A mega backdoor Roth is a strategy that uses after-tax 401(k) contributions, plus a Roth conversion step, to move substantially more money into Roth accounts than the standard Roth IRA or regular 401(k) limits allow. For 2026, a saver whose plan supports the full mechanics can push as much as $47,500 beyond the regular employee deferral ceiling into Roth space, with additional total plan capacity available through catch-up contributions for older savers.

The catch is that it only works when the employer's 401(k) plan has the specific features the strategy depends on. For most savers, the hard part is not understanding the idea; rather, it is figuring out whether their plan actually allows the moves the strategy depends on, and whether payroll, the recordkeeper, and the annual tax reporting all line up cleanly enough to make it worth the effort.

What is a mega backdoor Roth?

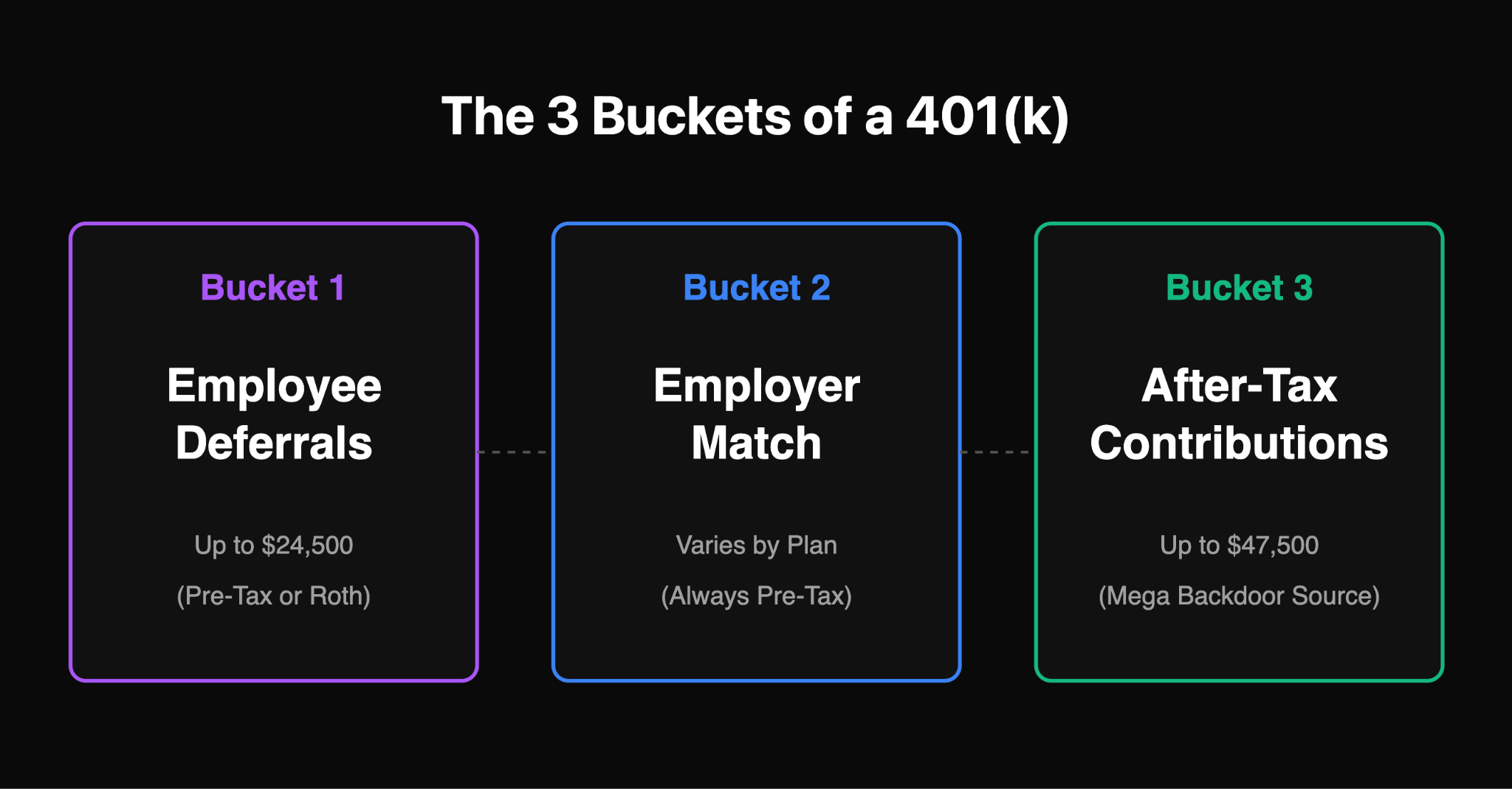

The cleanest way to see the strategy is to picture the three buckets of money flowing into a 401(k).

The first bucket is employee elective deferrals, which in 2026 are capped at $24,500, plus an $8,000 catch-up for those age 50 and older. These go in as either pre-tax or Roth 401(k) contributions.

The second bucket is employer contributions: match dollars, safe harbor contributions, profit sharing, and any other non-elective funds the employer adds to your account.

The third bucket is after-tax employee contributions. This is a separate, opt-in feature that many plans simply do not offer. These contributions are made with money you have already paid income tax on, they grow tax-deferred rather than tax-free, and on their own, they sit in an awkward middle spot of the retirement tax code.

The mega backdoor Roth lives entirely in that third bucket. You fund it, then move the money out quickly through one of two Roth conversion paths before earnings have time to pile up. Contributions that were already taxed (your basis) become Roth money, where future growth compounds tax-free and qualified withdrawals can generally be taken tax-free once the holder is over age 59 and a half and the relevant five-year rule is satisfied.

The phrase “mega backdoor Roth IRA” gets used interchangeably with “mega backdoor Roth,” even when the money technically lands in a Roth 401(k) sub-account rather than a Roth IRA. In practice, both destinations are common. The labeling is loose, but the mechanics are not.

