A hedge fund minimum is the smallest capital commitment a fund will accept from a single investor. For many hedge funds, that figure falls between $250,000 and $1 million. Flagship and institutional strategies routinely set the bar at $5 million or higher, while newer managers launching a first fund may accept $100,000 or less from early backers.

But the dollar figure on the subscription document tells only part of the story. The hedge fund minimum investment sits on top of investor qualification rules that determine who can participate at all. Whether you need to be an accredited investor, a qualified client, or a qualified purchaser depends on the fund's regulatory structure, and each threshold carries its own requirements. For a high net worth individual evaluating this space, the practical question is not just "can I get in?" It is whether the strategy, fees, liquidity terms, and transparency make the allocation worthwhile after you have cleared every gate.

At a Glance

- Typical hedge fund minimums range from $100,000 to $10 million or more, depending on fund size, strategy, and investor type. Stated minimums and actually accepted tickets often differ.

- Investor qualification matters as much as the check size. Most funds require accredited investor status at minimum. Many larger funds require qualified purchaser status ($5 million or more in investments).

- Minimums are strategic, not arbitrary. Fund managers use them to shape their investor base, control operational costs, and manage redemption risk.

- Fees, lock-ups, and liquidity terms are part of the true cost. A $500,000 minimum with a two-year lock-up and 20% incentive fee is a fundamentally different commitment than a $500,000 allocation to a liquid fund you can sell tomorrow.

- Lower-minimum access paths exist, but they come with tradeoffs. Fund-of-funds often start around $100,000 to $500,000 and add another fee layer, while liquid alternative funds may have no meaningful minimum but cannot replicate unconstrained hedge fund strategies.

How Much Do Hedge Funds Actually Require? Minimums by Fund Tier

One of the most common questions is simply how much to invest in a hedge fund. The answer depends heavily on the fund's size, stage, and target investor base.

A stated minimum is not always rigid. A compelling investor (strategic fit, long time horizon, referral from an existing LP) may gain access below the headline number. Feeder fund structures and platform vehicles can also effectively lower the entry point by pooling capital from multiple investors. And follow-on investments after the initial subscription often carry a much lower minimum, sometimes $25,000 to $100,000. But if a fund is willing to accept a dramatically lower amount from a new investor with no relationship, that is itself a signal worth interpreting.

Why Hedge Fund Minimums Are So High

- Regulatory arithmetic. A 3(c)(1) fund capped at 100 investors that targets $500 million in assets needs an average commitment of $5 million per investor. High minimums are not a preference; they are math.

- Operational cost per investor. Each limited partner creates subscription documents, KYC/AML compliance, quarterly statements, K-1 tax reporting, and investor relations overhead. Fund managers generally prefer fewer, larger relationships.

- Investor base composition. A $5 million minimum attracts a different investor than a $100,000 minimum. Managers who want sophisticated, patient capital use high minimums to filter for that profile. A concentrated LP base of institutions and large family offices tends to be more stable than a fragmented base of smaller investors who may redeem at the first quarterly drawdown.

- Capacity and signaling. In strategies where capacity is limited, a high minimum protects against dilution and signals selectivity. Some of this is genuine. Some is marketing discipline. Either way, it communicates something about the fund's positioning.

For many individuals, the practical barrier is not accredited status. It is that a hedge fund allocation only starts to make sense when the rest of the balance sheet is already very liquid.

Who Qualifies to Invest in a Hedge Fund?

Dollar minimums are only one gate. Most hedge funds also screen for one of three investor standards: accredited investor, qualified client, or qualified purchaser. Each threshold does a different job.

