What Is a Bank Statement Loan?

A bank statement loan is a mortgage that verifies income through bank deposit history rather than traditional documentation like W-2s or federal tax returns. The lender reviews 12 or 24 months of bank deposits to calculate an average monthly income figure and then uses that figure to assess repayment ability.

You may also see this product called a bank statement mortgage or an alternative income verification mortgage. Both terms refer to the same class of product, where the defining feature is that income is derived from deposit history rather than employment records.

Bank statement loans are non-QM (non-qualified mortgage) products. QM loans must meet specific underwriting standards set by the Consumer Financial Protection Bureau, including the requirement to document income through methods that produce a "reliable and accurate" income figure. Traditional W-2 or tax-return documentation meets that standard, whereas bank deposits, used alone, do not.

Non-QM lenders operate outside those rules and can use bank deposit history as an alternative income measure. Non-QM does not mean high-risk or subprime; these loans are frequently used by creditworthy borrowers with strong assets and real income. The "non-qualified" label reflects the documentation approach, not the borrower's creditworthiness.

Who Is a Good Fit for a Bank Statement Loan?

1. Self-employed borrowers and business owners

Self employed mortgage bank statements programs exist specifically for this group. Business owners who pay themselves through distributions, S-corporation salaries, or pass-through income often show lower taxable income than their actual cash flow because business deductions reduce the figure on paper. Bank deposits reflect what money actually moved through the business and the owner's accounts.

2. Founders and LLC owners

Founders and LLC owners with equity or ownership income often experience irregular cash flow that makes two-year average tax-return figures misleading. Bank deposit history over the prior 12 or 24 months typically gives a more accurate picture of current earning capacity.

3. Freelancers and contractors

Independent consultants, gig workers, and contractors with income from multiple clients may have W-2s from multiple sources, 1099s, and Schedule C income that creates a complex tax picture. A bank statement loan simplifies the income calculation to actual deposits.

4. Commission-based earners

Real estate agents, financial advisers, salespeople, and others with significant commission income can see large income swings year to year. Recent deposit history may be more representative of current income than a two-year tax return average.

5. Real estate investors

Investors with significant rental income who hold properties through LLCs or other structures often show limited personal taxable income after depreciation and deductions. Bank deposits reflect actual cash flow from the portfolio.

Who may not be the right fit

Borrowers who can easily qualify for a conventional mortgage will get significantly better rates and terms through that route. If you have straightforward W-2 income, strong credit, and the standard down payment, compare conventional options before pursuing a bank statement loan. The rate premium is real.

How Do Lenders Calculate Income From Bank Statements?

1. Personal vs. business bank statements

This distinction matters significantly. Personal bank statement programs use deposits into your personal accounts. Business bank statement programs use deposits into your business accounts and then apply an expense factor to estimate net income. Some lenders offer both and let you use whichever produces a better qualifying figure.

If you deposit business revenue directly into your personal account, a personal bank statement program may work. If you separate business and personal funds, a business bank statement program typically applies. Commingled accounts create ambiguity that can slow the process.