The three buckets at a glance

Prerequisites: is the mega backdoor Roth even available to you?

Before going deeper, be honest about these. If one of them is missing, the strategy either does not work or it is not where your next dollar should go.

- You are already maxing the regular employee 401(k) deferral. If you have unused space in your $24,500 elective deferral bucket, fill that first.

- Your plan document permits after-tax employee contributions beyond the standard pre-tax and Roth deferral limits. This is not the same as having a Roth 401(k) feature. Many plans that allow Roth deferrals do not allow after-tax contributions.

- Your plan allows either in-plan Roth conversions or in-service distributions of after-tax contributions while you are still employed. Without this, after-tax money sits in the plan and the conversion leg never happens cleanly.

- You have real surplus cash flow to fund the after-tax bucket. Your emergency fund should be solid, high-interest debt handled, HSA funded if eligible, and other tax-advantaged savings in order.

- You have the bandwidth to monitor execution year after year, including contribution timing, conversion timing, 1099-R reconciliation, and coordination with any backdoor Roth IRA you are also doing.

If any of the first three items is missing, stop, and do not assume the strategy works for your plan. Plan features are not inferable from plan size, employer prestige, or whether Roth 401(k) deferrals are offered.

Mega backdoor Roth 2026 limits

Two separate sections of the tax code do most of the work.

The Section 402(g) elective deferral limit for 2026 is $24,500 for combined pre-tax and Roth 401(k) contributions. Employees age 50 and older can add an $8,000 catch-up for a total of $32,500. Employees age 60 through 63, if their plan adopts the super catch-up under SECURE 2.0, can contribute up to $11,250 of catch-up instead of $8,000, for a total of $35,750.

The Section 415(c) overall annual additions limit is $72,000 for 2026. This is the combined ceiling for all sources flowing into the plan: employee deferrals, employer contributions, and after-tax contributions together. Catch-up contributions are outside the 415(c) limit, which is why a 50+ saver can reach up to $80,000 of total plan activity, and the 60-63 super-catch-up cohort up to $83,250.