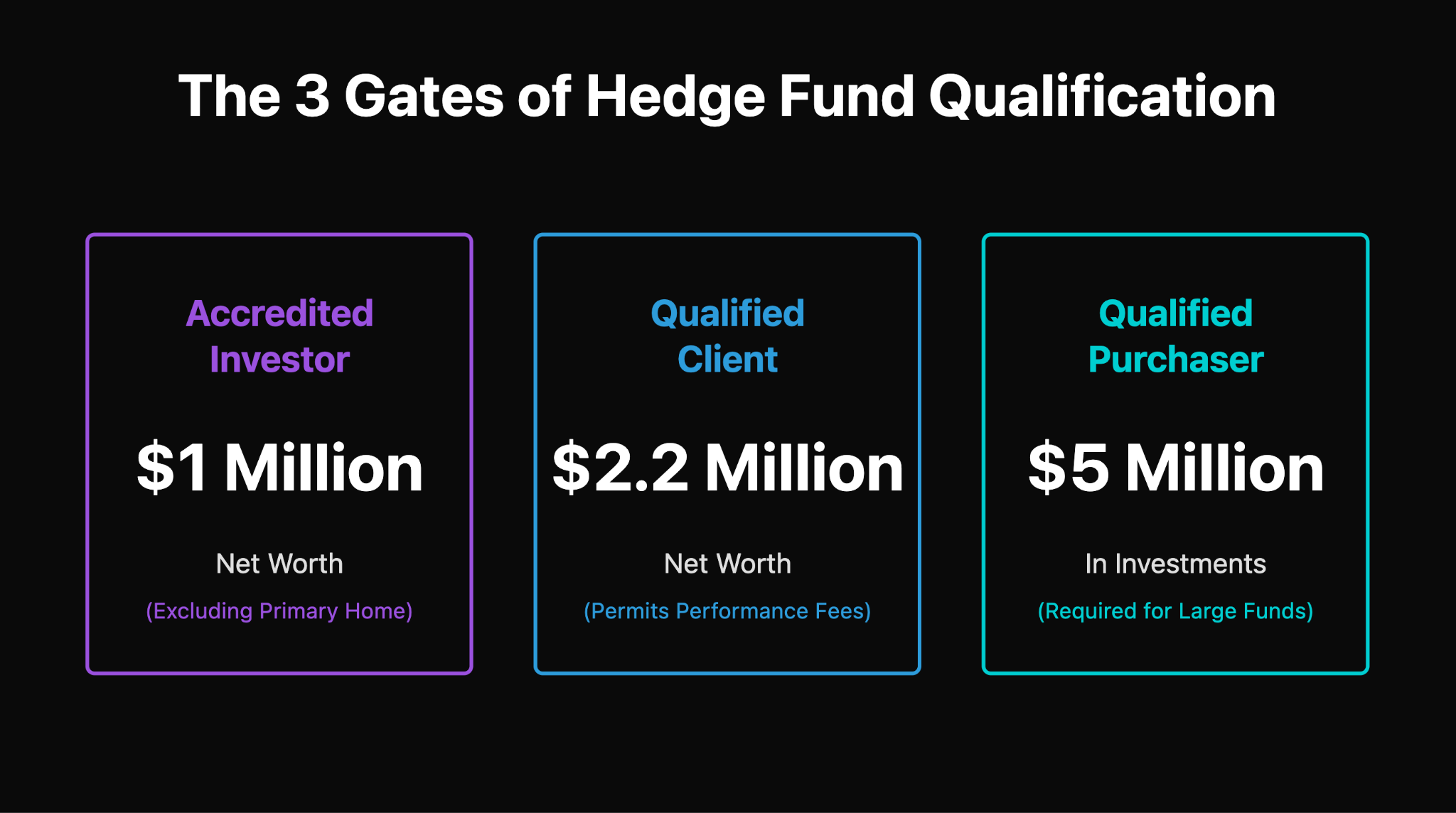

Accredited Investor

The baseline gate for most hedge funds. Under SEC Regulation D, an individual qualifies with a net worth exceeding $1 million (excluding the value of a primary residence) or annual income exceeding $200,000 individually ($300,000 jointly) in each of the prior two years, with a reasonable expectation of the same going forward. Holders of FINRA Series 7, 65, or 82 licenses also qualify. The hedge fund accredited investor threshold is explained in detail in Kubera's net worth categories guide, which maps where different wealth levels fall relative to these standards.

