery, prescriptions, and emergency care still flow through your health insurance plan. The retainer covers access and the relationship. Anyone treating the membership as a substitute for insurance is taking on unnecessary financial risk.

Concierge Medicine vs Direct Primary Care

These two models get confused constantly, partly because both involve membership fees and longer appointments. They are different products built for different audiences.

Direct primary care, or DPC, is generally an insurance-free arrangement. Patients pay the practice directly, usually $50 to $200 per month, and that fee covers most primary care services including routine visits, basic labs, and care coordination. The American Academy of Family Physicians describes DPC fees as typically lower than concierge fees, with the membership covering a broader range of primary care services. DPC practices usually do not bill insurance, and patients are often still advised to carry coverage for hospitalization, specialist care, and major medical events.

Concierge medicine usually does bill insurance for covered services. The retainer is layered on top of insurance, not in place of it. Fees are typically higher than DPC, panel sizes are similar or smaller, and the model tends to emphasize depth, access, and coordination rather than transparent primary care pricing. Concierge practices are also more likely to invest in extended annual physicals, longevity-focused diagnostics, and dedicated care coordination staff.

Neither model is universally better. DPC tends to win on affordability, transparent pricing, and simplicity. Concierge medicine tends to win on depth, executive-style assessments, and complex care coordination.