The formula for after-tax contribution room is straightforward:

After-tax room = $72,000 overall limit − your elective deferrals − employer contributions

Every dollar the employer contributes is a dollar of after-tax capacity you lose. This is why two employees at the same salary, in the same plan, can have wildly different mega backdoor Roth ceilings in a given year.

2026 after-tax contribution room by scenario (under age 50)

One SECURE 2.0 change is worth naming alongside these limits. Starting in 2026, participants aged 50 and older who had prior-year FICA wages of more than $150,000 (indexed for inflation) from the employer sponsoring the plan must make their catch-up contributions as Roth. The IRS issued final regulations in September 2025, with a good-faith compliance standard for 2026 and full effectiveness in 2027. This does not directly change mega backdoor Roth mechanics, which live in the after-tax bucket rather than the catch-up bucket, but it does change how affected high earners should think about overall Roth positioning.

How the mega backdoor Roth works, step by step

- Confirm plan features. Ask the three questions below before you elect anything.

- Elect after-tax contributions through payroll. These go in post-tax as a payroll deduction, separate from your pre-tax or Roth deferral election. You may need to contact HR, benefits, or the recordkeeper directly, since many payroll portals bury the feature.

- Convert quickly. The gold standard is per-paycheck automatic conversion. Weekly, monthly, or quarterly conversions also work. Annual conversions are where earnings drift and the tax picture gets messier.

- Choose the conversion path: in-plan Roth conversion to the Roth 401(k) sub-account, in-service distribution to an outside Roth IRA, or a split rollover where allowed.

- Reconcile at tax time. Verify that the Form 1099-R reflects only the growth between contribution and conversion as taxable, not the basis.

The three questions to put directly to HR or the plan administrator:

- Does the plan allow after-tax employee contributions beyond the regular pre-tax and Roth deferral limits?

- Does the plan allow in-plan Roth conversions, so after-tax dollars can be moved into the Roth 401(k) sub-account while I am still employed?

- Does the plan allow in-service distributions of after-tax contributions, so I can roll them out to a Roth IRA while still employed?

A “yes” to the first and either of the next two usually means the strategy is available. A “yes” to all three means you have flexibility on the conversion path.

