A generation-skipping trust is usually an irrevocable trust built to move wealth to beneficiaries two or more generations below you, most often grandchildren, while sidestepping an extra layer of estate or generation-skipping transfer tax. Your children can still benefit under its terms, through income or discretionary distributions, without owning the assets outright.

The goal is rarely to disinherit a generation. It is to decide which generation should own the assets for transfer-tax purposes and which can benefit from them. To work, the trust must be paired with correct generation skipping transfer tax exemption allocation and careful drafting.

That distinction matters more in 2026 than a year ago. The One Big Beautiful Bill Act (OBBBA) set the federal estate, gift, and GST exemptions at $15 million per individual from January 1, 2026, and removed the scheduled sunset that would have cut them roughly in half. The change makes deadline-driven gifting less urgent for many families, but it does not make multigenerational planning irrelevant. The families still most affected are those with fast-appreciating assets, long horizons, and estates that can compound well beyond today's exemption.

What is a generation-skipping trust?

In plain terms, it is an irrevocable trust funded by a grantor (often a grandparent) for people two or more generations younger. Because it is irrevocable, the grantor gives up the power to freely amend or revoke it, which is exactly what removes the assets, and their future appreciation, from the grantor's taxable estate when done correctly.

"Skipping" is misleading if taken literally. A well-drafted trust need not skip your children at all. The trustee can pay a child income, cover health and education, or make discretionary distributions for life, while principal is preserved for grandchildren, so the child benefits without the assets being included in the child's estate. That is the heart of it: benefit without ownership. Without this structure, wealth could face transfer tax passing grandparent to child, and again child to grandchild. The trust, paired with allocated GST exemption, lets a defined amount move down multiple generations while paying that transfer tax once at the front end, or not at all to the extent it is sheltered. The same structure supports family wealth protection goals such as shielding assets, within limits, from creditors and divorce.

One vocabulary note that trips up even sophisticated readers: the trust avoids future estate and GST tax on sheltered assets if structured and exempted properly. It does not make them grow income-tax-free. Trust income can still be taxed, to the trust, grantor, or beneficiaries depending on drafting. Conflating transfer-tax savings with income-tax savings is a common and costly error.