Concierge medicine vs direct primary care at a glance

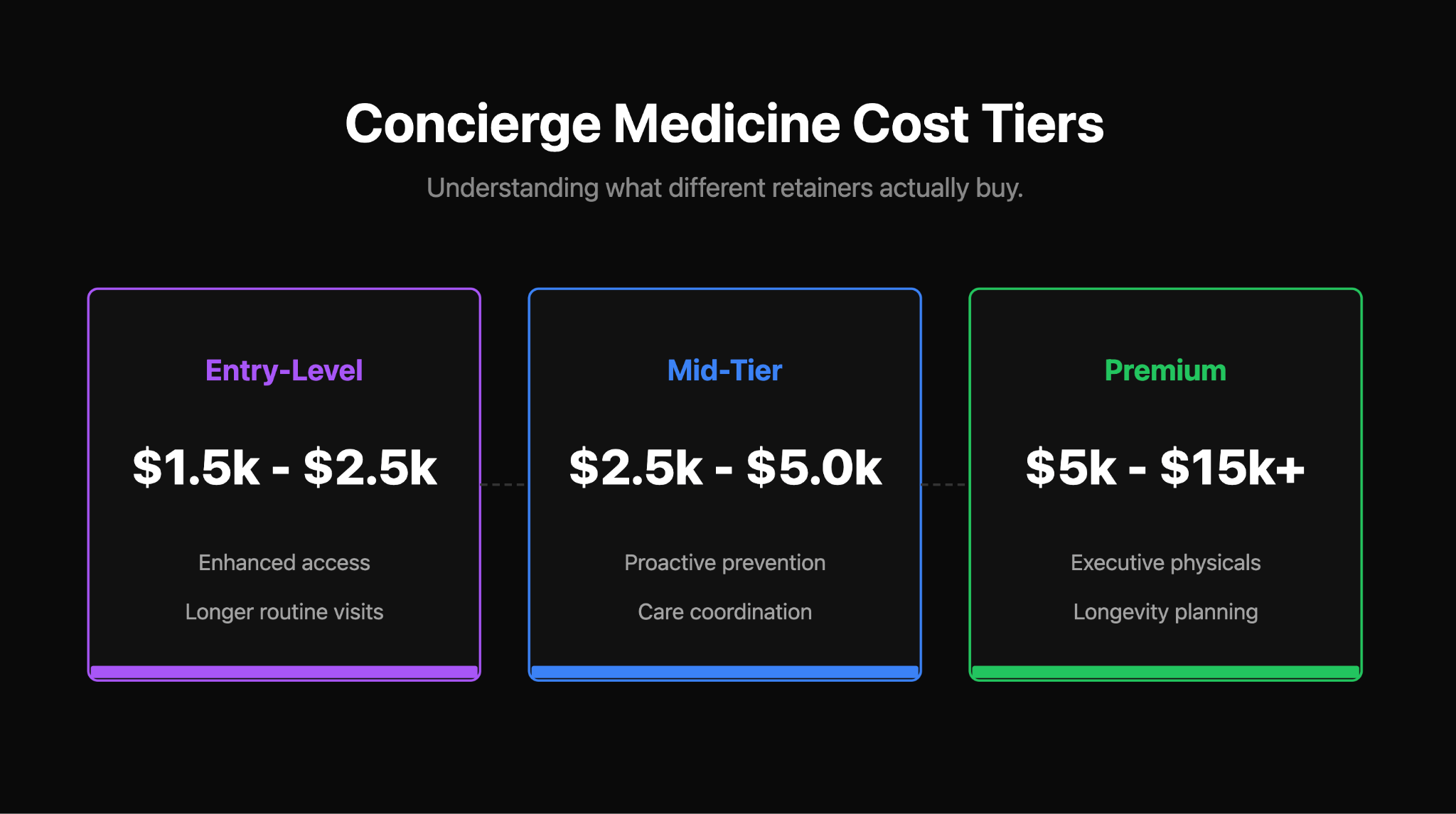

What Concierge Medicine Costs at Every Tier

Headline ranges are not very useful on their own because the model spans practices charging $1,500 per year and practices charging $40,000 or more. Thinking in tiers is more practical. Each tier reflects a different combination of panel size, scope of services, and physician time, and each fits a different kind of patient.

The figures below reflect commonly cited market ranges from current practice reporting and industry sources. They are not specific recommendations. Costs vary materially by city, physician, included services, family size, and whether a practice is part of a national network or a standalone practice.

Concierge medicine cost tiers

Two notes on the numbers: First, fees at the top end of each tier are not necessarily a sign of higher-quality medicine; they often reflect smaller panels, more time, and more concierge-style amenities. Second, even the highest tier still operates alongside a real insurance plan. A $40,000 retainer usually does not pay for a hospital admission, surgery, or oncology treatment.

What the Membership Fee Covers and What Insurance Still Covers

Asking whether concierge medicine takes insurance is the wrong starting question. The right question is what the membership pays for and what is still billed through insurance. A clean way to think about it is that the retainer pays for the relationship and the access, and insurance pays for the medicine.

Usually Included in the Retainer

- Annual physicals, often more extensive than a standard insurance-covered annual visit.

- Longer appointments and same-day or next-day availability.

- Direct phone, text, or email access to your concierge physician.

- Care coordination with specialists and follow-up oversight.

- Wellness planning, prevention strategy, and chronic condition support.

Usually Still Billed to Insurance

- Specialist visits and consultations.

- Labs, imaging, and diagnostic testing performed outside the practice.

- Hospital admissions, surgery, and emergency room visits.

- Prescription medications.

- Most procedures, even when ordered by the concierge doctor.

There is also a regulatory line worth understanding. A well-run concierge practice should clearly separate retainer-covered enhancements from services billed to Medicare or commercial insurance. Retainers are typically tied to non-covered benefits such as enhanced access, longer visits, care coordination, or communication, rather than duplicating services already reimbursed by insurance. Practices that blur this line have run into compliance scrutiny, and the cleanest practices keep the two streams clearly separated.

The Financial Case for Concierge Medicine

Concierge practices often market the model as cost-saving in the long run. The truth is more nuanced. A 2025 systematic review in The American Journal of Medicine (Maximizing the Value of Concierge Medicine) concluded that evidence on clinical outcomes from concierge medicine is limited, even as patient satisfaction is consistently higher. Industry-affiliated studies have reported substantial reductions in hospitalization rates, sometimes cited in the 40 to 70 percent range, but most of those studies were sponsored by or conducted in collaboration with concierge practices themselves. An independent 2023 economics analysis (Mansour et al., Journal of Health Economics) found that switching into concierge care was associated with 30 to 50 percent higher total healthcare spending and no measurable change in mortality on average.