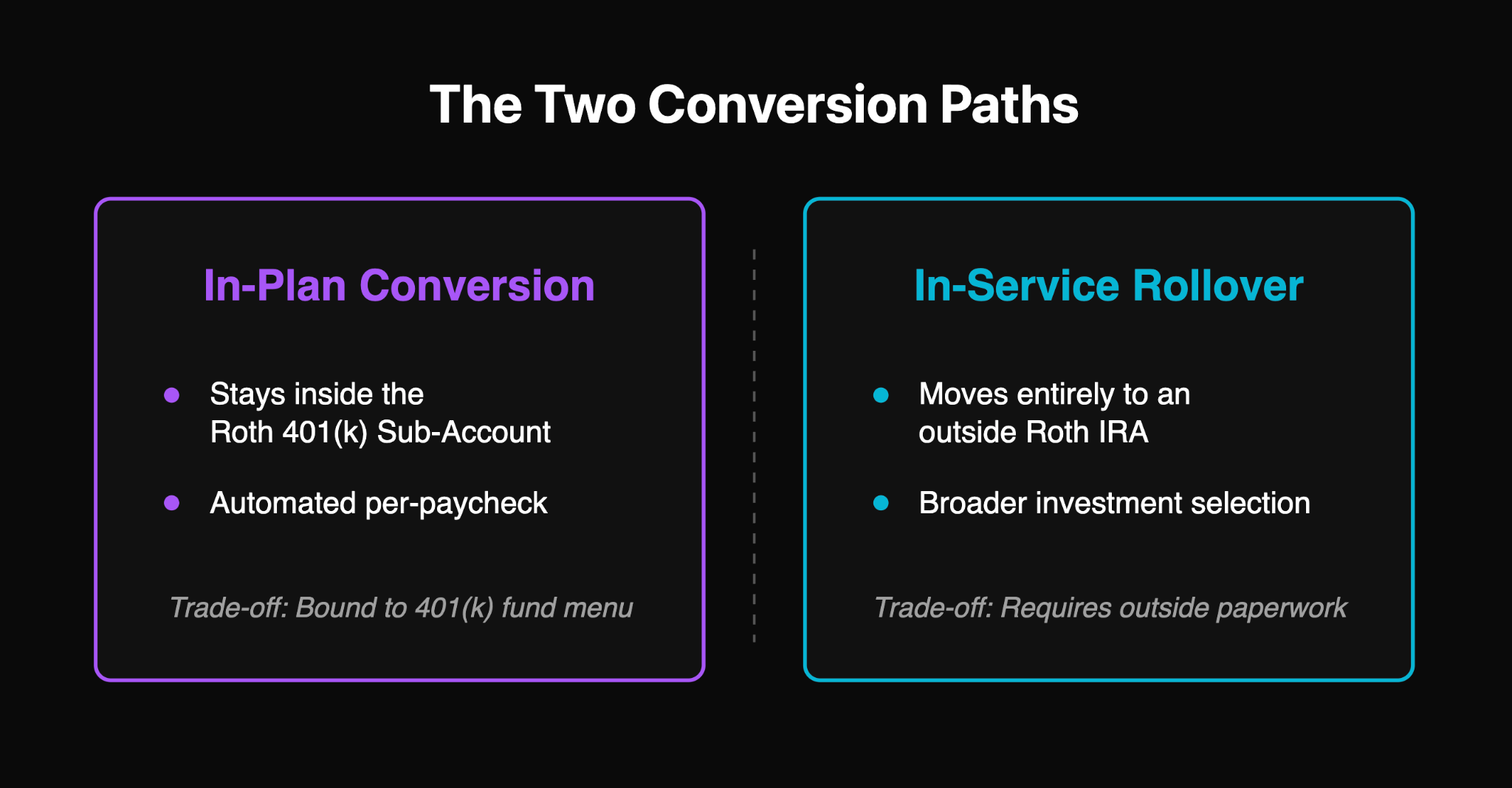

Two conversion paths: in-plan conversion vs. rollover to a Roth IRA

In-plan Roth conversion. This moves after-tax dollars into the Roth 401(k) sub-account within the existing 401(k). One plan, one statement, no outside paperwork. The tradeoff: you are bound to the plan's investment menu and the money is subject to 401(k) distribution rules until you separate from service. Some plans offer an automatic in-plan conversion feature that processes per payroll, which effectively eliminates earnings drift.

In-service rollover to a Roth IRA. This moves after-tax dollars out of the plan entirely and into a Roth IRA you control. The upside is broader investment selection, no 401(k)-level fees, and eventual freedom from Roth 401(k) RMD mechanics for the converted portion. The tradeoff is an additional account to track and verification that the plan permits in-service distributions of after-tax money specifically.

Split rollovers under Notice 2014-54. If earnings have accumulated in the after-tax sub-account before conversion, you can direct the after-tax contributions to a Roth IRA and the pre-tax earnings to a traditional IRA. Distributions sent to multiple destinations at the same time are treated as a single distribution for allocating pre-tax and after-tax amounts under Notice 2014-54. This separation is cleaner with in-service distributions than with in-plan conversions, which generally move basis and earnings together and tax the earnings as ordinary income at conversion.

The practical implication: if your plan only allows annual conversions, the split-rollover path is a legitimate way to keep the growth portion from being taxed immediately. If your plan allows per-paycheck conversions, the earnings piece is usually so small that it does not matter.

Real-world examples for realistic savers

These assume 2026 limits and set aside catch-up contributions for simplicity.