How the generation-skipping transfer tax works

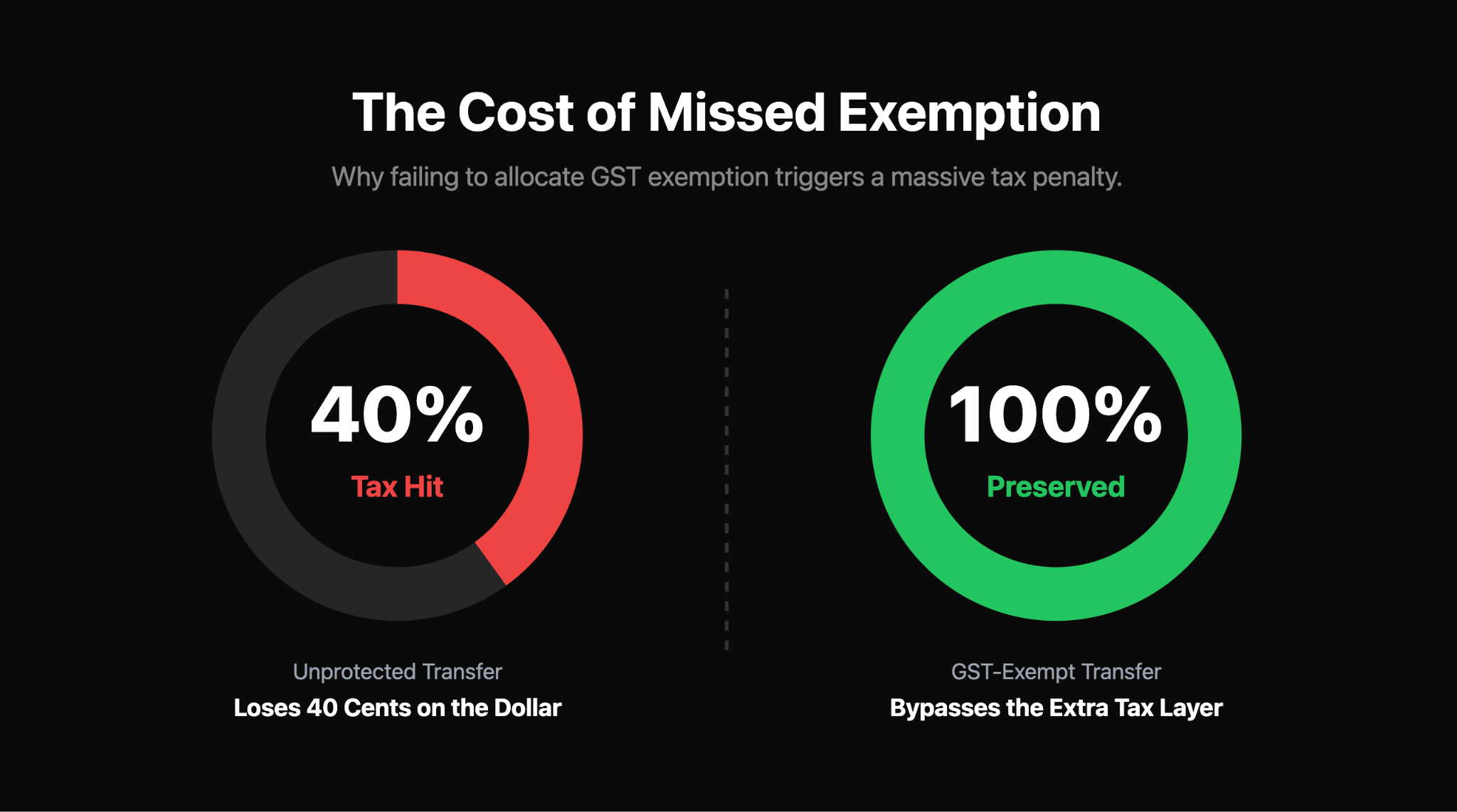

The GSTT was created in its modern form in 1986 to close a gap. Before it, families could leave assets in trust for a child for life and then to grandchildren, escaping estate tax at the child's death because the child never owned them. The tax ensures wealth bypassing a generation still bears at least one layer of transfer tax. It is a flat 40 percent, the same as the top estate and gift rate, and applies on top of any estate or gift tax. A missed allocation does not cost a few percent; it can cost 40 cents on the dollar.

Who is a skip person?

A skip person is anyone two or more generations below the transferor. For relatives that is simple: a grandchild or great-grandchild is a skip person; a child is not. For unrelated people it is age-based, anyone more than 37.5 years younger counts. That is why a large gift to a much younger partner, caregiver, or friend can be a generation-skipping transfer. A trust can also be a skip person, generally when all current beneficiaries are skip persons. One relief valve is the predeceased-parent exception (IRC Section 2651(e)): if the beneficiary's parent, your descendant, has already died, the beneficiary moves up a generation, and the transfer is generally not a skip.