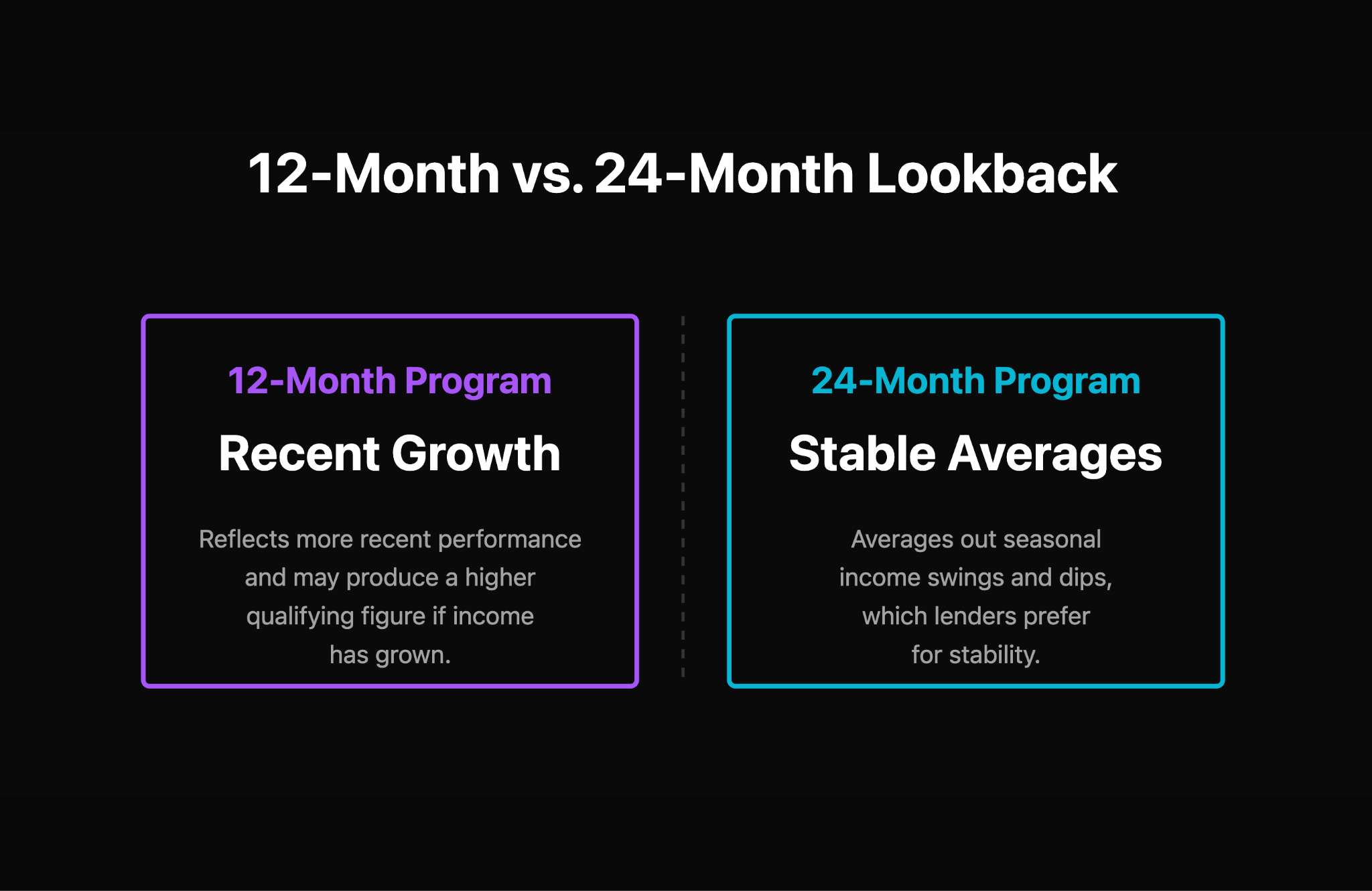

2. 12 month vs. 24 month bank statement loan programs

A 12 month bank statement loan uses the prior 12 months of deposits to calculate average monthly income, while a 24 month bank statement loan uses the prior 24 months. Each has trade-offs.

A 24-month lookback averages out seasonal income swings and dips, which lenders prefer for stability. A 12-month lookback reflects more recent performance and may produce a higher qualifying figure if income has grown. If you experienced a difficult year two years ago followed by strong performance recently, a 12-month program may serve you better. If your income is steady and you want the broadest lender options, a 24-month program typically offers more choices.