Funds relying on the 3(c)(1) exemption of the Investment Company Act can accept up to 100 accredited investors. That investor-count cap is one reason minimums tend to be high: fewer investors at higher amounts lets the fund raise adequate capital without bumping up against regulatory limits.

Qualified Client

Under Rule 205-3 of the Investment Advisers Act, a registered investment adviser may only charge performance-based fees to qualified clients. The current thresholds (as of the August 2021 SEC adjustment) are $1.1 million in assets under management with the adviser or a net worth of at least $2.2 million, excluding a primary residence. This matters because the classic hedge fund incentive fee (typically 15% to 20% of profits) is a performance-based fee. If the fund's investment manager is registered with the SEC, the qualified client threshold is what permits that fee arrangement.

Qualified Purchaser

Meaningfully higher. An individual qualifies by owning $5 million or more in investments (not net worth, and excluding a primary residence and business property). Entities need $25 million. The qualified purchaser hedge fund structure, organized under the 3(c)(7) exemption, can admit up to 2,000 investors, far more than the 100-investor cap under 3(c)(1). This is how many of the largest managers operate. If you are evaluating a flagship fund, there is a strong chance it requires this status. Kubera's comparison of qualified purchaser vs. accredited investor standards explains the distinction, and their ultra-high-net-worth guide provides context on the wealth levels typically involved.

Many people focus on the accredited investor hurdle and stop there. In practice, the more important question is often whether a fund wants qualified purchasers, institutional commitments, or only existing relationships.

Hedge Fund Minimums by Strategy

Strategy design affects minimum size because it influences the fund's capacity, operational complexity, liquidity profile, and target investor. The ranges below are directional, not definitive. Individual funds vary widely within each category.

Strategy affects minimums because it affects both capacity and investor behavior. Distressed and activist funds usually demand larger, stickier commitments because positions are harder to exit and timelines are longer. Long/short equity and some macro funds can accept smaller tickets because the underlying instruments are more liquid and redemption terms are easier to manage. Quant funds are a mixed case: some can take smaller allocations because operations scale well, while others are tightly capacity-constrained and want a narrower investor base.

Fees, Lock-ups, and the Real Cost of Access

The minimum to invest in a hedge fund is not the only capital commitment to budget for. The fee structure and liquidity terms determine the true economic cost of participating.

How Much Do Hedge Funds Charge?