Example 1: High earner, no employer match

Jasmine, 38, earns $320,000 at a fintech. The plan has no match but offers after-tax contributions with daily auto-conversion to the Roth 401(k). She defers the full $24,500 into a Roth 401(k) and contributes $47,500 into the after-tax bucket across the year, with each contribution converting the same pay period. Roth-bucket additions for the year: $72,000. Taxable earnings on conversion: minimal, because the daily conversion cadence leaves little time for growth.

Example 2: Standard 3% match

Marcus, 42, earns $200,000 at a national accounting firm. Employer matches 3% ($6,000). Marcus defers $24,500 pre-tax. After-tax room: $72,000 minus $24,500 minus $6,000 equals $41,500. He also contributes $7,500 via a backdoor Roth IRA. Combined Roth-side additions for the year: $49,000.

Example 3: 6% match, higher salary

Priya, 45, earns $275,000 as a tech PM. Employer match: 6%, equal to $16,500. She defers $24,500 pre-tax. After-tax room: $72,000 minus $24,500 minus $16,500 equals $31,000. Her plan allows monthly conversions but not per-paycheck, so she checks her statement each month to confirm timely processing.

Example 4: Very generous employer contribution

Dan, 49, is a senior executive at a Fortune 500 company. Employer match plus profit sharing totals $35,000. Elective deferral: $24,500. After-tax room: $72,000 minus $24,500 minus $35,000 equals $12,500. Smaller space, but meaningful. At his marginal rate, compounding $12,500 a year of Roth money for 15 to 20 years produces a significant tax-free balance.

Long-term illustration

A saver who consistently contributes $35,000 a year via the mega backdoor, invested at a 7% nominal annual return, accumulates roughly $1.5 million of Roth wealth over 20 years that will never face federal income tax on qualified withdrawal. These projections are illustrative, not guaranteed, and sensitive to contributions, returns, and market conditions. They do, however, show why the strategy tends to become a core planning tool for high earners once the plan supports it.