3. Expense factor logic

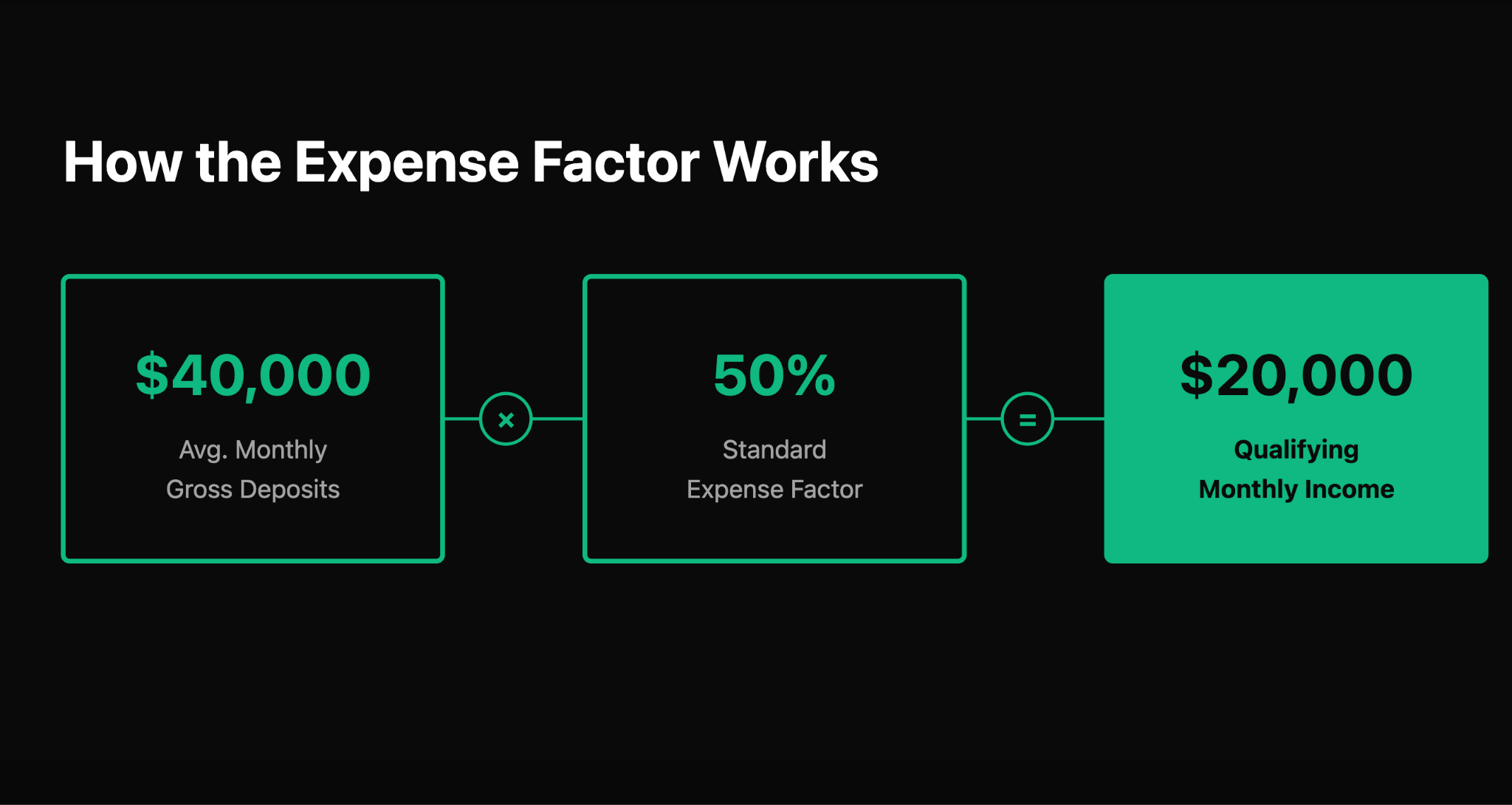

For business bank statement programs, lenders apply an expense factor to business deposits to arrive at a net income estimate. The expense factor represents the lender's assumption about what percentage of gross deposits goes to operating expenses.

A common starting point is a 50 percent expense factor. If your business deposits average $40,000 per month and the lender uses a 50 percent factor, the qualifying income figure is $20,000 per month. Some lenders allow you to submit a CPA-prepared profit and loss statement to document lower actual expenses and reduce the expense factor, resulting in a higher qualifying income figure.

Understanding how your lender calculates the expense factor is critical to understanding how much you can borrow. Ask directly before you submit an application.

Why documentation quality matters

Even though a bank statement loan uses deposits rather than W-2s, the documentation burden is still substantial. Lenders need complete statements, all pages, no gaps, and clear deposit patterns. Business and personal funds should ideally be separated. Unexplained large deposits will be questioned. The income calculation only works if the documentation is clean.

What Documents Do You Need for a Bank Statement Loan?

Expect more documentation than a conventional loan, not less. The flexibility is in how income is calculated, not in how much paperwork is required.

Bank statements

- 12 or 24 months of complete bank statements, all pages, from every account being used for income calculation

- Business account statements and personal account statements, depending on the program type

- Each statement must clearly show deposits, the account owner's name, and the institution

Business documentation

- Business license or other documentation confirming the business is active and operating

- Documentation of your ownership percentage, especially if the business is co-owned

- A current CPA-prepared profit and loss statement if you want to use a lower expense factor

Asset statements for down payment and reserves

- Bank and brokerage statements for down payment funds, typically 60 days, all pages

- Reserve documentation: bank statement loans typically require 6 to 12 months of reserves, compared to 2 to 6 months for conventional loans

- Explanations with supporting records for any large or irregular deposits

Credit and property documentation

- Government-issued ID

- Property appraisal (ordered by the lender after you are in contract)

- Purchase contract for a home purchase, or current mortgage statement for a refinance

For more on organizing bank account documentation, see our guide to organizing bank accounts for financial clarity.

Pros and Cons of Bank Statement Loans

Understanding the tradeoffs helps you decide whether this program is right for your situation.