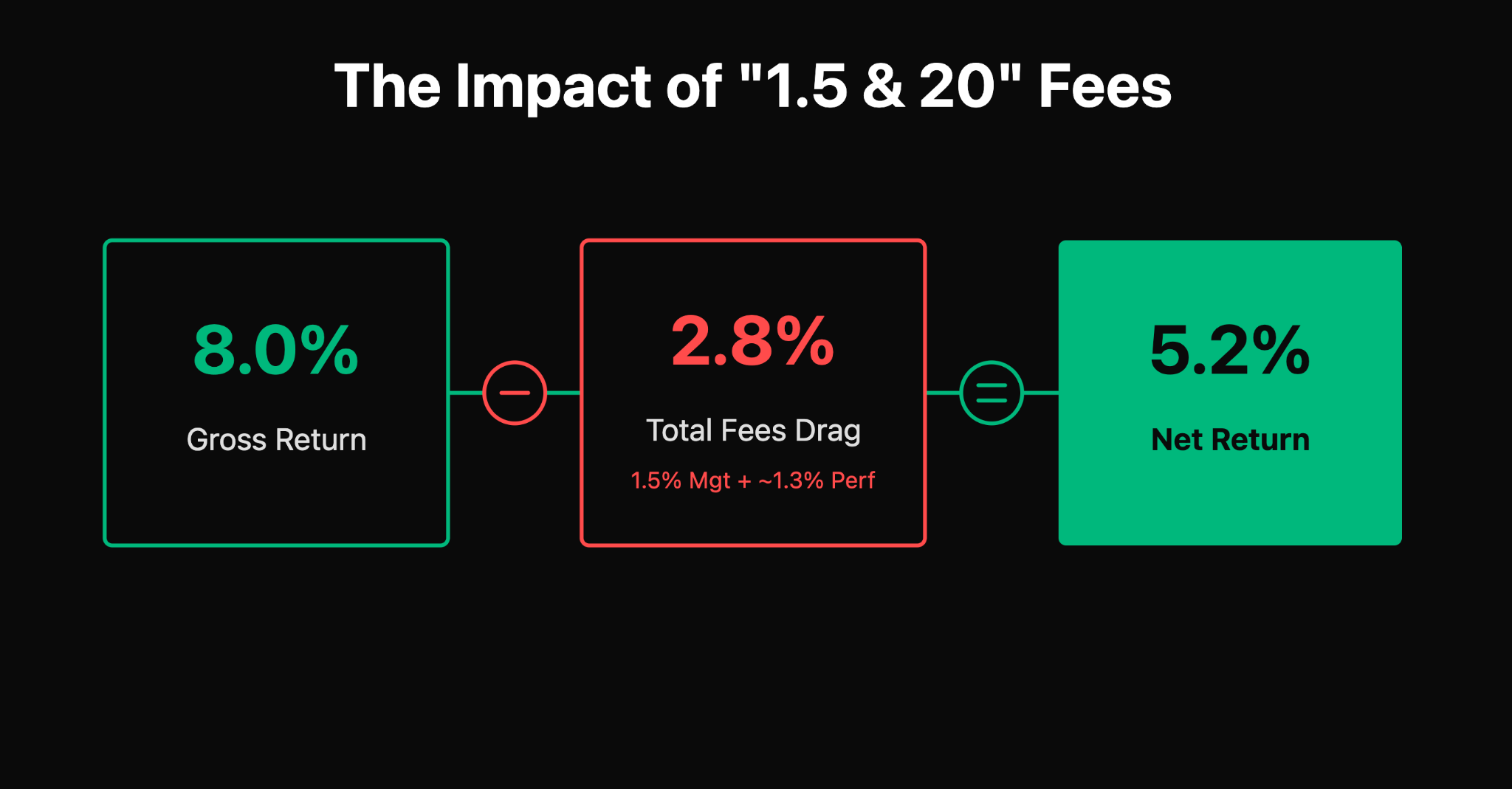

The traditional fee model is often described as "2 and 20": a 2% annual management fee and a 20% incentive fee on profits. Industry surveys suggest that fee compression has pushed many funds closer to 1.5% and 15% to 18% in recent years, particularly for institutional investors or larger commitments, though fee terms vary widely by fund. Some emerging managers offer lower fees to attract early capital. Administrative, legal, and trading costs are typically passed through on top of stated fees.

Example: what 1.5 and 20 means in practice

If a hedge fund returns 8% gross in a year:

- Gross return: 8.0%

- Management fee: 1.5%

- Performance fee on remaining gain: about 1.3%

- Approximate net return before taxes: about 5.2%

That is the difference between a good gross return and a merely decent investor outcome.

The discipline to evaluate net-of-fee, net-of-tax performance rather than headline gross returns separates experienced allocators from everyone else.

Hedge Fund Lock-Up Period

Lock-ups of one to two years are common. After the lock-up expires, redemptions are typically permitted quarterly or semi-annually with 30 to 90 days of advance notice. Gates may limit the total percentage redeemable in any period. Side pockets segregate illiquid holdings that cannot be fairly valued or sold on the fund's normal schedule. For investors accustomed to daily liquidity in public markets, this is a fundamentally different contract. Capital committed to a hedge fund should be treated as part of your illiquid allocation, alongside private equity and direct real estate.

Can Minimums Be Waived or Negotiated?

Yes, in certain circumstances. But this is not a standard access path, and treating it as one would be a mistake.

- Seed investors and first-close capital. Early backers who commit before or at the first close often receive reduced fees, co-investment rights, or lower minimums in exchange for taking launch risk. These arrangements are formalized through side letters.