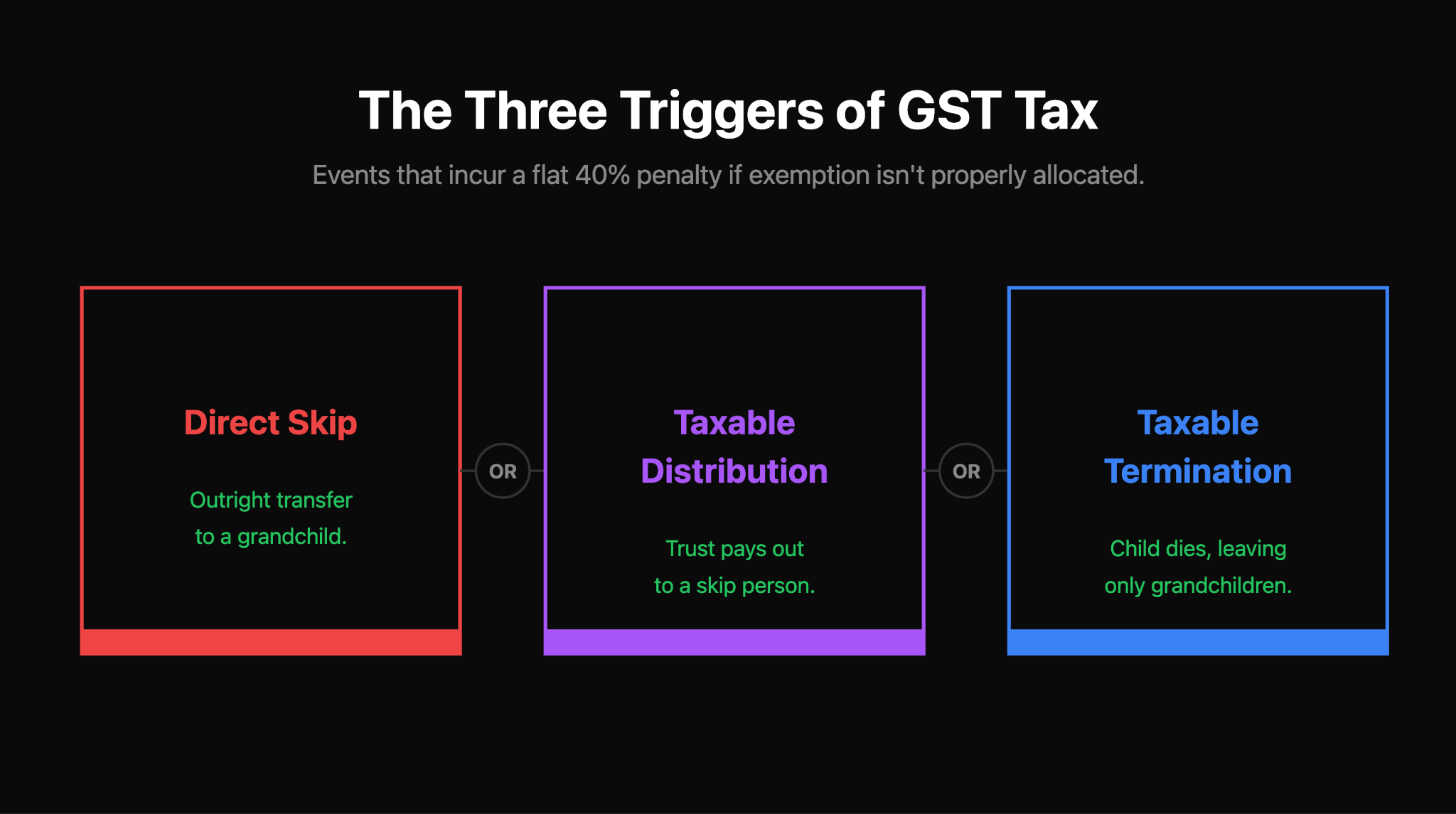

The three taxable events

GST tax is triggered by one of three events. Which applies tells you who pays and when.

The taxable termination is the one that ambushes families: a trust looks harmless for years, then triggers a 40 percent tax the moment the child dies and only grandchildren remain, unless GST exemption was allocated up front. Older trusts should be stress-tested against likely family scenarios.

The 2026 generation-skipping trust exemption

This is what changed most. For 2025 the GST exemption tracked the basic exclusion amount of $13.99 million per person and was scheduled to drop sharply at year-end. The OBBBA, signed in July 2025, replaced that cut. From January 1, 2026 the estate, gift, and GST exemptions are $15 million per individual, an effective $30 million for a married couple using both, indexed for inflation from 2027.