That does not mean concierge medicine has no financial logic. It means the financial logic is not primarily about reducing total healthcare spending. For most HNW families, the real value is in time, access, and risk management.

Where the Value Tends to Come From in Practice

- Time: A founder, executive, or surgeon who loses a day to a sick visit, a referral process, and a follow-up call is paying a much higher cost than the visit copay.

- Faster access to evaluation: Same-day or next-day appointments can prevent escalation, especially for chronic conditions and travel illnesses.

- Coordination: Multiple specialists, multiple residences, and aging parents create administrative complexity that a well-run concierge practice can absorb.

- Prevention and earlier detection: Longer visits and structured screening protocols can surface issues earlier, although outcomes evidence on this is mixed.

- Continuity: A physician who knows the patient deeply tends to make fewer redundant referrals and order fewer duplicative tests.

A Balanced View of the Financial Case

For some families, concierge medicine reduces friction more than it reduces spending. The annual fee may not pay for itself in lower bills, but it can pay for itself in saved time, faster decisions, and fewer administrative gaps. For other patients, especially generally healthy people with simple needs, the retainer is an unnecessary cost. The value is highly situational.

Executive Physicals and Longevity-Focused Care

Many concierge practices market an executive physical, sometimes called an executive physical concierge program. The format varies. At the simpler end, it is a longer annual visit with extended labs and a more thorough cardiovascular review. At the premium end, it is a multi-hour or multi-day evaluation with comprehensive labs, advanced cardiovascular screening, metabolic markers, imaging where appropriate, lifestyle and stress assessment, and a follow-up plan that integrates with the patient’s broader medical care.

Executive physicals can be genuinely valuable, particularly for patients with family history of cardiovascular disease or cancer, complex risk profiles, or limited prior access to comprehensive screening. They can also catch issues early when they are easier to manage. But more testing is not automatically better testing. Broader screening protocols carry a higher rate of false positives, incidental findings, and follow-up tests that can generate anxiety and downstream costs without changing outcomes. The quality of the follow-up matters more than the number of tests.

A few questions are worth asking before signing up for an executive physical: What screening tests are appropriate for someone with my risk profile, and what is included only because it can be marketed? How are incidental findings handled? What is the practice’s philosophy on overtesting? Is there a structured plan to connect findings back to my regular medical care, or does the physical sit in a silo?

What Concierge Care Looks Like for High-Net-Worth Families

For HNW households, the case for concierge medicine often shows up in coordination and continuity rather than in any single appointment. The same physician who manages a founder’s cardiovascular risk might also be coordinating an elderly parent’s post-discharge care, advising on travel medicine for a teenager spending a year abroad, and handling a referral for a household staff member if the family covers that benefit.

Common HNW use cases

- Whole-family coordination across children, spouses, and aging parents, often with a single point of medical contact.

- Multiple residences and frequent travel, with arrangements for care while away from home and physician availability across time zones.

- Privacy and discretion, including how records are handled and how specialist referrals are arranged.

- Chronic condition support that integrates with specialists rather than running in parallel.

- Hospital advocacy when a family member is admitted, including coordination with hospitalists and discharge planning.

- Executive-style preventive care for principals whose health disruptions affect business continuity.

- International travel medicine, including pre-trip planning and access to vetted local providers if something goes wrong abroad.

The picture is not always glamorous. Much of what families pay for is mundane but valuable: someone returning a call within an hour, a referral that does not require three phone calls, an annual physical that flows directly into a coordinated plan, an aging parent whose medication list is actually reconciled rather than reconstructed during each specialist visit. The value is in the friction that disappears.

Who Concierge Medicine Is Right For, and Who Should Skip It

The strongest predictor of value is not income. It is how much the patient or family actually uses the access, and how complex their care is to coordinate.