- Friends and family. Many emerging managers accept smaller commitments from personal contacts or former colleagues. These allocations may come with lower minimums but identical terms otherwise.

- Strategic anchor investors. A pension fund or endowment that commits a meaningful anchor investment may negotiate preferred terms, sometimes for co-investors alongside them.

- Follow-on contributions. Once you are an existing LP, additional contributions typically have a much lower minimum, often $25,000 to $100,000.

- Platform and feeder access. In practice, many individual investors get below-headline access not by negotiating directly with the fund, but by investing through a feeder vehicle, private bank platform, or wealth management platform that pools commitments and negotiates a lower effective minimum. The investor still pays for that convenience, whether through fees, less flexibility, or both.

The key distinction: stated minimums and accepted tickets are different things. Early-close investors, strategic seeders, and existing LP relationships sometimes get in below the headline minimum, while ordinary new individual investors usually do not. An institutional investor writing a $200 million check has negotiating leverage that an individual writing $500,000 simply does not. If you are being offered dramatically reduced terms without a clear reason, that is worth questioning rather than celebrating.

Hedge Fund vs Mutual Fund Minimum

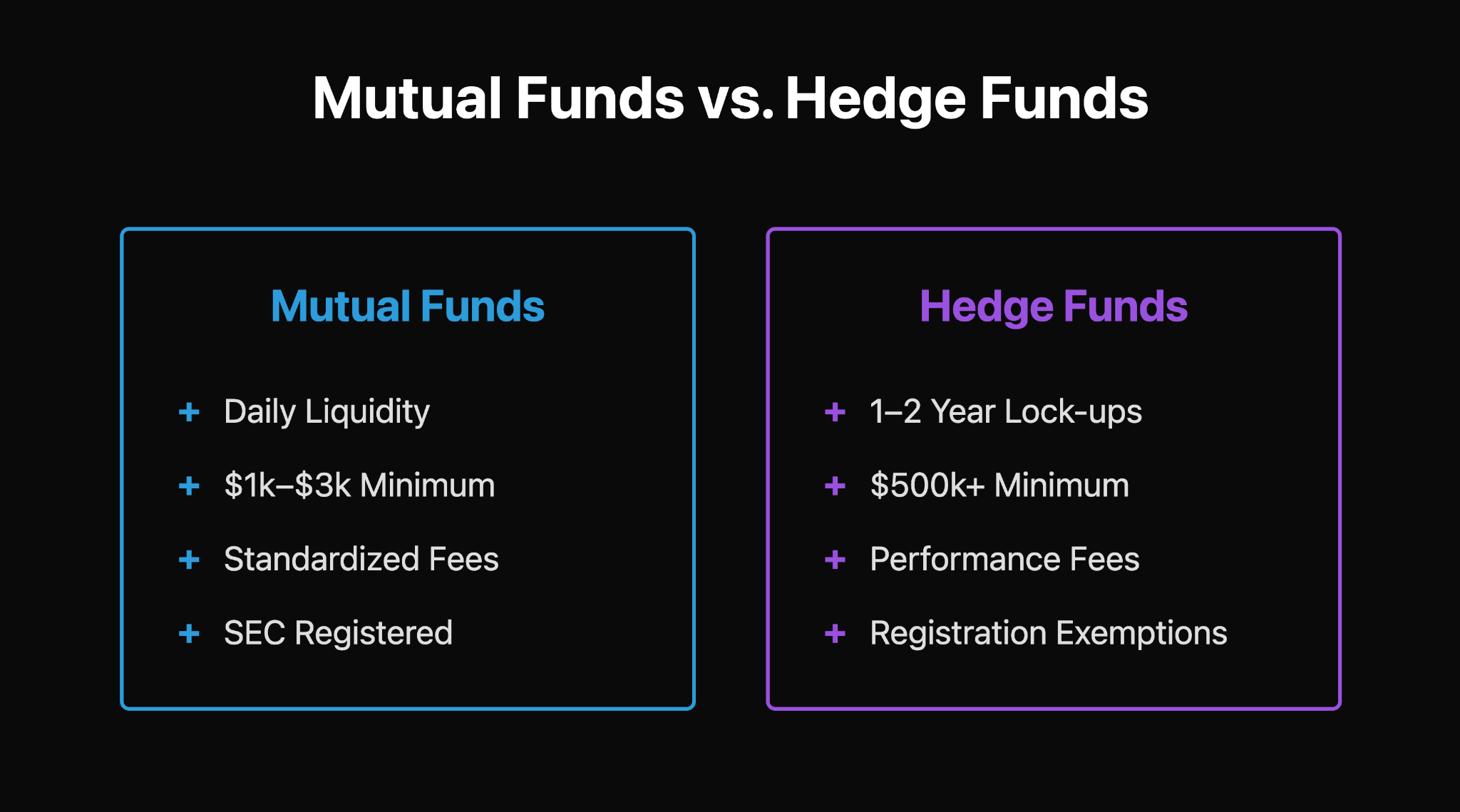

Mutual funds offer daily liquidity, regulatory disclosure, minimums of $1,000 to $3,000, and standardized fees. Any retail investor can participate. Hedge funds offer strategies that mutual funds generally cannot replicate: concentrated shorting, unconstrained leverage, illiquid and private investments, and flexible mandates. The tradeoff is higher minimums, restricted liquidity, less transparency, and higher fees.

Liquid alternative funds sit between the two. These are registered mutual funds and ETFs that use hedge-fund-like strategies within a regulated wrapper. Minimums are low, liquidity is daily, and fees are lower than traditional hedge funds. They provide some diversification benefit, but regulatory constraints on leverage, concentration, and illiquidity limit their ability to replicate what an unconstrained fund can do. For some investors, liquid alternatives are a perfectly reasonable substitute. For others, they are a compromise that misses the point. Kubera's guide to portfolio diversification offers a framework for thinking through the tradeoffs.