2026 planning point

The exemption is larger and no longer scheduled to sunset, which removes the artificial deadline that drove recent gifting. But the GST exemption is still not portable between spouses. A larger exemption raises the stakes of using it well, it does not lower them.

Two points matter. First, "permanent" describes current law, not a guarantee; a future Congress can change the exemption in either direction. Second, the higher exemption changes urgency, not relevance. A family with $20 million in slow-growing assets may now have little federal exposure. A family with $12 million in founder stock that could be worth $60 million in fifteen years has a different problem, and the GST exemption allocated today is what shelters that growth.

Why non-portability is the trap

Portability lets a surviving spouse use a deceased spouse's unused estate and gift tax exemption (the DSUE amount) by election on the estate tax return. The GST exemption has no such feature. If a spouse dies without allocating it, in most cases it is simply gone, for a couple, potentially up to $15 million of multigenerational growth lost permanently. The fix is structural: both spouses' GST exemptions must be deliberately used during life or at death, often through trusts funded and reported while both are living.

Non-portability, in one line

Estate and gift tax exemption can pass to a surviving spouse. GST exemption cannot. Use it, or risk losing it.

For lifetime transfers, GST exemption is allocated on Form 709. Automatic allocation rules apply to certain transfers, but relying on them without checking is risky, the defaults do not always match intent, and electing in or out must be done correctly and on time. Late or incorrect allocation can leave a trust partially exposed, so future distributions or terminations carry GST tax even though the family assumed the trust was fully exempt. This is squarely an advisor's job. For how lifetime gifting interacts with these limits, see Kubera's primer on family gifts and tax.

Example: with and without planning

Two simplified, illustrative examples make the difference concrete. The numbers are round and ignore state tax and growth nuance; they show direction, not precise outcomes.

Example 1: No GST planning

A grandfather leaves $15 million outright to his daughter, and the assets grow to $40 million by the time she dies decades later. If that $40 million then passes to her children and exceeds her available exemption, it can face estate tax at her death. The wealth has now potentially been exposed to transfer tax at two deaths.