Concierge medicine fit assessment

How to Evaluate and Choose a Concierge Doctor

The biggest variable in concierge medicine is not the brand on the door. It is the physician and the practice. Two practices charging the same retainer can deliver very different experiences depending on panel size, on-call coverage, and how the practice actually behaves when something is wrong on a Saturday night. A short list of questions can usually separate a well-run practice from a marketing-heavy one.

A Reality Check Before Joining Any Practice

The model matters less than the physician. A strong traditional primary care doctor may outperform a weak concierge practice, especially if the concierge practice sells access but does not deliver coordination. The retainer pays for behavior, not branding.

Questions worth asking before joining

- How many patients are on the physician’s panel, and is that a hard cap?

- What response time is committed to, in writing, for calls, texts, and messages?

- Are same-day appointments and next-day appointments routinely available, or are they aspirational?

- Is the physician personally reachable after hours, or does the practice rely on a covering provider?

- What is included in the retainer, and what is billed separately or to insurance?

- Does the practice coordinate directly with specialists, or only refer?

- How are emergencies handled, including weekend and holiday coverage?

- Does the physician still admit or coordinate hospital care, or does that hand off entirely to a hospitalist?

- What happens if the physician is on vacation, on leave, or eventually leaves the practice?

- How are records, communication, and privacy handled, including for family members?

- Does the practice support multiple residences, travel, and care while away from home?

- Are there family or household pricing options, and how do they work for children, spouses, and aging parents?

- What is the cancellation policy, and is any portion of the fee refundable if you leave mid-year?

How Concierge Medicine Fits Into HNW Lifestyle Costs

Concierge medicine sits alongside other premium services that wealthy households tend to accumulate over time: household staff, property management across multiple residences, private aviation arrangements, insurance programs, advisory fees, and security. Each one is reasonable in isolation. Together, they form a recurring operating cost that is easy to underestimate.

For most affluent families, the challenge with these expenses is not affordability. It is visibility. Costs get spread across personal accounts, trust accounts, family office statements, business entities, and credit card cycles. A concierge medicine retainer for two spouses and two children, plus an annual executive physical, plus a separate retainer for an elderly parent, plus the insurance premiums that still sit underneath all of it, can add up to a meaningful annual line item that no one looks at as a single number.

The point is not that any one cost is excessive. It is that the household benefits from seeing all of them in one view, alongside the assets and liabilities that fund them. A clear picture of recurring lifestyle spending tends to lead to better decisions about which premium services are pulling their weight and which were signed up for years ago and quietly renew.