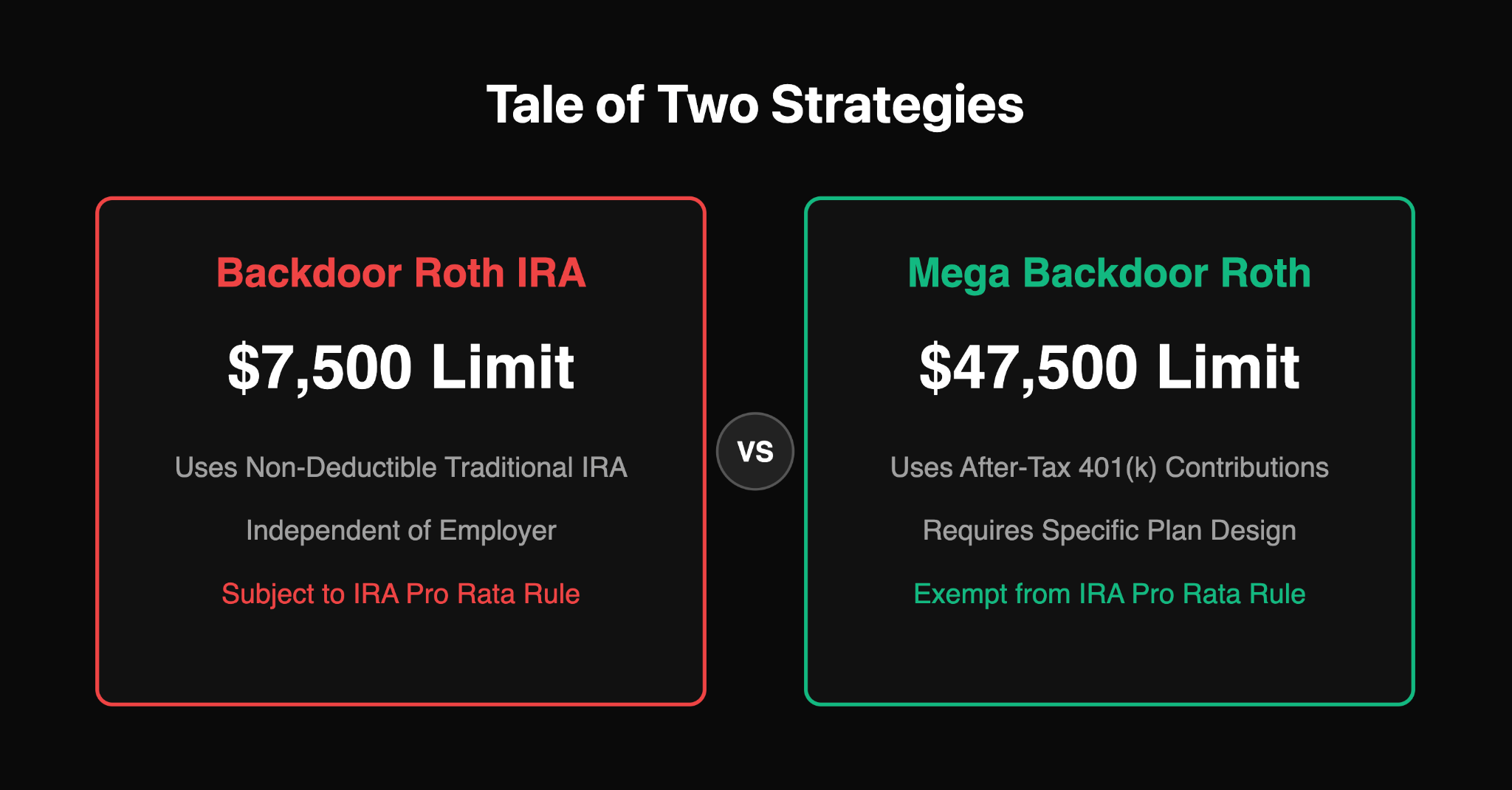

Mega backdoor Roth vs. backdoor Roth IRA

These strategies share a last name. They are otherwise distinct and can coexist.

One common misconception is worth flagging. The IRA pro rata rule is an IRA-level rule. It does not apply to after-tax money inside a 401(k) plan. It can bite you if you try to do a backdoor Roth IRA while holding pre-tax money in any traditional IRA. It does not automatically bite the mega backdoor Roth, because the plan-level basis allocation works differently. Savers who casually import IRA rules into their 401(k) thinking end up confused. The two sets of rules look similar and are not.

Who should consider a mega backdoor Roth

The strategy fits best for:

- High-income professionals who are already maxing the regular 401(k) deferral and a backdoor Roth IRA and still have surplus cash to invest.

- Executives with concentrated equity compensation who want to build tax-free space without triggering additional current-year taxable events.

- Self-employed individuals with a properly designed solo 401(k) that includes after-tax contributions and in-service distribution or in-plan conversion features.

- Earners above the Roth IRA contribution phase-out ranges ($153,000 to $168,000 for singles and heads of household, $242,000 to $252,000 for married couples filing jointly in 2026) who still want meaningful Roth exposure.

- Savers who expect a similar or higher effective tax rate in retirement and value tax diversification more than a current-year deduction.

“Can use it” and “should use it” are different questions. A 28-year-old with fifty years of compounding ahead and a moderate marginal tax rate benefits from this differently than a 58-year-old executive funding a bridge to retirement. Both can run the math. They may not reach the same conclusion.

When not to do this

- You have not yet maxed the regular 401(k).

- Your emergency fund is thin, or you are carrying high-interest consumer debt.

- You are HSA-eligible and underfunded. The triple-tax HSA usually beats almost everything else at the margin.

- You will need the money inside three to five years. Roth conversions have five-year clocks that complicate penalty-free access before 59 and a half.

- Your plan only allows infrequent conversions and you are uncomfortable with the taxable earnings drift that produces.

- You are early in a business with volatile cash flow and cannot commit consistently.