Example 2: GST trust with exemption allocated

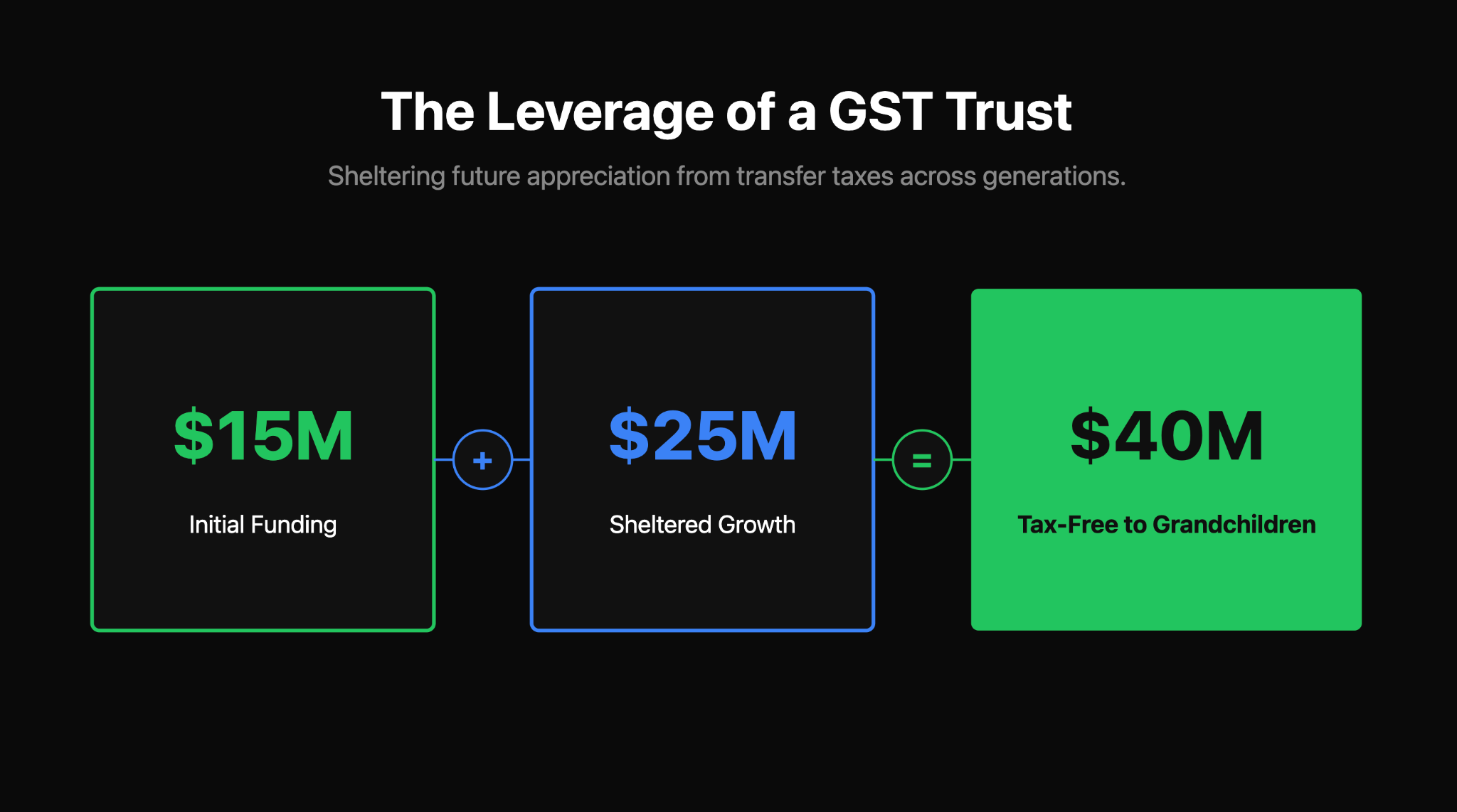

Instead, the grandfather funds an irrevocable generation-skipping trust with $15 million and allocates his $15 million of GST exemption to it. The trust supports his daughter for life, but she does not own the assets. The same growth to $40 million happens inside the trust. Because it is GST-exempt, that appreciation is generally not subject to estate or GST tax at her death, and the full value continues for the grandchildren with no fresh transfer-tax event. Exemption was measured at funding, but it shelters all later growth. That leverage is the engine of the strategy.

The lesson is not that everyone should do this. It pays off most when assets appreciate quickly and the horizon is long. For assets unlikely to outgrow the exemption, the same machinery adds cost for little benefit.

GST trust vs dynasty trust

These terms get used interchangeably, which is a mistake. A GST trust is any trust designed to use GST planning and exemption. A dynasty trust is a long-term or perpetual trust built to last across many generations; it almost always uses GST exemption, so it is a form of GST planning, but a GST trust need not be perpetual. It can benefit a child, then grandchildren, then wind down. The practical difference is time horizon and state-law dependency: a dynasty trust's effectiveness rests on its situs (perpetuities rules, trust income tax, asset protection, decanting, directed-trust statutes), while a shorter GST trust leans less on those.

GRATs are powerful for shifting appreciation but a poor vehicle for GST exemption, because of how the rules treat the retained-interest period (the ETIP). Families wanting both effects usually run a GRAT and a separate GST-exempt trust. For how illiquid or appreciating equity fits these decisions, Kubera's note on the value of unvested stock options is a useful companion.

Best state for dynasty trust planning

For a dynasty trust, the situs can matter as much as the terms. States compete on how long a trust can last, whether they tax trust income, asset protection strength, and statutory flexibility. The summary below reflects widely cited features as of early 2026. State laws change, and the right answer depends on your goals, trustee structure, asset mix, and counsel's advice.