When Technology Helps

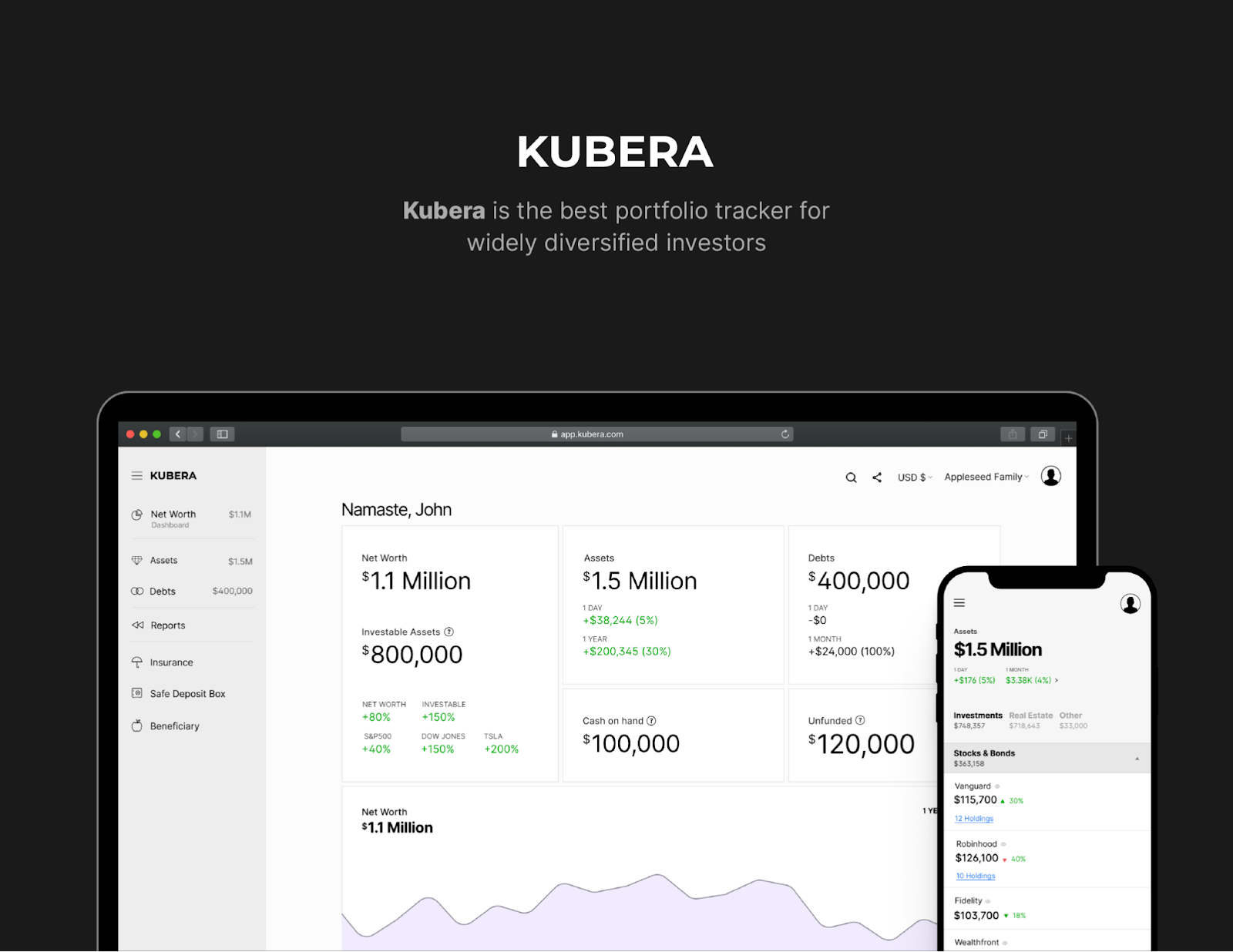

Most HNW households end up with their financial life scattered across multiple banks, brokerage accounts, business entities, trusts, real estate holdings, private investments, and recurring lifestyle costs that live on a mix of cards and accounts. Healthcare spending is part of that picture, even if it is not the largest part. Concierge memberships, family insurance premiums, executive physical upgrades, and out-of-pocket medical costs are all recurring commitments that benefit from being tracked alongside everything else.

Kubera is one tool that families and family offices use to bring this picture into one view. It is not a healthcare tool. It does not track medical records, care plans, or clinical outcomes. What it does is give a household a single place to see assets, liabilities, real estate, investments, insurance policies, and the ability to plan for recurring expenses such as concierge memberships, advisory fees, and household operating costs. For families thinking about whether a $5,000 or $25,000 retainer fits comfortably alongside everything else they pay for, that kind of visibility is genuinely useful. The decision about concierge medicine becomes easier when the rest of the household financial picture is not a blur.

Sign up now for a 14 day trial to get started and explore more.

Frequently Asked Questions

What is concierge medicine?

Concierge medicine is a membership-based primary care model. Patients pay an annual or monthly fee for enhanced access to a primary care physician who limits the practice’s patient panel. The fee typically buys longer appointments, same-day or next-day access, direct communication with the physician, and care coordination. It is usually layered on top of an insurance plan, not in place of one.

How much does concierge medicine cost?

Most concierge memberships fall between $2,000 and $10,000 per year. Entry-level practices often charge $1,500 to $2,500. Mid-tier practices commonly run $2,500 to $5,000. Executive health and premium programs typically range from $5,000 to $15,000. Ultra-premium and family-office-style practices can charge $15,000 to $40,000 or more per member or per family. Costs vary by market, services included, and panel size.