Alternatives if You Cannot Meet Hedge Fund Minimums

- Fund-of-funds. These pool capital from multiple investors and allocate across a portfolio of underlying hedge funds. Minimums often fall in the $100,000 to $500,000 range, which makes them one of the most realistic access paths for investors below direct fund thresholds. The tradeoff is cost. A common structure might charge 1% management and 10% incentive at the fund-of-funds level on top of the underlying funds' own fees. On an 8% gross return at the underlying manager level, that extra layer can materially reduce what reaches the end investor. You gain diversification and manager selection, but you pay for both.

- Liquid alternative mutual funds and ETFs. Accessible to all investors within the Investment Company Act framework. Useful for adding return-diversifying strategies without the lock-up and minimum constraints of a direct allocation. Kubera's alternative investments and alternative assets guides cover the broader landscape.

- Publicly traded alternative asset managers. Companies like Blackstone, Apollo, and Ares are publicly listed and provide indirect exposure to alternative investment management. Buying their stock is not the same as investing in their funds, but it offers economic participation in the industry.

None of these fully substitute for a direct hedge fund allocation. They are approximations, each with its own cost, complexity, and compromise. A fund with a lower minimum is not automatically more accessible in any meaningful sense if the liquidity terms are still restrictive.

How to Evaluate Whether a Hedge Fund Is Worth the Minimum

Meeting the minimum does not mean you should write the check. The minimum tells you something about the fund's desired investor base, but not necessarily whether the strategy is worth paying for.

- Manager quality. How long has the team been together? How did the fund perform during its worst drawdowns, not just its best years? Drawdown behavior reveals more about risk management than any pitch deck.

- Strategy fit. Does the fund fill a genuine gap in your portfolio? If you already hold diversified equities and a long/short fund with 0.7 net exposure, you may be adding fees without adding diversification. The most valuable hedge fund allocations tend to be strategies with low correlation to what you already own.