This is not a ranking. There is no single best state for dynasty trust planning for everyone. South Dakota and Nevada are cited for privacy and protection; Delaware for its trustee market and specialized court; New Hampshire and Wyoming for flexibility and cost. The deciding factors are usually your home state's tax reach (some states tax trust income regardless of situs, at least for a period), the assets involved, and trustee structure, a decision for counsel, not a comparison chart.

What assets can fund a generation-skipping trust?

The strategy rewards assets expected to appreciate, since future growth happens outside the children's taxable estate once GST exemption is allocated. The strongest candidates: marketable securities (easy to value); concentrated stock and founder equity; closely held business interests, FLP or family LLC units (often transferred at supportable valuations, with succession coordinated); private equity and pre-liquidity interests; appreciating real estate; and life insurance held through an ILIT with GST provisions.

Some assets are awkward or risky. Do not fund a trust with anything you may need to live on, irrevocable means irrevocable. Hard-to-value assets invite scrutiny and complicate allocation. S corporation stock requires the trust to qualify (for example, as an ESBT or QSST) or it can jeopardize the S election. Encumbered or liability-prone assets carry their problems into the trust. Retirement accounts follow their own rules and generally do not belong here without specialized planning. The common thread: cleanly valued, appreciating assets you can part with are the best fit.

How children and grandchildren actually benefit

Distribution design is where the tax tool and the family document meet. The trustee operates under standards you set. Common approaches: a HEMS standard (health, education, maintenance, support), widely used because it gives the trustee a clear, ascertainable standard that helps keep assets out of a beneficiary's estate; fully discretionary distributions, which maximize flexibility and protection but concentrate judgment in the trustee; milestone or incentive provisions tied to age or events; and income distributions to a child for life while principal is preserved for grandchildren.

This is the mechanism that lets children benefit without owning the assets. A child can receive support, education funding, and discretionary help for life, while principal stays in the trust, protected and outside the child's estate, for grandchildren. In short: a trust pays a daughter's living and medical costs and her children's tuition during her life, and at her death the principal, including all appreciation, continues for the grandchildren with no taxable termination if the trust is GST-exempt. Design matters beyond tax: a trust drafted as a control mechanism can corrode the family it was meant to protect, so the better instruments pair trustee discretion with beneficiary education.

Asset protection and family governance

Asset protection is a genuine benefit and the area most often oversold. Within the limits of trust design and state law, a properly structured irrevocable trust can offer creditor protection (assets in a discretionary trust are generally harder for a beneficiary's creditors to reach, especially with a spendthrift clause in a protective jurisdiction), divorce protection (assets a beneficiary never owned outright are typically more insulated, though outcomes vary by state), and protection from a beneficiary's own decisions.

The caveats are real. Protection depends on the trust's design, the situs state's laws, trustee discretion, and the specific creditor facts. There is no universal guarantee. Critically, too much beneficiary control cuts the other way: broad beneficiary powers can both weaken creditor protection and, in some cases, pull assets back into the beneficiary's taxable estate. A trust protector can hold limited powers (change situs, replace a trustee, adapt administrative terms) without the kind of control that triggers inclusion. Choosing the right fiduciary is its own decision; Kubera's guide to choosing a trustee covers the tradeoffs. No structure substitutes for communication.

GST trust cost setup and ongoing administration

What does a GST trust cost setup run? It depends on complexity, but the components are predictable. A sophisticated generation-skipping or dynasty trust is not a download-a-template exercise, the drafting, exemption allocation, and administration are exactly where value is created or destroyed. The ranges below are illustrative and current as of early 2026.

These costs are generally justified when the expected transfer-tax savings, asset protection, and multigenerational benefits clearly exceed the lifetime cost of administration, that is, when the estate is large enough and the horizon long enough for the math to work. For a family comfortably below the exemption, ongoing fees can quietly outweigh the benefit.