Is concierge medicine worth it?

It depends on use and complexity. Concierge medicine tends to be worth it for patients managing a chronic condition, families coordinating care across specialists or generations, executives whose health disruptions affect business continuity, and people who travel frequently. It tends not to be worth it for generally healthy patients with simple needs who already have a primary care doctor they like, or for people whose main goal is lower total healthcare bills.

Does concierge medicine replace health insurance?

No. Concierge medicine supplements insurance. The retainer covers access and the relationship with the primary care physician. Hospital stays, specialist visits, imaging, labs, prescriptions, and emergency care still go through your insurance plan. Treating concierge medicine as a substitute for insurance is a planning mistake.

What is the difference between concierge medicine and direct primary care?

Direct primary care, or DPC, is generally insurance-free and charges lower monthly fees of roughly $50 to $200 per month. The fee covers most primary care services. Concierge medicine typically charges higher annual fees, still bills insurance for covered services, and emphasizes deeper access, longer appointments, and care coordination. DPC is built around affordability and predictable primary care pricing. Concierge medicine is built around depth, access, and coordination.

What does a concierge doctor do?

A concierge doctor functions as a primary care physician with a smaller patient panel and more time per patient. The same physician handles routine care, annual physicals, preventive screening, chronic condition management, and triage of urgent concerns, while coordinating with specialists when needed. Many also provide direct contact by phone, text, or email and handle care coordination during hospital stays.

Can concierge medicine help with chronic conditions?

It often can, particularly when proactive coordination across specialists and consistent monitoring matter. Longer visits and direct access make it easier to manage conditions like hypertension, diabetes, and cardiovascular risk in a more structured way. That said, evidence on whether concierge medicine produces better clinical outcomes than well-run traditional primary care is limited, and outcomes depend heavily on the physician and the patient’s engagement.

What is an executive physical?

An executive physical is a more comprehensive version of an annual physical. It typically includes extended labs, cardiovascular screening, metabolic markers, sometimes advanced imaging, lifestyle and stress assessment, and a detailed follow-up plan. Many concierge practices include some form of executive physical in the retainer or offer it as an upgrade. The quality of the follow-up and integration with regular medical care matters more than the volume of tests.

Are concierge medicine fees tax deductible or HSA eligible?

Sometimes, with limits. Traditional concierge retainers are often not fully HSA-eligible, especially when fees primarily cover access or exceed DPC limits. The IRS treats fees paid for actual medical services as deductible medical expenses under Section 213(d), subject to itemization and the 7.5 percent of adjusted gross income floor, with the physician usually providing an allocation between medical services and access. Starting January 1, 2026 under the One Big Beautiful Bill Act, qualifying DPC arrangements up to $150 per month for individuals or $300 per month for families may be HSA-compatible. That HSA treatment generally does not extend to most concierge memberships at typical price points. A tax advisor should weigh in on individual situations.

Conclusion

Concierge medicine is best understood as paid access and coordination, not as a different kind of medicine. The annual or monthly fee buys time, attention, and a closer doctor-patient relationship. It does not buy better outcomes by default, and it does not replace insurance. The right question is not whether concierge medicine is good or bad in the abstract. It is whether a specific practice, at a specific price, with a specific physician, fits a specific family’s needs.

For some families, the model is genuinely transformative. Complex medical histories get coordinated, aging parents get advocacy, executives get the same physician on the phone in twenty minutes instead of waiting a week for a referral. For other families, the retainer is an expensive subscription to a service they rarely use. The difference is rarely about the practice. It is about fit.

Treat the decision the same way you would treat any other major recurring household commitment. Understand what the fee actually buys. Compare it to what direct primary care or a strong traditional primary care practice would provide. Confirm the practice can absorb the parts of your medical life that create the most friction. And track the cost alongside your other recurring obligations so it does not quietly become invisible.