- Service providers and red flags. Reputable, independent administrators, auditors, and prime brokers are a basic hygiene check. Consistent returns with no losing months, reluctance to disclose providers, aggressive marketing, and pressure to invest quickly are all warning signs. If you are weighing whether professional advisory support is worth the cost at this stage, it often is.

Portfolio Fit and Liquidity Budgeting

For many investors, the minimum is not the real constraint. Portfolio fit is. A reasonable hedge fund allocation typically falls in the 5% to 20% range of investable assets, but the percentage matters less than sizing it relative to your liquidity budget. If you have $10 million and commit $1 million to a fund with a two-year lock-up, the remaining 90% needs to comfortably cover planned and unplanned cash needs. Treat each hedge fund as part of a broader alternatives sleeve alongside private equity, venture, and real assets, not as a standalone decision. Kubera's portfolio optimization framework covers how to structure liquidity tiers across these allocations.

Tracking the Operational Reality

Hedge fund statements arrive weeks after period-end. K-1s arrive late. Valuations include estimates. Each fund reports in its own format. As positions multiply across private vehicles, reconciling total net worth using spreadsheets becomes impractical, particularly for investors with estate planning considerations across entities and trusts.

A platform like Kubera can pull hedge fund positions, documents, and K-1s into the same view as the rest of the balance sheet, which makes allocation and liquidity decisions easier to manage. It is most useful as an organizational layer, not as a substitute for diligence.

Sign up now for a 14 day trial to get started.

Frequently Asked Questions

What is the minimum to invest in a hedge fund?

Most hedge funds require initial investments between $250,000 and $1 million, though the range extends from under $100,000 for some emerging managers to $10 million or more for elite funds. The minimum depends on the fund's size, strategy, regulatory structure, and target investor base.

Can retail investors invest in hedge funds?

Direct hedge fund investment is generally restricted to accredited investors, qualified clients, or qualified purchasers. Retail investors who do not meet these thresholds can gain indirect exposure through liquid alternative mutual funds, ETFs, or fund-of-funds vehicles, though the latter typically still require accredited investor status.

What is the difference between an accredited investor, a qualified client, and a qualified purchaser?

An accredited investor meets either a $1 million net worth threshold (excluding primary residence) or a $200,000/$300,000 income threshold. This governs offering access. A qualified client has $1.1 million under management or $2.2 million net worth; this governs whether an adviser can charge performance fees. A qualified purchaser owns $5 million or more in investments and can access 3(c)(7) fund structures that permit up to 2,000 investors.

What is a hedge fund lock-up period?

A lock-up period is the initial timeframe (typically one to two years) during which an investor cannot redeem capital. After expiration, redemptions are allowed on a periodic schedule with 30 to 90 days of advance notice. Some funds also impose gates limiting total redemptions per period.

Do hedge fund minimums apply to follow-on investments?

Usually not at the same level. Most funds set a lower minimum for additional contributions from existing limited partners, often $25,000 to $100,000. Terms are specified in the offering memorandum and any applicable side letter.

Are hedge funds registered with the SEC?

The funds themselves are not registered as investment companies. They rely on exemptions under the Investment Company Act (Sections 3(c)(1) or 3(c)(7)). However, many hedge fund managers are registered with the SEC as investment advisers under the Investment Advisers Act of 1940, particularly those managing $150 million or more.

Conclusion

A hedge fund minimum is not just a number on a subscription form. It is a filter that tells you something about the fund's investor base, operating model, and positioning. Meeting the minimum is necessary, but it is nowhere near sufficient.

The hedge fund investment requirements extend well beyond the initial check. Qualification status determines which funds are available to you. The fee structure, lock-up terms, and redemption schedule determine the real cost. And the quality of the manager, the fit of the strategy, and the role the fund plays in your broader portfolio determine whether the whole exercise is worthwhile.

The goal should not be to get access for its own sake. It should be to make a deliberate allocation that improves the risk-adjusted profile of your portfolio and sits comfortably within your liquidity capacity. That is a higher bar than most fund marketing materials acknowledge, and it is the bar that matters.