How to set up a generation-skipping trust

The mechanics follow a logical order, each step depending on accurate information from the one before, which is why a clear net-worth picture at the outset matters.

- Estimate net worth and projected growth, including brokerage, real estate, private equity, business interests, crypto, and collectibles. Project the estate 10 to 30 years out.

- Identify beneficiaries and skip persons, including any unrelated individuals 37.5+ years younger.

- Decide whether GST planning is needed now, comparing projected growth against the current exemption.

- Choose the trust type and state situs, a shorter GST trust or a perpetual dynasty trust, in a fitting jurisdiction.

- Select the trustee and consider a co-trustee or trust protector, balancing control, expertise, continuity, and tax consequences.

- Define distribution standards (HEMS, discretionary, milestone, or income) that protect against estate inclusion.

- Decide which assets to fund, favoring cleanly valued, appreciating assets; obtain valuations for private holdings.

- Allocate GST exemption correctly, typically on Form 709 for lifetime transfers; confirm automatic-allocation defaults.

- Coordinate with the broader estate plan, aligning the will, revocable trust, beneficiary designations, insurance, and business succession.

- Track assets, records, and valuations over time. Funding and future planning depend on current data.

Setup checklist, at a glance

- Before funding: net-worth and growth estimate, beneficiary/skip-person map, need analysis, trust type and situs, trustee and protector, distribution standards.

- At funding: asset selection, valuations, transfer documents, GST exemption allocation strategy.

- After funding: Form 709 filing, coordination with the estate plan, ongoing recordkeeping and revaluation.

Drawbacks and when a GST trust may not make sense

A balanced view names the costs. Irrevocability means giving up control over contributed assets. Complexity, drafting, administration, tax filings, and trustee fees recur for as long as the trust exists. Compressed trust income tax brackets mean income retained in a non-grantor trust can be taxed heavily, an income-tax issue separate from the transfer-tax benefits. There is loss of direct control, potential family conflict, trustee risk, administrative burden, evolving state law, and the possibility that a future Congress changes "permanent" exemptions. Overfunding can strand assets you needed; underfunding wastes exemption.

Some families should probably not use one, at least not yet: those comfortably below the exemption with no realistic path past it, those who may need access to the assets, those unwilling to take on the complexity, and those whose goals are better served by simpler tools. Annual exclusion gifts, direct payments of tuition and medical expenses (not treated as taxable gifts when paid directly to the institution or provider), and 529 plans accomplish a great deal without an irrevocable trust. The strategy should earn its place, not be adopted by default.

Fitting it into the broader plan, and seeing the whole estate

GST planning should never happen in isolation. A generation-skipping trust must coordinate with your will and revocable trust, other irrevocable trusts, ILITs, GRATs and SLATs, beneficiary designations, charitable planning, business succession, and estate liquidity. When these conflict, the damage is quiet but real: a beneficiary designation that overrides a trust, a GRAT never coordinated with GST allocation, a business interest funding a trust with no buy-sell behind it. For the wider context, Kubera's overviews of estate planning and trusts are useful before you sit down with counsel.

A problem that rarely makes the legal checklists routinely undermines real plans: most wealthy families do not know their current net worth with precision. Assets sit across brokerage and bank accounts, multiple LLCs, private equity, real estate in several states, crypto wallets, operating businesses, and collectibles, each updated on its own schedule. The consequences are direct. If the picture is incomplete, the decision about whether GST planning is even needed can be wrong. An estate under the exemption today can cross it after years of appreciation. Funding decisions depend on current and projected values, not stale statements. And the costliest coordination failure, leaving one spouse's non-portable GST exemption unused, is likelier when no one has a clear, current view of who owns what.