Bank Statement Loans vs. Conventional vs. Asset-Based Mortgages

It helps to see where bank statement loans fit relative to other nontraditional mortgage options.

For detailed guidance on the alternatives, see our articles on asset-based mortgages, margin loans vs mortgages, and buying a rental property.

How to Prepare for Bank Statement Loan Underwriting

The lenders who offer bank statement products see a lot of messy applications. Clean, organized submissions move faster and produce better outcomes.

- Separate business and personal accounts if you have not already. Commingled accounts make income calculation ambiguous and may lead to a lower qualifying figure.

- Pull 24 months of complete statements from every account you plan to use. Include all pages. Download each month as a separate PDF and label them clearly.

- Review your deposit history for large or irregular deposits. Identify any that came from sources other than business operations. Prepare short explanations and supporting records for each.

- Calculate your own income estimate using the lender's likely expense factor. If the lender uses a 50 percent factor, multiply your average monthly gross deposits by 0.50 to get your qualifying income estimate. Compare this to the loan payment you need to qualify.

- Get a CPA-prepared profit and loss statement if you want to use a lower expense factor. Ask the lender first whether they accept this and what format they require.

- Prepare a balance-sheet summary of your assets: down payment funds, reserves, and all other holdings. This accelerates the asset documentation portion of underwriting.

- Compare 12-month vs. 24-month lookback options. If your income has grown recently, the shorter lookback may produce a higher qualifying income figure. Ask the lender whether they offer both programs.

Kubera helps you track and organize your full financial picture. For bank statement loan applications, you can use Kubera to generate a signed, dated, shareable snapshot of your assets and liabilities that accompanies your bank statement package as a clean overview for the lender. Learn more at kubera.com/proof-of-wealth. Lenders still decide what documentation they accept. Kubera does not guarantee mortgage approval.

For related documentation guides, see our articles on personal balance sheets and statements of net worth.

Frequently Asked Questions

What is a bank statement loan?

A bank statement loan is a non-QM mortgage that uses 12 or 24 months of bank deposit history, rather than W-2s or tax returns, to verify income. It is designed for self-employed borrowers and others whose taxable income does not accurately reflect their actual cash flow.

Are bank statement loans only for self-employed borrowers?

They are primarily designed for self-employed borrowers, business owners, freelancers, and commission-based earners. Some lenders extend eligibility to other nontraditional income situations. However, if you qualify for a conventional mortgage, you will almost always get better terms there. Bank statement loans are a solution for borrowers who cannot document income through standard means.

Do bank statement loans have higher interest rates?

Yes. Bank statement loans typically carry rates 1 to 3 percentage points above comparable conventional mortgage rates. The precise premium depends on the lender, loan amount, down payment, credit score, and reserve levels. Shopping among multiple non-QM lenders is important because rates vary significantly.

How many months of statements do lenders need?

Most programs require either 12 or 24 months of complete bank statements. A 24 month bank statement loan gives lenders a longer history and is typically easier to qualify for because it averages out income fluctuations. A 12 month bank statement loan reflects more recent deposits and may produce a higher income figure if your earnings have grown.

Can I use business bank statements instead of personal statements?

Yes. Most bank statement loan programs offer a business bank statement option alongside a personal bank statement option. For the business option, the lender applies an expense factor to gross business deposits to estimate net qualifying income. Personal statement programs may count a higher percentage of deposits as income but typically require that deposits come from identifiable professional or business sources.

What is an expense factor?

The expense factor is the percentage of gross business bank deposits that the lender assumes goes to operating expenses. A 50 percent factor means the lender counts half your gross business deposits as qualifying income. Some lenders accept a CPA-prepared profit and loss statement to document lower actual expenses and reduce the factor, which increases the qualifying income figure.

Is a bank statement loan the same as an asset-based mortgage?

No. A bank statement loan uses deposit history to establish income. An asset-based mortgage uses the value of your investment portfolio to impute income through an asset depletion calculation. Bank statement loans are typically used by income-earning self-employed borrowers. Asset-based mortgages are typically used by asset-rich, income-light borrowers such as retirees or passive investors. They are different products for different situations.

Track your balance sheet in Kubera

Kubera connects your bank accounts, business accounts, investments, and other assets in one organized view. Generate a signed, shareable financial snapshot to prepare for bank statement loan underwriting.

Disclaimer: This article is for informational purposes only and does not constitute mortgage, legal, or financial advice. Loan terms, qualification requirements, and interest rates vary by lender and program. Always compare options and consult a licensed mortgage professional for guidance on your specific situation.