- You are uncertain you will stay on top of the tax reporting year after year.

Sometimes a taxable brokerage account is the more honest answer. It preserves flexibility, generates long-term capital gains at preferential rates, and avoids plan-operations risk. The 401(k)-versus-brokerage tradeoff is more nuanced than the Roth-at-all-costs framing suggests.

Tax implications and risks

Contributions into the after-tax bucket are post-tax dollars. That basis will be recovered tax-free at conversion. Earnings that accrue in the after-tax sub-account before conversion are treated as pre-tax, which means they are taxable at ordinary income rates when converted to Roth.

This is why conversion speed matters. Per-paycheck auto-conversion can keep taxable earnings down to pennies. A plan that only allows annual in-service distributions can leave many months of dividends, interest, and realized gains sitting in the after-tax bucket as taxable-on-conversion income.

A few underappreciated nuances worth internalizing:

- The IRA pro rata rule, which prorates any IRA distribution between basis and pre-tax, does not apply the same way to plan-based mechanics. Do not import IRA reasoning into 401(k) conversions.

- Form 8606 is the IRS form for IRA basis reporting. It is not the form for plan-based Roth conversions. Filing it when the facts do not call for it is a common error. Plan-based conversions generally flow through Form 1099-R to your Form 1040, unless you also have separate traditional IRA nondeductible basis in play.

- The “once per year” 60-day IRA rollover rule does not apply to direct rollovers of after-tax plan money to a Roth IRA.

- Large conversions can warrant estimated tax payments. A taxable earnings portion that shows up in January, reported against the prior tax year, can catch savers off guard.

Legislative risk is worth naming but not dramatizing. Congress has debated restricting or eliminating back-door Roth strategies several times over the past decade. As of this writing, both the backdoor Roth IRA and the mega backdoor Roth remain legal under current law. That can change. Savers should run the math for the current tax year, not for a hypothetical future law.

Solo 401(k) and self-employed considerations

A solo 401(k) can, in principle, support the mega backdoor Roth. In practice, the off-the-shelf solo 401(k) documents offered by the major discount brokerages typically do not include the after-tax contribution feature or in-service distribution provisions. Self-employed savers who want this strategy usually need a custom plan document, adopted through a third-party administrator who offers the right template.

A few practical notes:

- For solo owners with no common-law employees, ACP nondiscrimination testing concerns that can limit the strategy in large employee populations generally do not apply in the same way.

- The plan must actually be set up with the right provisions. Intent does not count. The plan document controls the features available.

- Contributions are still constrained by compensation, the 415(c) limit, and the interaction with whatever entity structure you are operating through. S-corp owners, LLC members, and sole proprietors face different practical limits.

If you are self-employed and want this strategy, talk to a TPA or retirement-plan-savvy tax advisor before you assume it works. The self-employed retirement plan landscape is more nuanced than the marketing usually suggests.

The operational challenge of tracking the strategy

A saver running all of the pieces in a given year might have:

- A 401(k) with a pre-tax sub-account, a Roth 401(k) sub-account, an employer-contribution sub-account, and an after-tax sub-account.

- A Roth IRA receiving in-service distributions.

- A separate Roth IRA receiving backdoor Roth contributions.

- A traditional IRA holding any pre-tax earnings split off under Notice 2014-54 mechanics.

- A taxable brokerage, HSA, and deferred compensation balances sitting alongside.

Across all of that, there are contribution caps that interact, conversion dates that matter for five-year clocks, tax forms that need reconciling, and cash flow timing that needs active management through payroll. Spreadsheets handle the math but go stale the moment a plan statement updates, an RSU vests, or a bonus retimes a contribution.

When technology helps

A net worth platform that connects to the plan recordkeeper, the Roth IRA custodian, the traditional IRA, and the taxable brokerage surfaces the strategy in one place.