This is the practical role a tool like Kubera can play. Kubera is an asset-tracking and net-worth platform, not a legal or tax tool. It does not set up trusts, draft documents, or file Form 709, and it does not replace your attorney, tax advisor, or trustee. What it does is keep the operational picture current: tracking total net worth across brokerage, bank, real estate, private equity, crypto, business interests, and collectibles in one place; helping model how an estate might grow; and letting you share a read-only view with the advisors who build the plan. Seeing your financial life on one page keeps trust funding decisions grounded in real numbers and makes conversations with counsel faster.

Sign up now for a 14 day trial to get started and explore more.

Frequently asked questions

What is a generation-skipping trust?

Usually an irrevocable trust that transfers wealth to beneficiaries two or more generations below the grantor, most often grandchildren, while avoiding an additional layer of estate or GST tax. Children can still benefit under the trust terms without owning the assets outright.

What is the generation-skipping trust exemption in 2026?

$15 million per individual, an effective $30 million for a married couple using both exemptions, up from $13.99 million in 2025. The OBBBA set this amount, removed the prior scheduled sunset, and indexes it for inflation from 2027.

Is the GST exemption portable between spouses?

No. Unlike the estate and gift tax exemption, the GST exemption is not portable. If a spouse dies without using it, it is generally lost, so married couples must plan deliberately to use both exemptions.

What is the difference between a GST trust and a dynasty trust?

A GST trust is any trust designed to use GST planning and exemption. A dynasty trust is a long-term or perpetual trust meant to last across many generations and almost always uses GST exemption. Every dynasty trust is GST planning, but a GST trust can be shorter-term, and dynasty trusts depend far more on state trust laws.

What is the best state for a dynasty trust?

There is no single best state for everyone. South Dakota, Nevada, Delaware, Alaska, New Hampshire, and Wyoming are common choices for some mix of perpetual or near-perpetual duration, no state income tax on trusts, strong asset protection, privacy, and flexible statutes. The right choice depends on your goals, your home state's tax reach, the assets, and counsel's advice.

How much does it cost to set up a GST trust?

Drafting a sophisticated generation-skipping or dynasty trust often runs from roughly $5,000 to $25,000 or more. Ongoing costs include a professional trustee (commonly about 0.5 to 1.5 percent of assets per year, or flat fees in directed-trust arrangements), tax prep, accounting, valuations, and situs fees. Template online forms are not appropriate here.

Can children benefit from a generation-skipping trust?

Yes. The trust can support children for life through income or discretionary distributions for health, education, maintenance, and support, while principal is preserved for grandchildren. Children benefit without owning the assets, which keeps principal out of their taxable estate.

Are GST trusts good for asset protection?

They can offer meaningful protection from creditors, divorce, and a beneficiary's own decisions, but it is not absolute. It depends on the trust's design, the situs state's laws, trustee discretion, beneficiary powers, and the facts. Giving a beneficiary too much control can weaken protection and even cause estate inclusion.

The bottom line

A generation-skipping trust can be a genuinely powerful tool for tax-efficient wealth preservation, but only for the right family and only when built and maintained with care. The 2026 exemption of $15 million per person makes the strategy less urgent than it felt under the looming sunset, yet no less relevant for families with fast-appreciating assets, long horizons, and estates that can compound past today's thresholds.

The strategy succeeds or fails on the details. Correct GST exemption allocation, the right situs, a well-chosen trustee, sound distribution standards, attention to non-portability, and disciplined administration separate a trust that quietly does its job for generations from one that triggers a 40 percent surprise or strands an unused exemption. If your wealth, assets, and goals point this way, the next step is not a template. It is a current, complete personal balance sheet and a conversation with qualified estate and tax counsel.

This article is for general educational purposes only and is not legal, tax, or investment advice. Estate, gift, GST, and income tax treatment differ and depend on federal and state law, trust language, beneficiary powers, trustee discretion, exemption allocation, asset type, and future legislation, all of which change over time. Consult a qualified estate-planning attorney and tax advisor before acting.