Kubera is a personal balance sheet tool that aggregates retirement accounts, Roth IRAs, traditional IRAs, taxable brokerage, real estate, private investments, and other household assets in one view. Concretely for this strategy, that means seeing whether after-tax contributions are actually being converted on the schedule you set up, keeping the multiple Roth vehicles (the Roth 401(k) sub-account, any in-service rollover Roth IRA, and a separate backdoor Roth IRA) visible in one place rather than scattered across three logins, and having a contemporaneous record of balances to reconcile against the 1099-R you'll receive at tax time.

That does not replace the plan administrator or the tax advisor, but it does replace the stale spreadsheet. For most households, the goal is an integrated view that supports a longer wealth-management process rather than another disconnected login.

Sign up now for a 14 day trial to get started.

FAQ

What is a mega backdoor Roth?

A strategy that uses after-tax 401(k) contributions, then converts those dollars to Roth status inside the plan or via rollover to a Roth IRA. It allows savers to move significantly more into Roth accounts than the Roth IRA or standard 401(k) limits alone permit.

Is the mega backdoor Roth legal in 2026?

Yes, under current law. It relies on existing provisions in the Internal Revenue Code that permit after-tax 401(k) contributions and Roth conversions. Congress has considered restricting it; no such change has been enacted at the time of writing.

What are the mega backdoor Roth 2026 limits?

The 2026 overall 401(k) annual additions limit is $72,000. The maximum theoretical after-tax contribution is $47,500, calculated as $72,000 minus the $24,500 elective deferral limit, and reduced further by any employer contributions. Catch-up contributions for savers 50 and older (and the higher 60-63 super catch-up) sit outside the $72,000 annual additions limit. That increases your total plan activity, but it does not add to the after-tax contribution ceiling; the after-tax formula still starts from the $72,000 cap.

Can I do both a backdoor Roth IRA and a mega backdoor Roth in the same year?

Yes. They use different mechanics, different accounts, and different IRS rules. Many high earners execute both, though the IRA pro rata rule can complicate the backdoor Roth IRA side if you hold pre-tax money in other traditional IRAs.

What if my 401(k) plan does not allow after-tax contributions?

Then the mega backdoor Roth is not available through that employer's current plan design. There is no workaround that sidesteps the plan document. You can advocate for a plan amendment, consider alternatives like a backdoor Roth IRA or taxable brokerage, or, for business owners, explore a custom plan document.

Does the pro rata rule apply to a mega backdoor Roth?

The IRA pro rata rule does not apply to plan-based mechanics. Plan conversions follow basis allocation rules under IRS Notice 2014-54, which permit directing after-tax contributions to Roth and pre-tax earnings to a traditional IRA in a single distribution.

What is the difference between an in-plan Roth conversion and an in-service rollover?

An in-plan conversion moves after-tax dollars to the Roth 401(k) sub-account inside the same plan. An in-service rollover moves them out of the plan entirely into a Roth IRA while you are still employed. The first is simpler; the second offers more investment flexibility.

Can a solo 401(k) do a mega backdoor Roth?

Only if the plan document explicitly permits after-tax contributions and either in-plan conversions or in-service distributions. Most off-the-shelf solo 401(k) plans from discount brokerages do not include these features. A custom plan through a third-party administrator usually does.

Bringing it together

The mega backdoor Roth is among the most powerful tax-advantaged savings strategies available to high-income employees, when the plan actually supports it. The tax upside is meaningful, the Roth compounding runway is long, and the mechanics are well established under current law.

But the strategy is also plan-design-dependent in ways that matter. Payroll has to cooperate. The recordkeeper has to convert efficiently. Tax reporting has to be checked each year. Simpler priorities have to be handled first.

For savers who clear those hurdles, the mega backdoor Roth is worth taking seriously, often alongside a broader plan that includes deferred compensation, HSA funding, and taxable brokerage diversification. For savers who do not, there is no shame in acknowledging that the next best dollar belongs somewhere else, whether that is paying down a mortgage, funding a taxable account, or simply rebuilding margin. The strategy is an asset, not an obligation.